Sales Force Management

advertisement

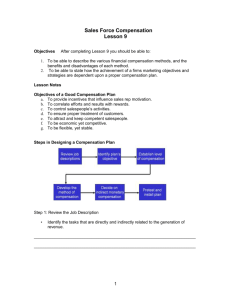

Outcome vs. Behavioral Control Systems Definitions, theories and examples Impact on salespeople Implications for managers Where on the continuum “should” a firm be and why Relationship to compensation 1 Recall from the Jamestown Case Low High Control Control (OUTCOME) (BEHAVIOR) Mfr. Reps Direct with commission, low supervision Direct with salary, high supervision 2 Outcome Control System Salespeople are held accountable for their results but not their behaviors Low control of behaviors by firm extreme is manufacturers’ reps: Jamestown Need objective measures of results 3 Behavior Control System Salespeople are held accountable for their behaviors - the results are expected to follow (at least in the long term) High control of behaviors by firm Firm knows (or believes it know) critical success factors Need to measure these behaviors 4 Some Relevant Theories Agency Theory An approach that describes how principals can control the activities of agents who work for them. Idea is to make the agent’s incentives compatible with the principals goals/outcomes. Transaction Cost Analysis Premise: Outcome control is preferred unless there’s an overriding circumstance. “transaction specific assets”-- ex. Knowledge of brand/ firm/ customers.. Too valuable to replace Organization Theory Behavior vs. outcome vs. clan (socialization control) 5 Outcome Measures Orders Number of orders Average size of orders Number of cancelled calls Accounts Number Number Number Number Number of of of of of active accounts new accounts lost accounts overdue accounts prospective accounts 6 Outcome Measures- A little more sophisticated Volume & volume growth Share by product, customer type, territory Measures of retention: number of repeat orders, customer satisfaction Order size growth Selling cost/sales Sales over quota 7 Behavior Measures Calls Number of calls Number of planned calls Number of unplanned calls Time & time utilization Days worked Calls per day Selling time versus nonselling time 8 Behavior Measures Nonselling activities Letters written to prospects Number of formal proposals developed Advertising displays set up Number of meetings held with distributors/dealers Number of training sessions for distributors/dealers/customers Number of service calls made 9 Impact of Control Systems: How Salespeople Think, Feel, Behave OUTCOME CONTROL (high % commission) Oriented toward personal bottom line “Get off my back” Take customers’ side more than management’s side Generates short-term results: sales, growth, etc. BEHAVIOR CONTROL (high % salary) More oriented toward mutual benefit Relatively cooperative w/ mgmt. Tends to see mgmt’s viewpoint more when balancing customer interests Generates strategic results: customer satisfaction, new product introduction, lower turnover, etc. 10 Impact of Control Systems: How Salespeople Think, Feel, Behave • OUTCOME CONTROL (high % commission) – Long term= next week – Often work harder – More interested in tangible rewards, such as money, trips – More likely to sell on personal relationships, closing techniques – Lean and mean • BEHAVIOR CONTROL (high % salary) – Can think, move in LT fashion – Often work smarter – More interested in nontangible rewards, such as feeling of achievement, personal growth, etc. – More likely to sell on expertise – Kinder, gentler, and fatter 11 Is it really a dichotomy? The world’s a little messier Personal characteristics attitude, initiative/aggressiveness, appearance/manner, citizenship often addressed in hiring decisions Other subjective measures product knowledge, communication skills, ethical behavior, report preparation, selling skills often addressed in training opportunities 12 Managerial Implications of more “behavioral” control Can direct reps to perform activities with unspecified payoffs paperwork, market research can direct to pursue long-term goals new market penetration, customer satisfaction can monitor and redirect activities call patterns, service, nature of presentation, image projected can resolve disputes via authority e.g. which products to emphasize “closer to market” - better knowledge 13 What to consider Environment: demand uncertainty, sales volatility Firm: comfort with risk, current culture, outcome measurement feasibility, behavior measurement feasibility, product characteristics Salesperson: goal congruence, risk aversion, sales “expectancy”, specialization to products/industry/firm 14 Behavioral Control Fits when: You want a loyal sales force turnover is particularly expensive job knowledge, relationship, experience are highly valuable You want an obedient sales force want to know what they’re doing want to direct them to do particular behaviors You can afford to support the overhead 15 Outcome Control Fits when: You want a very motivated sales force effort You are willing to let salespeople be very independent make a good deal of money You are in a hurry You can’t afford or don’t want to support an expensive sales organization 16 How does all this fit with Compensation? How do we use the compensation system to communicate the control system? Focus here is on financial compensation Fixed Salary & benefits At risk Commission,incentive payments or bonuses, sales contests 17 What do different components accomplish? Salary: motivate effort on nonselling activities adjust for differences in territory potential reward experience and competence Benefits satisfy reps’ security needs match competitive offers 18 What do different components accomplish? Commissions: motivate a high level of selling effort encourage sales success Bonus: direct effort toward strategic objectives provide additional rewards for top performers encourage sales success Contests: stimulate additional effort targeted at specific shortterm objectives 19 How are people getting paid? Salary plus commission Salary plus bonus Salary plus commission and bonus Commission only Other Sales Reps Managers 25% 14% 22% 48% 21% 21% 15% 2% 17% 15% Mercer/Compensation & Benefits Review Survey- 1994 20 Compensation Practices Trends From sales volume to profits From new customers & prospecting to customer retention and satisfaction From individual pay to team/group pay From “straight” commission or salary to combination plans 21 Compensating for Customer Retention and Satisfaction In 1994, 10% of 450 companies surveyed by SMM said they link some portion of sales force compensation to customer satisfaction 11% said they are implementing such a plan within the next 12 months Of these companies, 64% say that less than 30% of a salesperson’s compensation is tied to customer satisfaction 22 Compensating for Customer Satisfaction Pros: consistent with quality emphasis fits with trend toward consultative selling and relationship-building account management fits with customer retention objectives (long term profits) fits with higher% of sales coming from lower % of customers Cons: primarily measurement (mostly survey-based) 23 Compensating Teams Individual Component salary individual incentives based on team performance and any individual work Group/team component: pre-arranged % contribution, job responsibilities sales manager observations intragroup performance evaluations contingent on success of all who share a particular client 24 Bonus: Group vs. Individual Consistent finding in compensation literature across job categories: Group/team bonuses become less motivating as the group gets bigger sense of “who cares” social pressure not to free ride decreases So why not give individual bonuses exclusively leads to cut-throat behavior no teamwork 25 Additional considerations Ethical Issues Plans which encourage inappropriate behavior on the part of the rep; Caps on Compensation Quotas 26 Use of Incentive Caps by Industry Food and Beverages 91.7% Soaps, Cosmetics, Consumer Packaged Goods 83.3% Pharmaceuticals 66.7% Telecommunications 42.0% Forest Products 40.0% Publishing 20.0% Office Equipment/Computers 20.0% SOURCE: Lesley Barnes, “Finding the Best Sales Compensation Plan,” Sales and Marketing Management, (August 1986), pp. 46-49. 27 Steps in Designing Compensation Programs Assess the firm’s marketing and sales objectives, and current performance of the sales force Determine aspects of job performance to be rewarded (desired instrumentalities) Assess personal characteristics of salespeople and their valences for alternative rewards Determine most attractive and motivating mix of rewards Decide on most appropriate level of total compensation Decide on form and % of incentive-Commission,Bonus, Contest (short-term incentive awards) Do analysis to determine the cost of program under various scenarios/ modify plan if necessary. Communicate the program to the sales force 28