Chapter 3 - Class notes file from textbook authors

advertisement

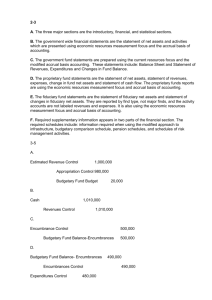

Chapter 3 Issues of Budgeting and Control Chapter 3 Granof-5e 1 Thought to Ponder: Chapter 3 "A budget is more than simply numbers on a page. It is a measure of how well we are living up to our obligations to ourselves and one another." President Barack Obama Chapter 3 Granof-5e 2 Learning Objectives Key Purposes of Budgets Various ways of classifying expenditures Key Phases of the Budget cycle Limitations of Actual-to-budget comparisons How an encumbrance system prevents overspending How budgets enhance control Chapter 3 Granof-5e 3 Budgets Key Purposes of Budgets Planning Controlling and Administering Reporting and evaluating Chapter 3 Granof-5e 4 Budgets in Government are MUCH MORE IMPORTANT than they are in Business The General Fund and special revenue funds usually require a legally adopted budget before the government can collect revenues from taxes and other sources and incur expenditures. Severe penalties may exist for failure to comply with the budget, so it is imperative that the accounting system facilitate accounting for the budget as well as all other operating transactions. Chapter 3 Granof-5e 5 Major types of Budgets Appropriation Budget Monitors current or operating fund (i.e. general fund) Typically covers one operating cycle Capital Budget Monitors construction and acquisition of long-lived assets Typically covers multiple years Flexible Budget Contains alternative budget estimates based on varying levels of output Helps distinguish fixed and variable costs Most useful to business-type activities where level of activity depends on customer demand Chapter 3 Granof-5e 6 Key Phases of Budget Cycle Preparation Legislative adoption and executive approval Execution Reporting and auditing Chapter 3 Granof-5e 7 Current GASB Model Vs. Old Model Old model: governments reported only their amended budget. Current model: requires the actual results and both the original and final appropriated budgets. Budgetary compliance can be assured by building safeguards in the accounting systems. Journals Ledgers Chapter 3 Granof-5e 8 CITY OF HOUSTON GENERAL FUND BUDGET FOR FISCAL YEAR 2008 (unaudited) (amounts expressed in thousands) Total Budgeted Resources $ 1,984,199 Total Budgeted Expenditures 1,768,473 Designated "Sign Abatement" Amount Designated "Rainy Day" Amount Budgeted Ending Fund Balance as of June 30, 2008 2,070 20,000 193,656 Total Budgeted Expenditures and Reserves Chapter 3 Granof-5e $ 1,984,199 9 Budgetary Accounts Purpose: Used to record the budgetary inflows and outflows estimated or authorized in the annual budget Accounts: Estimated Revenues, Estimated Other Financing Sources Appropriations, Estimated Other Financing Uses Encumbrances Chapter 3 Granof-5e 10 Budgetary and Operating Statement Accounts Revenues and Other Financing Sources increase fund balance when closed. Both are recognized on the Modified Accrual basis--when measurable and available to pay current period obligations. Expenditures and Other Financing Uses decrease fund balance when closed. Both are recognized on the Modified Accrual basis--when incurred, if expected to be repaid from currently available resources of the fund. Chapter 3 Granof-5e 11 Budgetary and Operating Statement Accounts (cont’d) An appropriation is a legal authorization granted by the legislative body to incur liabilities for purposes specified in the appropriation act or ordinance. Let’s do a simple example Chapter 3 Granof-5e 12 Example A A city government incorporates its budget in its accounting system and encumbers all commitments. Prior to the start of the year, the city council adopted a budget in which city revenues were estimated at $500,000 and expenditures of $450,000 were appropriated. Record the budget using only the control accounts. Estimated revenues Appropriations Fund balance $500 $450 50 Next slide shows what the detail might look like Chapter 3 Granof-5e 13 Examples of Budgetary Journal Entries (A) Budget Approved on 1-1-2010: Estimated Revenues Appropriations Fund Balance Revenues Ledger: Taxes Licenses and Permits Intergovernmental Revenues Charges for Services Fines and Forfeits Miscellaneous Revenues Appropriations Ledger: General Government Public Safety Public Works Culture and Recreations Chapter 3 Granof-5e Dr. 500,000 Cr. 450,000 50,000 300,000 50,000 50,000 50,000 25,000 25,000 $500,000 $450,000 120,000 150,000 100,000 80,000 14 Budgetary and Operating Statement Accounts (cont’d) An encumbrance is an estimated amount recorded for purchase orders, contracts, or other expected expenditures chargeable to an appropriation. Chapter 3 Granof-5e 15 Encumbrance Prevents overspending the budget Entry to record encumbrance is made when purchase order is issued, a