ch03

advertisement

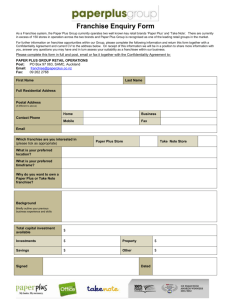

Additional Topics in Income Determination Revsine/Collins/Johnson: Chapter 3 Learning objectives 1. When is it appropriate to recognize revenue before or after the point of sale? 2. Revenue recognition details for long-term construction contracts, agricultural commodities, and installment sales. 3. Revenue principles for franchise sales, right of return, and “bundled” software sales. 4. How GAAP income determination invites “earnings management”, the various techniques used, and recent SEC guidance intended to thwart such activities. 5. How error corrections and prior period restatements are reported. RCJ: Chapter 3 © 2005 2 Recall the criteria for revenue recognition Time of sale is used in most industries Condition 1: The critical event in the process of earning the revenue has taken place. Condition 2: The amount of revenue that will be collected is reasonably assured and is measurable with a reasonable degree of reliability. RCJ: Chapter 3 © 2005 3 Revenue recognition prior to sale: Long-term construction projects Before construction begins, a formal contract has been signed. The buyer is assured and the contract price is specified. Consequently, both revenue recognition conditions are satisfied prior to the time of sale. Condition 1: The critical event is actual construction, thus revenue is earned over time as the project progresses toward completion. Condition 2: Measurability is satisfied because there’s a firm contract with a known buyer at a set price. In addition, construction costs can be estimated with reasonable accuracy so that expenses can be matched with revenues. Percentage-of-completion method: revenue is recognized in proportion to the “work done” each period. RCJ: Chapter 3 © 2005 4 Example: Solid Construction Corp. Contract price is $1,000,000 and construction costs are estimated to be $800,000. Original estimate was $800,000 Gross profit 2005 2006 2007 ? ? ? Total $150,000 How much gross profit must be recognized each year? RCJ: Chapter 3 © 2005 5 Percentage-of-completion for 2005 (Year 1) Step 1: Percentage of completion ratio Step 2: Estimated total contract profit Step 3: Estimated profit earned to date RCJ: Chapter 3 30% = $240,000 = $800,000 Cost incurred Estimated total costs $200,000 = $1,000,000 - $800,000 $60,000 = $200,000 x 30% © 2005 6 Percentage-of-completion for 2006 (Year 2) Step1: Percentage of completion ratio 30% Step2: Estimated total contract profit $200,000 Step3: Estimated profit earned to date $60,000 $60,000 = $544,000 $850,000 Step4: Incremental profit earned RCJ: Chapter 3 64% $150,000 = $1,000,000 - $850,000 $96,000 = $150,000 x 64% $36,000 = $96,000 - $60,000 © 2005 7 Percentage-of-completion for 2007 (Year 3) Step1: Percentage of completion ratio Step2: Estimated total contract profit Step3: Estimated profit earned to date Step4: Incremental profit earned RCJ: Chapter 3 30% 64% 100% $200,000 $150,000 $150,000 $60,000 $96,000 $150,000 $36,000 $54,000 © 2005 8 Percentage-of-completion: Journal entries RCJ: Chapter 3 © 2005 9 Percentage-of-completion: Alternative journal entries RCJ: Chapter 3 © 2005 10 Percentage-of-completion: Balance sheet presentation RCJ: Chapter 3 © 2005 11 Completed-contract method: Long-term construction projects Suppose it is not possible to determine expected costs with a high degree of reliability. Percentage-of-completion then becomes inappropriate because “matching” fails. Completed-contract method postpones all revenue recognition (and expenses) until the period of project completion. RCJ: Chapter 3 © 2005 12 Completed-contract method: Journal entries RCJ: Chapter 3 © 2005 13 Completed-contract method: Journal entries concluded Entry for recognizing income in 2007 at project completion DR Billings on construction in progress $1,000,000 CR Construction in progress $850,000 CR Income on long-term construction contract 150,000 RCJ: Chapter 3 © 2005 14 Revenue recognition prior to sale: Commodities Revenue recognition conditions: Condition 1: The critical event is extraction (mining) or harvesting (agriculture), and occurs before the sale (i.e., formal transfer of title). Condition 2: The precise time at which measurability is satisfied is open to some dispute. Critical Event Time of Sale Revenue recognition could occur when the sales transaction is completed, or earlier at extraction or harvest (i.e., when the critical event is satisfied). RCJ: Chapter 3 © 2005 15 Commodities: Completed-transaction (sales) method Condition 2 is not satisfied until the eventual selling price is known. Accordingly, only the 100,000 bushels sold on Sept. 30, 2005 are included in 2005 