Ford and the European Automotive Market

advertisement

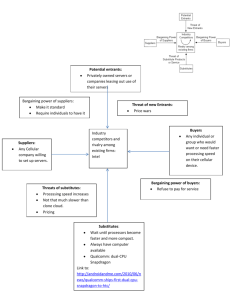

Ford and the European Automotive Market The University of Illinois at Urbana-Champaign Executive MBA Program 1 Executive MBA Case Group Jeff Attwood Jean Baird Maryann Carrero Lucas Chan Susan Krieger Ravi Menon Kent Miller Terry Nichols Randy Short Faculty Advisor: Dr. Jeffrey A. Krug University of Illinois at Urbana-Champaign 2 Analysis Porter’s Five Forces Model The Value Chain Standardization vs. Differentiation Platform Strategy Summary 3 Michael Porter’s Five Forces Model Threat of Substitutes Threat of Entry Threat of Rivalry Power of Suppliers Power of Buyers 4 European Automotive Sector Threat of Substitutes Substitutes Threat of Entry Low Switching Costs Low Priced SubstitutesThreat of Few High Quality Substitutes Rivalry Suppliers MODERATE Power of Buyers 5 European Automotive Sector Threat of Rivalry Threat of Substitutes Power of Suppliers Many Competitors Competitors of Equal Size Low Switching Costs Intense Rivalry High “First Mover” Advantages Competitors High Exit Barriers Low Entry of New Firms Threat of Entry Power of Buyers STRONG 6 European Automotive Sector Threat of Entry Threat of Substitutes Power of Suppliers New Entrants Economies of Scale Technology Advantages Experience Curve Effects Threat of High Brand Loyalty Rivalry High Customer Loyalty High Capital Requirements Buyers WEAK 7 European Automotive Sector Threat of Substitutes Power of Suppliers Power of New Buyers Entrants (Dealers) Profits are Low Threat of Rivalry Purchase in Small Quantities High Switching Costs ? Dealer Size Buyers ? Purchase from Several Suppliers WEAK TO MODERATE 8 European Automotive Sector Substitutes Power of Suppliers Threat of Entry (Material and Labor) High Switching Costs Threat of Few Substitute Products Rivalry Suppliers have Good Reputations ? Number of Suppliers Suppliers to Integrate Forward ? Opportunity Power of Buyers MODERATE 9 European Automotive Sector Forces Threat of Substitutes Threat of Entry Moderate Weak Threat of Rivalry Strong Power of Suppliers Moderate Power of Buyers Weak to Moderate 10 Block Exemption Proposal Spring announcement - Fall implementation Less exclusive selling Less regional control Bypass OEMs 11 Car Rental Service and Parts Leasing/Financing New Car Retailing European Automotive Value Chain Concurrent Infrastructure 12 Car Rental Service and Parts Leasing/Financing New Car Retailing European Automotive Value Chain Insurance 16% 5% 8% 2% 7% 5% 15% 12% 9% 17% Credit Suisse/First Boston: European Automotive Sector January 29, 2002 4% 13 •Composite materials Car Rental Opportunities Service and Parts •Commodity type products Leasing/Financing Threats New Car Retailing European Automotive Value Chain Insurance 16% 5% 8% 2% 7% 5% 15% 12% 9% 17% 4% 14 •Created from outsourcing •Margin squeeze Car Rental Threats Service and Parts Leasing/Financing New Car Retailing European Automotive Value Chain Opportunities •Software systems •Parts sales to others •Consolidation •Increasing power •Sole source •Information sharing •Additional outsourcing Insurance 16% 5% 8% 2% 7% 5% 15% 12% 9% 17% 4% 15 •Block Exemption proposal •Euro transparency •Labor •Imports •Economies of scale •Shorter development cycles 16% •Stronger suppliers 5% 8% 2% 7% 5% Car Rental Service and Parts Leasing/Financing Threats New Car Retailing European Automotive Value Chain Opportunities •Block Exemption proposal •Flexible manufacturing •Information sharing Insurance •Design/provide solutions •Enhance brand/loyalty Insurance •Direct selling 17% 15% •Cost reductions 12% 9% •Differentiation 4% •Standardization 16 16% 5% 8% 2% 7% 5% 15% 12% 9% Car Rental Service and Parts Leasing/Financing New Car Retailing European Automotive Value Chain 17% 4% 17 Standardization vs. Differentiation Cost-Focused Customer-Focused Customization Standardization Differentiation Individualization Advantages/Opportunities Low production and variation dependent costs Reduction in complexity Reduction in resources Advantages/Opportunities Meet customer needs/wants Define/enhance brand More flexible to multibrand strategy Goal: Low cost with high product differentiation while maintaining or extending the identity of the relevant brand 18 Standardization vs. Differentiation How does an automobile manufacturer produce at low cost and keep a high degree of product differentiation while maintaining or extending the identity of its brand? Multi-branding Strategy – breadth of the product line through internal product development or acquisitions Platform Strategy – depth of the product line Badging Strategy – cooperation of two different manufacturers or between brands of one manufacturer 19 Standardization vs. Differentiation Platform Strategy Advantages Reduced complexity Sharing of innovation Economies of scale Increase multi-branding strategy Manufacturing flexibility Disadvantages Product dilution Cannibalization Incompatibilities Risk concentration 20 Standardization vs. Differentiation Badging Strategy Advantages Disadvantages Time advantage Limited autonomous Sharing of development and control investment costs. Competitive advantage Manufacturing and supplier more heavily influence by economies of scale marketing, advertising, Risk minimization dealer networks, and Can fill gaps in multi-branding pricing strategies strategy Mutual transfer of technology and knowhow Supplier time, production and development cost reduced 21 Ford EAO Platform Strategy Pre-1999 Europe Aston Martin Jaguar Lincoln Sub-B Class Ford Mercury Mazda Ka Fiesta B Class Puma Escort C Class Cougar C/D Class Mondeo D Class Scorpio Galaxy VW Sharan SEAT Alhambra M Class (MPV) Windstar People Mover/Cargo SUV/Truck Transit Ranger Explorer Maverick Nissan Terrano 22 Ford EAO Car Platform Strategy Premium Automotive Group Land Rover Volvo Aston Martin Jaguar Europe Lincoln Sub-B Class Ford Mercury Mazda Ka B Class Fiesta XRV Fiesta C Class Focus Options C/D Class D Class Mondeo V70 S-Type E Class S80 F Class LS ? X-Type 23 Ford EAO SUV/MPV Platform Strategy Europe Ford SEAT Alhambra VW Sharan Mazda Land Rover Galaxy MPV Windstar SUV Ford Escape Maverick Mazda Tribute 24 Summary Five Forces Model Threat of Rivalry Power of Buyers and Suppliers Value Chain Collaboration and Information Sharing Design, Development, Brand & Loyalty Exploitation Standardization vs. Differentiation Low Cost with High Product Differentiation Platform Strategy Brand, Platform and Badging Opportunities 25 Ford and the European Automotive Market The University of Illinois at Urbana-Champaign Executive MBA Program 26