contract is signed, or a commitment is made. Entry that records encumbrance reduces the budget available for expenditure. Outstanding encumbrances are reported in the notes to the entity’s financial statements No longer on face of balance sheet per GASB 54. Chapter 3 Granof-5e 16 Impact of GASB 54 Significant encumbrances must be reported in the notes to the financial statements A separate display of encumbrances within fund balance categories is not permitted In the general fund: add encumbrances not related to restricted, committed or assigned purposes to the unassigned fund balance In special purpose funds: add encumbrances for specific purposes to the appropriate committed or assigned fund balance This requirement is necessary because special purpose funds cannot report a positive unassigned fund balance Chapter 3 Granof-5e 17 Let’s do an example with encumbrances Based on the Example posted on Blackboard Chapter 3 Granof-5e 18 Budgetary Control — Expenditures Budgetary control of expenditures is achieved by: ensuring that a valid appropriation exists prior to recording an encumbrance or expenditure, and periodically comparing encumbrances and expenditures to appropriations. Comparison is enhanced by using a common classification scheme for appropriations, encumbrances, and expenditures Chapter 3 Granof-5e 19 Example B - Budgetary Control Example: City Clerk's office orders a new multipurpose machine on January 2, 2010 which had a list price in the vendor's catalog of $500. General Fund General Journal: Dr. Encumbrances--2010 $500 Reserve for Encumb.--2010 Chapter 3 Granof-5e Cr. $500 20 Accounting Control over Expenditures Appropriations (expenditure budget) Estimated revenues & other sources of financing (revenue budget) Encumbrances (unfilled orders) The sum of the detailed Appropriations, Encumbrances, and Expenditure account balances of the subsidiary ledger must equal the general ledger control account balances Chapter 3 Granof-5e 21 Accounting model for the General Fund ASSETS = LIABILITIES + FUND BALANCE Balance Sheet Accounts Reserved (Nonspend + Rest., Comm., & Assign) FB + Unreserved (Unassig) Fund Balance (permanent) Budgetary/ Operating Budgetary Accounts Operating Accounts Statement Accounts (temporary) Chapter 3 Granof-5e 22 Classification of Expenditures GASB suggestions classifying expenditures by any of the following: Fund Ex. general fund, special revenue fund, etc. Function or Program Def. Group of activities carried out with the same objective Ex. general government, public safety, sanitation, etc. Organization Unit Ex. police department, fire department, etc. Activity Def. Line of work contributing to a function or program Ex. highway patrol, burglary investigations, etc. Character Def. The fiscal period presumed to benefit Ex. Current, Capital, Debt Service Object Def. The types of items purchased or services obtained Ex. Salaries, fringe benefits, travel, etc. Chapter 3 Granof-5e 23 Most Commonly Used Budget . . . Object Classification Budget Chapter 3 Granof-5e 24 Object Classification Budget Traditional and most common Facilitates control Drawbacks: Discourages planning Promotes bottom-up budgeting than top-down budgeting Overwhelms top-level decision-makers with details Limits post-budget evaluation Chapter 3 Granof-5e 25 Classification of Revenues and Estimated Revenues GASB Suggestion: 1st classify by fund 2nd classify by source FUND S O U R C E Chapter 3 Sources include: Taxes (Ad-valorem and self-assessing) Special Assessments Licenses and Permits Intergovernmental Revenues Charges for Services Fines and Forfeits Miscellaneous Revenues Granof-5e 26 On What Basis of Accounting are Budgets Prepared? Chapter 3 Granof-5e 27 Basis of Accounting Neither GASB nor FASB have control over budgeting principles – Budgeting principles are set by either the government/organization or the government/organization that supervises them GASB recommends using modified accrual basis of accounting. However, most governments use the cash basis for their budgets. Chapter 3 Granof-5e 28 Cash Basis Budgeting Budgeting principles are established by individual governments or organizations and not by GASB nor FASB. Although GASB recommends the use of modified accrual basis in preparing the annual budgets, many governments adopt cash basis or modified cash basis. Chapter 3 Granof-5e 29 Cash Basis Budgeting Governments using cash basis: Assign revenues and expenditures to the period during which the cash is expected to be received or disbursed. Treat encumbrances equivalent to actual purchases. Recognize taxes and other revenues in the year in which they are due and not in the year in which they are expected to be collected. Chapter 3 Granof-5e 30 Cash Basis Disadvantages: May distort the economic impact of planned fiscal activities. May