Unit 2 Fundamental Concepts

advertisement

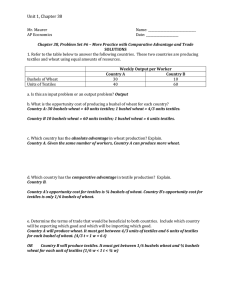

AP Macroeconomics Unit 2 Lesson 1: Key Idea: The study of economics exists because of scarcity. Scarcity forces us to choose between various alternatives (trade-offs). All choices have costs (opportunity cost). Incentives guide our choices. Scarcity- the basic condition that exists when unlimited wants exceed limited productive resources. **Scarcity is NOT a shortage! A shortage can be fixed. Trade-off- possible options that we can choose from when we face scarcity Opportunity Cost – the next best alternative given up when a choice is made Incentive- a reason for doing something. Lesson 2: Key Idea: Economics recognizes certain factors of production that are scarce. Since these factors of production are scarce, we must choose how we allocate them between various alternatives. Factors of Production: Building blocks of the economy Capital Goods- man-made tools used to make other things (tractors, factories) Entrepreneurship- willingness to combine all factors and start a business to provide goods and services Land – natural resources such as oil, coal, natural gas, timber, iron ore, etc. Labor- human workers; this can also be reflective of human capital which is the knowledge and skills workers have Allocate – to distribute. In economics, we must decide how to distribute our scarce factors of production. Will it be based on price, first-come, firstserve? Lesson 3: Key Idea: Not all decisions are “all or nothing”. With some decisions, we must decide whether we should do a little more or a little less. (Should I sleep ten more minutes? Should I eat another piece of pizza?) This is referred to as making decisions “at the margin”. A rational decision will occur where the marginal benefit is greater than or equal to the marginal cost of a decision. Marginal- additional Rational Decision – marginal benefit is greater than or equal to marginal cost Lesson 4: Key Idea: The concepts of scarcity, trade-offs, opportunity cost, and decision making at the margin can all be observed on a production possibilities curve. Production Possibilities Curve/Frontier: Trade-offs: Refrigerators or cars Opportunity Cost: If I move from Point A to Point B, I give up refrigerators. If I move from Point C to Point B, I give up cars. Scarcity: The curve is the limit of resources. Points A, B, and C are productively efficient. Point X: All resources are not being used (during a recession) Point Y: Unattainable using current resources Lesson 5: Key Ideas: Specialization and voluntary exchange increase satisfaction of both parties. Specialization: Focusing on one particular area of expertise to increase productivity. (One should specialize where they have their comparative advantage.) Comparative Advantage: Specialization should always occur where an individual, business, or country has the comparative advantage. To have the comparative advantage means to be able to produce at a lower opportunity cost than another producer. This is different than the absolute advantage, which is the ability to produce more than another producer using the same resources. To determine comparative advantage, you must determine whether the problem is an input problem or an output problem. For input problems, use the method: Input, Other, Under. (IOU). For output problems, use the method Output, Other, Over (OOO). Example of an Input Problem: ** The data below represents the number of hours needed to produce one of the following: Hours to Produce One Car Hours to Produce One Airplane United States 8 (8/16=1/2) 16 Canada 10 (10/25 =2/5) 25 (16/8 = 2) (25/10 -5/2 =2 1/2 In this example, the US has the absolute advantage in both cars and airplanes because it takes them fewer hours to produce one. To determine comparative advantage, you use the input, other goes under method. Using this method, you see that Canada should make cars and the US should make airplanes. This is where the respective opportunity costs are lower. Appropriate terms of trade will fall between the opportunity costs. acceptable term would be one airplane to 2 ¼ cars. An Example of an Output Problem: ** The data below represents output given a set number of inputs. Bushels of corn per acre Bushels ofTomatoes per acre United States 30 30 (30/30=1) Mexico 20 10 (20/10 = 2) (30/30 = 1) (10/20=1/2) In this example, the US has the absolute advantage in both. They can produce more corn and tomatoes per acre than Mexico. To determine comparative advantage, use the Output, other goes over method. Using this method, the US should specialize in tomatoes and Mexico should specialize in corn. This is where the opportunity costs are lower. An acceptable term of trade will lie between opportunity costs. For example, an acceptable trade term would be 1 bushel of tomatoes to 1 and ½ bushels of corn. Another acceptable term would be 1 bushel of corn to ¾ bushel of tomatoes. Voluntary Exchange: Willingness to trade. it benefits you! You will only make an exchange if Lesson 6: Key Ideas: Productivity is increased through specialization, technology, investment in capital goods, and investment in education (human capital). Productivity: relationship of inputs to outputs An increase in productivity will shift the production possibilities frontier to the right. Lesson 7: Key Ideas: All societies must decide how to produce and distribute goods and services. When they do this they form an economic system. Three Basic Economic Questions: What will we produce? produced? For whom will it be produced? How will it be Types of Economic Systems: Market Economy – three basic questions are answered by individuals Command Economy- three basic questions are answered