Chapter 7

advertisement

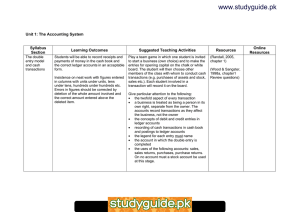

POSTING JOURNAL ENTRIES TO GENERAL LEDGER ACCOUNTS Chapter 7 The General Ledger Posting– The process of transferring information from the journal to the General Ledger General Ledger– Permanent record of accounts organized by account number A.k.a. – Book of final entry Ledger Account Forms – Forms used to record information about specific accounts Used in a manual accounting system Starting a Ledger Page New Account Name, Account Number, Date Existing Account Name, Account Number, Date BALANCE, $$, √ Account Balances When using an Account with a DEBIT Balance If the transaction is a debit, ADD the amounts If the transaction is a credit, SUBTRACT the amounts When using an Account with a CREDIT Balance If the transaction is a debit, SUBTRACT the amounts If the transaction is a credit, ADD the amounts Account Balances Zero Balances Indicated by a line through the normal balance side of the ledger Preparing a Trial Balance Proving the ledger – Comparing the total debit balances with the total credit balances Debits = Credits Trial Balance – A list of all the account names and their current balance A formal way to prove the ledger Finding and Correcting Errors Transposition Error – Two digits are accidentally reversed. The difference is divisible by 9 52 written as 25; difference is 27; 27 is divisible by 9 Slide Error – Decimal point is in the wrong spot 1800.00 becomes 180.00 Correcting Entry – A journal entry necessary to fix a mistake. Used only if error has been posted Do I need to do a Correcting Entry? 3 types of errors Error in a journal that is not posted Error Error in posting when journal is correct Error Error in journal that is posted Correcting Entry