be unbalanced as to economic costs and revenues. It may give an appearance of a budget that has achieved inter-period equity when it really has not. Makes it easier to transfer resources from a fund that has a budget surplus to one that needs extra resources. Complicates financial accounting and reporting. Chapter 3 Granof-5e 31 Legally adopted budgets vs. GAAP-based Financial Statements Differences arise between the legally adopted budgets and GAAP-based financial statements. They are caused by: Basis of accounting Timing Perspective Reporting entity Chapter 3 Granof-5e 32 Performance Budgets Supplement to object classification budgets Focus on measurable units of efforts Institutionalize effective decision process The most common type of performance budget is program budget. Chapter 3 Granof-5e 33 Recording Budgets Example Additional examples to study (beyond textbook and ones we did in class) Chapter 3 Granof-5e 34 Recording Budgets Estimated revenues (DB) – Actual Revenues (CR) = Remaining revenue to be recognized Appropriations (CR) - Actual expenditures (DR) = Balance available for expenditure Refer to pgs. 105-108 for budgeting entries. Chapter 3 Granof-5e 35 Example C A government health care district incorporates its budget in its accounting system and encumbers all purchase orders and contracts. Prior to the start of the year, the governing board adopted a budget in which agency revenues were estimated at $5,600 and expenditures of $5,550 were appropriated. Record the budget using only the control accounts. JE 1: Estimated revenues Appropriations Fund balance Chapter 3 Granof-5e $5,600 $5,550 50 36 Example - C (cont’d) JE 2: During the year, the government health care district collected $5800 in fees, grants, taxes, and other revenues. Prepare journal entries. Cash $5,800 Revenues 5,800 JE 3: It ordered goods and services for $3,000. Encumbrances $3,000 Reserve for encumbrances Chapter 3 Granof-5e 3,000 37 Example – C (cont’d) JE 4: During the year it received and paid for $2,800 of goods and services that had been previously encumbered. It expects to receive the remaining $200 in the following year. a: Expenditures Cash b: Reserve for encumbrances Encumbrances $2,800 2,800 $2,800 2,800 JE 5: It incurred $2500 in other expenditures for goods and services that had not been encumbered. Expenditures Cash Chapter 3 $2,500 2,500 Granof-5e 38 Example –C (cont’d) Prepare end of year closing entries. JE 6: Revenues Estimated revenues Fund balance JE 7: Appropriations $5,550 5,300 200 50 Expenditures Encumbrances Fund balance Chapter 3 $5,800 5,600 200 Granof-5e 39 Supporting Computations – original style Reserve for Encumbrances dr cr balance $0 3,000 (3,000) bal fwd 3 4b 2,800 (200) (200) bal fwd 1 6 7 Fund balance (unassigned, unreserved) dr cr balance 0 50 (50) 200 (250) 50 (300) bal fwd 3 4b 7 Encumbrances (temporary acct) dr cr balance 0 3,000 3,000 2,800 200 200 0 Total fund balance at year end: Fund balance –committed (Reserved for encumbrances ) Fund Balance Unassigned (unreserved) Total This should equal revenues – expenditures (since bal fwd in FB was 0) 200 300 500 Revenue – Expenditures = 5,800 – 5,300 = $500 Chapter 3 Granof-5e 40 Example C (alternate style closing) Fund= General Fund Debit Credit JE 6 Reverse original budgetary entry: Appropriations $5,550 Fund balance (unassigned) 50 Estimated revenues 5,600 JE 7 Close revenue, expenditure & encumbrance accounts Revenues $5,800 Expenditures Chapter 3 5,300 Encumbrances 200 Fund balance (unassigned) 300 Granof-5e 41 Supporting Computations – alternate style Reserve for Encumbrances dr cr balance $0 3,000 (3,000) bal fwd 3 4b 2,800 (200) (200) bal fwd 1 6 7 Encumbrances (temporary acct) dr cr balance bal fwd 3 4b 7 3,000 Fund balance (unassigned, unreserved) dr cr balance Total fund balance at year end: Fund Balance –committed 0 50 (50) (Reserved for encumbrances) Fund Balance -Unassigned 50 (unreserved) 300 (300) Total 2,800 200 200 300 500 This should equal revenues - expenditures since balance fwd was zero TRUE Chapter 3 Granof-5e 0 3,000 200 0 5,800 5,300 500 42 City of Houston - Facts Did you know? The final sales tax revenue for FY 2009 was $507 million, 2.4 % more than FY 2008 amount. Sales taxes comprise 21% of the city’s revenue source for governmental activities. Total unreserved fund balance of the General Fund for FY 2009 was $281 million. Chapter 3 Granof-5e 43 Summary Chapter 3 The General Fund and special revenue funds usually require a legally adopted budget before the government can collect revenues from taxes and other sources and incur expenditures. Severe penalties may exist for failure to comply with the budget, so it is imperative that the accounting system facilitate accounting for the budget as well as all other operating transactions. END! Granof-5e 44