by government Mixed Economy- three basic questions are answered by individuals and government Lesson 8: Key Ideas: All societies form economic systems based on their social and economic goals. These goals are often in conflict with one another. Because of this, most countries have some level of a mixed economy so that they can balance the interest between these competing goals. Economic Growth- increasing output/ increasing real Gross Domestic Product Economic Freedom- ability to start a business, work where you want, purchase what you want, sell to whom you want, etc. Economic Efficiency- using all resources to make things that people want with very little waste Economic Equity- distributing resources, goods, and services in a way that is fair Economic Security- providing an economic safety net to prevent unemployment, homelessness, etc. Economic Stability- avoiding large fluctuations in prices Goals Best Achieved in a Market Economy Goals Best Achieved in a Command Economy Economic Growth Economic Equity Economic Freedom Economic Security Economic Efficiency Economic Stability A MIXED ECONOMY helps societies achieve a balance of all these goals. Lesson 9: Key Idea: In the Soviet-style command economy, lack of information for consumers and warped incentives led to extreme inefficiency with resources. People were left with little freedom and poor-quality products. Lesson 10: Key Ideas: Market economies are characterized by private ownership, profit motive, consumer sovereignty, and competition. Private Ownership: The ability to own and control your resources and goods. You own and control your labor as well as private property. This gives you the incentive to be as efficient as you can with your resources so that you do not waste them. Profit Motive: The incentive to improve your material well-being. This is why people go to work, start businesses, and further their education. This is part of the idea of Adam Smith’s “invisible hand.” No one needs to direct the economy. People will act in their own self-interest, and this will lead to a functioning economic unit. Consumers Sovereignty: “Consumers Rule”- This is the idea that consumers ultimately decide what gets produced. Due to profit motive, entrepreneurs only want to make things that people are willing to buy. Therefore, they will make what consumers want! Competition: This is the regulating force in a market economy. When many firms compete with one another, firms that are not the best tend to go out of business. This helps to ensure low prices, high quality, and the greatest efficiency possible with our scarce resources. Lesson 12: Key Ideas: A market economy can be illustrated through a circular flow diagram. This shows the interaction between households and businesses in the factor or resource market and the product market. The exchange of resources, goods, and services takes place through the exchange of money. Factor or Resource Market: Households sell their factors of production (especially labor) to businesses in exchange for income. You participate in this market when you go to work. Product Market: Businesses sell final consumers goods and services to households. These are created using the factors of production the business purchases in the factor market. Medium of Exchange: Money is our medium of exchange. It facilitates the flow of goods, services and resources throughout the economy. If we did not have money, we would have to rely upon barter which would be much less efficient. Lesson 13: Key Ideas: There are no pure market economies left in the world. There are problems with a laissez-faire style economy, and therefore there are certain reasons for government to get involved, leading to a mixed economy. Laissez-Faire: pure free market; government “hands-off” Regulation: A rule or law placed on businesses by government. More regulation tends to increase costs for producers and prices for consumers. However, there tends to be increased safety, quality, or product clarity when regulations are in place. Deregulation: Removal of laws placed on business. Reasons for Government Involvement in a Market-based Economy 1. Redistribution of Income- This is one way a market-based economy seeks to achieve more equity and security. They tax the population and give money to specific individuals and programs. This includes Social Security, Temporary Aid to Needy Families (Welfare), Food stamps, etc. 2. Protection of Private Property Rights- Since private ownership is key to a market, there must be rule of law to protect that property. In addition, government serves to protect intellectual property by giving patents and copyrights. This gives individuals the incentive to go out and innovate so that they can expand their own material well-being, and help us in the process! 3. Provide Public Goods and Services- There are certain goods and services that would be under-produced if left to the market. These include roads, fireworks, etc. They would be under-produced due to the freerider problem, which means that people can use and enjoy a good or service and not have to pay for it. To fix this problem, the government taxes everyone and provides the service to all. 4. Correcting Market Failures (Externalities)- Sometimes the market does not distribute costs efficiently. People wind up bearing external costs from the actions of others. These are called negative externalities. Examples of this include pollution, second-hand smoke, loud music, etc. The role of government is to come in and place regulations or taxes on the groups involved in the behavior to reduce the spill-over costs. (**Actions that provide external benefits are often provided as public goods, such as education.)