File

advertisement

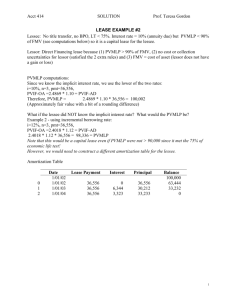

Smoak, Tammy Finance 2 EXSUM Finance II Lease Student Lecture Question: Describe the two primary types of leases. Explain how lease financing affects both financial statements and taxes. Discuss the factors that create value in lease transactions. Top Domain: Health Resource Allocation/ Performance Measurement and Improvement Method of Research/Model: Bloom’s Taxonomy/ Student-led Class (Flipped Classroom) Overview In finance II, students were split into groups of three to develop a lesson plan on a financial concept. My group’s topic was leasing. Leasing is a substitute for debt financing and hence expands the range of financing alternatives available to businesses (and to individuals). One way to obtain the use of assets is to raise debt or equity capital and then use this capital to buy them. An alternative method is to obtain the use of assets is by leasing. • There are two parties to lease transactions: – Lessee: uses the asset and makes the lease (rental) payments • Financing decision for the lessee – Lessor: owns the asset and receives the rental payments • Investment decision for the lessor – Commonly classified into two parties: operating and financial leases Operating Leases • Provides both financing and maintenance • Required to maintain and service the leased equipment • Not fully amortized • Cancellation clause • Lease (rental) payments – Conventional terms – Per procedure terms • Capital leases vs. Operating leases – No maintenance – Not cancelable – Period covers useful life of the asset, hence – Fully amortized • Terms of a financial lease – Full amortization of lessor’s investment – Rate of return on the lease • Close to the percentage rate equal to payment on a secured term loan • End of a financial lease Smoak, Tammy Finance 2 EXSUM – The ownership of the leased asset is transferred from the lessor to the lessee • Sale and leaseback – Real estate – Immediate cash payment in exchange for future series of lease payments • Note: Today most leases are a combination of both financial and operating leases. Tax Effects • Important role for investor-owned and not-for-profit business • Investor-owned (taxable) business – Full amount of lease payment is tax deductible • IRS must determine contract is a genuine lease • Guideline or tax-oriented, lease – Ownership (depreciation) tax benefits accrue to the lessor – Lessee’s lease payments are fully tax deductible • Non-tax-oriented lease – Lessee can only deduct the implied interest portion of each lease payment – Lessee obtains the tax depreciation benefits • Not-for-Profit (Tax-Exempt) Business – Benefit from lower rental payments • Note: The cost of tax exempt debt to not-for-profit firms can be lower than the after-tax cost of debt to taxable firms – Leasing is not automatically less costly to not-for-profit firms • Tax-exempt lease – Special type of financial transaction for not-for profit business • Tax-exempt vs. Conventional lease – Implied interest portion of the lease payment is not classified as taxable income to the lessor – The return portion of the lessor’s payment is exempt from federal income taxes • Financing for Not-for-profit organization is tax-exempt to the lender (lessor is the lender) – Tax-exempt leases provide greater after tax return to lessors • Lower lease payments for lessee Motivations for Leasing • Tax differentials • Alternative tax minimum • Ability to bear obsolescence (residual value) risk • Ability to bear utilization risk • Ability to bear project life risk • Maintenance services • Lower information costs Smoak, Tammy Finance 2 EXSUM • • Lower risk in bankruptcy Leasing is a zero-sum game • Lessor and the lessee have same inputs. (costs, taxes, etc) • Positive NAL creates a negative NPV for the lessor. • Leasing activity is driven by differentials between the lessor and lessee. Tax Differentials • Tax asymmetry – Lessor and the lessee can use tax shields (primary depreciation). – Drives tax rates low, often to zero • Tax differentials between – Not-for-profit providers – Investor-owned lessors Ability to Bear Utilization Risk • Per-procedure lease – The lessor charges the lessee a fixed amount for each procedure performed – Per-procedure risk changes the lessee’s cost from fixed to variable – The lessee’s risk is reduced • Lessor bears the utilization risk – Beneficial to both parties if the lessor is better able to bear that risk Conclusions The Bloom’s Taxonomy model refers to a classification of the different objectives that educators set for students. It divides educational objectives into three "domains": cognitive, affective, and psychomotor. During Finance 2, we built upon finance 1 principles and incorporated data analysis through Microsoft excel. This student-led class allowed me to further apply my understanding of financial concepts and excel functions. I am more apt to remember this information during future financial projects now that I have applied it as a student.