Lecture 1 - Department of Systems Engineering and Engineering

advertisement

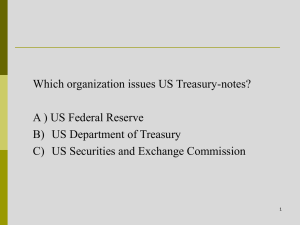

Risk Analysis for Financial Engineering SEEM3580 Tuesday, 10:30am – 13:15pm, ERB407 Lecturer: Prof. Wu,Qi TAs: Leung Cheuk Hang, Ma Shumin, Yan Xing Lecture1: Risks of Financial Institutions Categories of Financial Institutions Sell side:sellers of financial and/or investment services -- brokers: bridging buyers and sellers -- dealers: making markets for securities -- investment banks: IPOs, advisories, researches 2 Categories of Financial Institutions Buy side: buyers of assets and/or financial services -- Mutual funds & pension funds -- Insurance companies -- Corporations, University endowments -- Hedge funds 3 Categories of Financial Institutions Middle side: central banks & regulators -- US Federal Reserve Bank -- Hong Kong Monetary Authority -- PBoC, BoE, ECB, BoJ …… 4 Categories of Financial Institutions Middle side: central banks & regulators -- US Securities and Exchange Commission -- UK Financial Services Authority -- China Security Regulatory Commission 5 Topic 1. Risks of Financial Institutions 1.1 Role of Financial Institutions 1.2 Understanding risk 1.3 Risks faced by financial institutions 6 1.1 Role of Financial Institutions (FIs) Without FIs Cash Corporations Investors Financial claims: Equity or debt claims 7 1.1 Role of Financial Institutions (FIs) The following will decrease the attractiveness of the investment to the investors: Information cost: Too costly for the investors to gather the information of the corporations and sometimes even impossible to do that. (e.g. Apple, JPM) Liquidity risk: Difficult to sell the financial claims in the secondary market. Price risk: The sale price of the financial claim will be less than their purchase price. 8 1.1 Role of Financial Institutions (FIs) With FIs FI (brokers) Investors Cash Financial claims (may not be the same as A) FI (asset transformers) Corporations Financial claims (A) Cash 9 1.1 Role of Financial Institutions (FIs) FI can act as one, or both of the following: Broker: FI acts as an agent for investors to help them to purchase or sale of the financial claims from corporations and helps them to monitor the corporations. (bridge buyers and sellers) Asset transformer: The FI issues financial claims (secondary securities) that are more attractive to investors than the claims directly issued by corporations (primary securities). Because of the popularity, the secondary securities usually have lower liquidity and price risks. (whole sales), e.g. ETF 10 1.1 Role of Financial Institutions (FIs) FI helps investors to reduce Information cost: Delegated monitor - by grouping the funds of the investors, FI has greater incentive to collect information and monitor actions of the corporation. Information producer – through a wide spectrum of secondary securities. Liquidity and price risk: Through the diversification, FI could reduce the liquidity and price risk of its issued primary and secondary securities. 11 1.1 Role of Financial Institutions (FIs) Transaction cost: By aggregating the investors’ funds, FI can purchase the assets in bulk with lower transaction costs. Risk of mismatching the maturities of assets and liabilities: By issuing new forms of financial contracts with different maturities. 12 1.1 Role of Financial Institutions (FIs) Other special services of FIs Transmission of monetary policy In US, Federal Reserve Board adjust the Federal Funds Rate (Fed Funds Rate) to control the supply and demand of banks’ excess reserve and in turn the money supply. (Open market operations) Fed Funds rate: The interest rate at which banks lend their excess reserve to the other banks. (short end) Credit allocation To finance a particular sector of economy which is identified as being in special need of financing such as home mortgages. (GSE) 13 1.1 Role of Financial Institutions (FIs) Intergenerational wealth transfers or time intermediation To transfer wealth between young and old age and across generations. Life insurance Co. and pension funds play a key role in it. Payment service (clearing house, ) For example, check-clearing. Denomination intermediation Through the mutual fund, to allow the investors overcome the constraints to buying assets imposed by large minimum denomination sizes. 14 1.1 Role of Financial Institutions (FIs) Types of financial institutions Depository institutions Insurance companies Securities firms and investment banks Mutual funds and hedge funds Finance companies 15 1.1 Role of Financial Institutions (FIs) Regulation on financial institutions FIs play the key role for the global economic development. Their negative news or failure would cause serious impact to the economy over the globe. Examples: • • • • Bear Stearns Lehman Brothers Citigroup AIG Could you imagine what will happen to Hong Kong if HSBC went bankrupt? 