C. Financing a Small

Business

5.00 Explain the financial statements

maintained in a small business.

5.01 Develop the financial

records used in a small business.

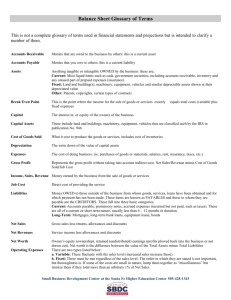

XYZ Balance Sheet

March 31, ____

Assets

Cash

$10,745

Accounts receivable

868

Inventory

5,799

Supplies

433

Total Assets

$17,845

¯¯¯¯¯¯¯

Liabilities

Accounts Payable

Notes Payable

$3,444

5,705

Total Liabilities

$ 9,149

Net Worth

Robin Smith

Total Liabilities & Net Worth

8,696

$17,845

¯¯¯¯¯¯¯

Balance Sheet:

• A financial statement that shows what a

business owns, what it owes, and how

much it is worth at a particular point in

time.

• Components include:

Assets

Liabilities

Net worth

Assets: Items of value owned

by a business.

Types of Assets:

Current Assets: Easily converted into cash

Fixed Assets: Not easily converted into

cash

Intangible Assets: Can not be seen or

touched

Other Assets: Value of life insurance policy

or retirement savings

Liabilities: The amount owed

to others.

Types of Liabilities:

Current: Financial obligations that will be

repaid within one year.

(Accounts payable, notes payable for small

loan, salaries payable, income taxes

payable)

Long-term: Financial obligations that will

take the business more than one year to

repay.

(Mortgage, notes payable for large loan)

Net Worth: The monetary

amount a business owns.

Net worth is calculated by

subtracting a business’

liabilities from assets.

Assets – Liabilities = Net

Worth

XYZ Income Statement

Year Ended December 31, ____

Revenue

Net Sales

$450,000

Cost of goods sold

250,000

Gross Profit on Sales

$200,000

Operating Expenses:

Salaries

$70,000

Advertising

12,000

Rent

14,000

Utilities

3,600

Maintenance

1,200

Insurance

1,500

Miscellaneous

1,000

Total Expenses

Net Income (before taxes)

103,300

$96,700

¯¯¯¯¯¯

Income Statement:

• A financial statement that shows how much a

business has earned or lost during a year.

• Components include:

Gross sales

Net sales

Cost of goods sold

Gross profit on sales

Expenses

Net income

Taxes

Gross sales: The dollar

amount of all sales, usually

within a one-year period.

Net sales: Gross sales minus

returned goods.

Cost of goods sold: The dollar

amount a company pays to

purchase a product for resale.

Gross profit on sales: Net

sales minus the cost of goods

sold.

Expenses: All costs

associated with running a

business except for the cost of

goods sold.

Includes:

Variable expenses: Business expenses

that change month-to-month.

Fixed expenses: Business expenses that

do not change month-to-month.

Net Income: The amount of

money left after all costs and

expenses have been deducted.

Net income is calculated by subtracting total

expenses from gross profit.

This can result in a net profit or loss.

Gross Profit – Total Expenses = Net Income

Taxes: Federal, state, and

local taxes that are owed to

the government.

The tax due is calculated on the net income

which represents the true profit of the

business. Taxes are not considered an

operating expense and are subtracted below

net income on the income statement.

Cash Flow Statement:

• A cash flow statement is a monthly

financial report for internal use that

describes the flow of money into and

out of the business.

• Components include:

Cash receipts

Cash disbursements

Net cash flow

0

0