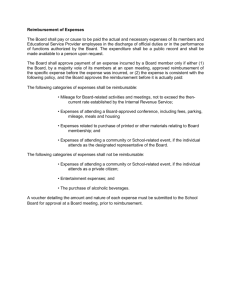

Purchase Vouchers - Texas A&M University

advertisement