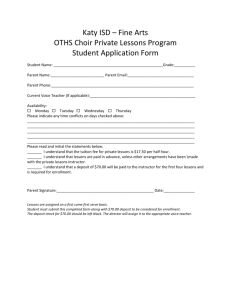

Accounting Procedure of Deposit Accounts

advertisement