16 1.1 Role of Financial Institutions (FIs) Regulation is not costless Net regulatory burden = Private cost of regulations – Private benefit of the producers of financial services. Example (volker rule, comm, mutul fund, hedge fund) Regulations prohibit commercial banks from making loan that exceed more than 10% of their equity capital even though the loan is profitable. Private cost: Banks loss the investment opportunity. Private benefit: To safeguard the financial health of the bank. 17 1.2 Understanding risk Definition of risk Risk is a condition in which there is a possibility of an adverse derivation from a desired outcome that is expected or hoped for. In financial risk, the desired outcome may be the expected profit from certain assets or investments. 18 1.2 Understanding risk Why manage financial risk? Societal view Modern society relies on the smooth functioning of banking and insurance systems and has a collective interest in the stability of such systems. The role of finance in capital market 19 1.2 Understanding risk Shareholder’s view Proper financial risk management (RM) can increase the value of corporation and hence shareholder value. • • • RM can reduce tax cost. RM gave FI have better access to capital markets than individual investors. RM can make bankruptcy less likely and reduce the bankruptcy cost. So, the firm value can then be increased. The bankruptcy cost is costly in the sense that the assets have to be sold out at a price well below the fair one, completely destroy of reputation and involving huge fees to accountants and lawyers. 20 1.2 Understanding risk Economic capital The economic capital is the capital that shareholders should keep to limit the default (bankruptcy) probability to a given reasonable level (confidence level) over a given time horizon. A good RM could reduce this economic capital. 21 1.2 Understanding risk Asset liability management (ALM) ALM is to minimize the overall level of risks inherited from the assets and liabilities of a financial institution so as to earn adequate return and to maintain a comfortable surplus of assets beyond liabilities. ( how much debt to take on ) 22 1.3 Risks faced by financial institutions Interest rate risk The risk incurred by an FI when the maturities of its assets and liabilities are mismatched. More precisely, we should match duration instead of maturity if the timing of cash flows is taken into consideration. DV01 23 1.3 Risks faced by financial institutions Refinancing risk – the cost of rolling over or reborrowing funds will rise above the returns being earned on asset investments. Assets’ maturity > Liabilities’ maturity Example 1.1 0 Liabilities Liabilities ($100M) ($100M) (Loan A) (Loan B) 1 2 Assets ($100M) 0 1 2 24 1.3 Risks faced by financial institutions At t = 0, FI 1. Borrows $100 million for 1 year with loan interest rate 9% per annum (simple compounding and compounding frequency = 1) (loan A) 2. Buys a 2-year par bond with principal $100 million and coupon rate of 10% per annum (paid annually) 25 1.3 Risks faced by financial institutions At the end of year 1 (t = 1), FI 1. Borrows 1-year loan of $100 million with loan interest rate r% per annum (simple compounding and compounding frequency = 1) (loan B) 2. Repays loan A together with its interest 3. Receives bond’s coupon Net profit = 100M – (100M + 9%100M) + 10% 100M = $1M. It is important to note that r is not known at t = 0. 26 1.3 Risks faced by financial institutions At the end of year 2 (t = 2), FI 1. Receives bond’s principal and coupon 2. Repays loan B together with its interest Net profit = (100M + 10%100M) – (100M + r% 100M) = (10% – r%)100M If r% < 11%, FI makes profit. If r% > 11%, FI incurs loss. 27 1.3 Risks faced by financial institutions Reinvestment risk – the returns on funds to be reinvested will fall below the cost of funds. Liabilities’ maturity > Assets’ maturity Example 1.2 Liabilities ($100M) 0 0 2 1 Assets Assets ($100M) ($100M) (Bond A) (Bond B) 1 2 28 1.3 Risks faced by financial institutions At t = 0, FI 1. Borrows $100 million for 2 years with loan interest rate 9% per annum (simple compounding and compounding frequency = 1) (loan A) 2. Buys a 1-year par bond with principal $100 million and coupon rate of 10% per annum (paid annually) (Bond A) 29 1.3 Risks faced by financial institutions At the end of year 1 (t = 1), FI 1. Pays loan’s interest 2. Receives bond’s coupon and principal 3. Buys 1-year par bond with principal of $100 million and coupon rate c% per annum (paid annually) (bond B) Net profit = – 9% 100M + (100M + 10%100M) – 100M = $1M. It is important to note that c is not known at t = 0. 30 1.3 Risks faced by financial institutions At the end of year 2 (t = 2), FI 1. Receives bond’s principal and coupon from bond B 2. Repays loan together with its interest Net profit = (100M + c%100M) – (100M + 9% 100M) = (c% – 9%)100M If c% < 8%, FI incurs loss. If c% > 8%, FI makes profit. 31 1.3 Risks faced by financial institutions One of the simple ways to hedge the interest rate risk is to match the maturities (duration) of the FI’s assets and liabilities. However, that way is inconsistent with the role of FI being an asset transformer. 32 1.3 Risks faced by financial institutions Market (Trading) risk The risk incurred in the trading of assets and liabilities due to changes in interest rates, exchange rates, and other asset prices. Based on time horizon and secondary market liquidity, the FI’s asset and liability portfolio can be classified into: • • Investment portfolio – contains assets and liabilities that are relatively illiquid and held for longer periods. Trading portfolio – contains assets, liabilities and derivatives contracts that can be quickly brought or sold on organized financial markets. 33 1.3 Risks faced by financial institutions Banking book = Investment portfolio Trading book = trading portfolio 34 1.3 Risks faced by financial institutions The market risk increases as the volatility of the prices of the traded financial instruments increase. The larger of the unhedged (open) trading position, the higher of the market risk will be. 35 1.3 Risks faced by financial institutions Credit risk The risk that the promised cash flows from loans and securities held by FIs may not be paid in full. The examples of credit event include delay, reducing or missing of bond’s coupon and/or principal. Firm-specific credit risk – the risk of default of the borrowing firm associated with the specific types of project risk taken by that firm. 36 1.3 Risks faced by financial institutions Systematic credit risk – the risk of default associated with general economy wide or marco conditions affecting all borrowers. For example, the economic recession. Contagion credit risk – the default of a firm induces the default of the other firms. For example, if GM collapses, it may cause financial trouble or even bankruptcy to its suppliers. Through portfolio diversification, only firm-specific risk and part of contagion credit risk can be diversified away. The systematic risk is still here. 37 1.3 Risks faced by financial institutions Off-balance-sheet risk The risk incurred by an FI due to activities related to contingent assets and liabilities held off the balance sheet. The off-balance-sheet activity (item) is defined as the activity (item) does not involve holding a current asset or the issuance of a current liability. The offbalance-sheet item only appear on the FI’s balance sheet when a contingent event occurs. The advantage of off-balance-sheet item is that it can avoid regulatory costs or “taxes”. 38 39 1.3 Risks faced by financial institutions Future contract is an example of off-balance-sheet item. The underlying asset of the future contract does not appear on the FI’s balance sheet when the contract commences. The asset will only be part of the balance sheet when the asset delivery is really occurred. 40 1.3 Risks faced by financial institutions Foreign exchange risk The risk that exchange rate changes can affect the value of an FI’s assets and liabilities denominated in foreign currency. Example 1.3 A U.S. FI makes a loan to a British Co. in pounds sterling (₤). If the British pound depreciate with respect to USD or the exchange rate (US/pound) decreases, then the return from the loan will drop. 41 1.3 Risks faced by financial institutions To have effective hedging foreign exposure (foreign exchange rate and foreign interest rate risk) requires matching the amount of foreign assets and liabilities and also their duration. 42 1.3 Risks faced by financial institutions Country or sovereign risk The risk that repayments from foreign borrowers may be interrupted because of restrictions, intervention, or interference from foreign governments. One of the examples is the European debt crisis in 2010. (Greece, Iran) 43 1.3 Risks faced by financial institutions Technology and operational risks The technology risk refers to the risk that incurred by an FI when technological investments do not produce cost saving anticipated. The operational risk is defined as the risk that existing technology or back-office support systems may malfunctions or break down. For example, HSBC in London lost customer data disc in April, 2008. It may subject to fine by Financial Service Authority (FSA). 44 1.3 Risks faced by financial institutions Liquidity risk The risk that a sudden surge in liability withdrawals may require an FI to liquidate assets in a very short period of time and at low prices (fire-sale, Lehman). 45 1.3 Risks faced by financial institutions Insolvency risk The risk that an FI may not have enough capital to offset a sudden decline in the value of its assets. It is a consequence or outcome of one or more the risks described before: interest rate, market, credit … risks. 46 1.3 Risks faced by financial institutions Other risks Discrete risks external to the FI such as sudden change in regulation policy and natural disasters like earthquake. Macroeconomic or systematic risk such as increased inflation. 47 1.3 Risks faced by financial institutions Interaction of risks Actually, the risks described above are not independent with each other. They interact with other for certain degree. If 2 risks are positively (negatively) correlated, the sum of their individual effect will underestimate (overestimate) their combined effect. If the interest rate increases, the more difficult for the borrowers to repay the loan to FI. As a result, the credit risk of FI increases. 48