revenue. Recognition Matching Revenue (and related expenses) for the remaining 10,000 bushels is postponed to 2006 when those bushels are sold. RCJ: Chapter 3 © 2005 16 Commodities: Market-price (production) method Because producers face an established market price for the commodity, Condition 2 is satisfied continuously. Accordingly, all 110,000 bushels produced in 2005 are included in 2005 revenue under the production method. Recognition Matching Net realizable value As a result, the inventory of 10,000 bushels is shown at market value of $35,000. DR Crop inventory $15,000 CR Market gain on unsold inventory RCJ: Chapter 3 © 2005 $15,000 17 Commodities: Market-price (production) method continued The farmer is engaging in two activities: corn production and commodity speculation (10,000 bushels held in inventory). Subsequent changes in the market price give rise to speculative gains and losses, called inventory holding gains and losses. At the start of 2006, the market price drops from $3.50 to $3.00. The inventory is “marked-to-market” to reflect the loss: DR Inventory (holding) loss on speculation CR Crop inventory RCJ: Chapter 3 © 2005 = 10,000 x ($3.50 - $3.00) $5,000 $5,000 18 Commodities: Market-price (production) method continued Fearing a further market price decline, the farmer immediately sells all 10,000 bushels at $3.00: DR Cost of goods sold CR Crop inventory $30,000 $30,000 DR Cash CR Crop revenue $30,000 $30,000 The inventory book value is $30,000 at the time of sale: Production cost (10,000 x $2.00) $20,000 Market gain at harvest (10,000 x $1.50) 15,000 Inventory holding loss (10,000 x $0.50) ( 5,000) $30,000 RCJ: Chapter 3 © 2005 19 Commodities: Comparison of revenue recognition methods In practice, the completed-transaction method is more prevalent. However, the market price method conforms to GAAP when readily determinable prices are continuously available. Dual advantages of the market price method: Recognizes two income streams—one from farming and another from commodity speculation. Conforms more closely to the income recognition conditions (critical event and measurability). RCJ: Chapter 3 © 2005 20 Revenue recognition after the sale: Installment sales method Sometimes revenue is not recognized at the point of sale even though a valid sale has taken place. High risk of not receiving cash from the buyer (Conditions 1 and 2 are not met). Or there is no reasonable basis for estimating uncollectible accounts (Condition 2 is not met). Conditions 1 and 2 are both satisfied over time as cash collections take place. So, revenue recognition occurs as cash is collected (i.e., as installment payments are made). RCJ: Chapter 3 © 2005 21 Revenue recognition after the sale: Installment sales method example The amount of revenue recognized each period depends on two things: Installment-sales gross-profit percentage Amount of cash collected on installment accounts receivable. RCJ: Chapter 3 © 2005 22 Revenue recognition after the sale: Installment sales calculations Installment Sales Income: Cash collections from 2005 sales Gross-profit % Income recognized Cash collections from 2006 sales Gross-profit % Income recognized $600,000 30% $90,000 $180,000 $340,000 32% $108,800 Total income recognized RCJ: Chapter 3 $300,000 30% © 2005 $288,800 23 Revenue recognition after the sale: Installment sales income statement $340,000 x 32% $600,000 x 30% $300,000 x 30% RCJ: Chapter 3 D © 2005 24 Revenue recognition after the sale: Installment sales journal entries Note: GAAP requires that the interest component of the periodic cash receipts must be recorded separately. RCJ: Chapter 3 © 2005 25 Revenue recognition after the sale: Cost recovery method GAPP allows this approach when: Collections on installment sales occur over an extended period. There is no reasonable basis for estimating collectibility. Under the cost recovery method: No profit is recognized until cash payments from the buyer exceed the seller’s cost of goods sold. After the seller’s cost has been recovered, any excess cash collected is recorded as recognized gross profit. RCJ: Chapter 3 © 2005 26 Revenue recognition after the sale: Cost recovery example $800,000 -600,000 $200,000 RCJ: Chapter 3 © 2005 27 Revenue recognition after the sale: Cost recovery example $1,200,000 -600,000 -200,000 $400,000 Note: The cost recovery method is very conservative because profit is recognized only when the cumulative cash collections exceed the total cost of land sold. RCJ: Chapter 3 © 2005 28 Specialized transactions: Franchised sales Exercise right to sell product or service Franchisor Franchisee Seller Customer Buyer 1. Initial franchisee fee 2. Continuing (periodic) fees Continuing franchise fees are recorded as revenue in the period they are earned and received. The initial franchise fee is comprised of two elements: Payment for the right to operate a franchise in a given area. Payment for services to be performed later by the franchisor. The issue: How much of the initial franchise fee should be recognized as revenue up front by the franchisor? RCJ: Chapter 3 © 2005 29 Specialized transactions: Franchise sales example SFAS No. 45 says: recognize revenue for the initial franchise fee only when all material services and conditions have been substantially performed by franchisor. But, there is no “bright line” test. RCJ: Chapter 3 © 2005 30 Specialized transactions: Recording initial franchise fees 1/1/2005 Sell franchise for $25,000 ($10,000 cash) 3/1/2005 12/31/2005 Franchisor provides trainings, etc Received installment payment plus 8% interests January 1, 2005 DR Cash DR Note receivable CR Earned franchise fee revenue CR Unearned franchise fees $10,000 $15,000 Use of name and right to sell $10,000 $15,000 March 1, 2005 DR Unearned franchise fees CR Earned franchise fees RCJ: Chapter 3 © 2005 Training $7,500 $7,500 31 Specialized transactions: Recording initial franchise fees (continued) 1/1/2005 Sell franchise for $25,000 ($10,000 cash) 3/1/2005 12/31/2005 Franchisor provides trainings, etc Received installment payment plus 8% interests December 31, 2005 DR Unearned franchise fees CR Earned franchise fees $2,500 $2,500 DR Cash CR Notes receivable $5,000 DR Cash CR Interest revenue $1,200 $5,000 $1,200 $15,000 x 8% RCJ: Chapter 3 © 2005 32 Specialized transactions: Recording continuing franchise fees Suppose franchise sales were $100,000 in 2005, and recall that the continuing fee is 2% of sales. The entry for the continuing fee is: DR Cash CR Earned franchise fee revenue $2,000 $2,000 Costs incurred by the franchisor for initial and continuing services are expensed in the same period the franchise revenue is recognized (matching principle). RCJ: Chapter 3 © 2005 33 Specialized transactions: Sales with right of return Sell with right of return Seller Buyer Customer Resale Cash payment or obligation to pay SFAS No. 45 says the following six criteria must be met for a seller to record revenue at the time of sale: Seller’s price to buyer is substantially fixed at the date of sale. Buyer has paid seller, or is obligated to pay and the obligation is not contingent on resale. Buyer’s obligation does not change in the event of theft, destruction, or damage of the product. The buyer has economic substance and is distinct from seller. Seller does not have significant obligations for future performance to bring about resale. The amount of future returns can be reasonably estimated. RCJ: Chapter 3 © 2005 34 Specialized transactions: Bundled sales Oracle sells a database software “bundle” for $1.5 million. The “bundle” includes: Revenue recognized: Customer support $150 Staff training “Free” software upgrades On-going customer support for five years. Upgrade $300 How much revenue should Oracle record up front? Over 5-year period As installed Training $450 When completed Software $600 When delivered and installed SOP 97-2 provides guidance. Oracle’s software and services bundle RCJ: Chapter 3 © 2005 35 Specialized transactions: What Oracle says about bundled sales RCJ: Chapter 3 © 2005 36 Earnings management Determining when revenue has been earned (critical event) and is realized (measurability)—the two revenue recognition conditions—often requires judgment. Managers can sometimes exploit the flexibility in GAAP to manipulate reported earnings in ways that mask the company’s underlying performance. Some managers have even resorted to outright financial fraud (but that’s rare). RCJ: Chapter 3 © 2005 37 Earnings management: Avoiding a loss or earnings disappointment RCJ: Chapter 3 © 2005 38 Popular earnings management devices “Big bath” restructuring charges: Excessive restructuring write-offs that overstate estimated charges for future expenditures. Creative acquisition accounting: Abuses linked to purchased “in-process R&D” that SFAS No. 2 requires to be expensed at the date of acquisition. Miscellaneous “cookie jar reserves” for bad debts, loan losses, warranties and other accruals: Reserve too much in good times and cut back on estimated charges, or even reverse previous charges, in bad times. A convenient income smoothing device. Intentional errors deemed to be “immaterial” and intentional bias in estimates. Premature or aggressive revenue recognition (details to follow). RCJ: Chapter 3 © 2005 39 Revenue recognition abuses The SEC says revenue is earned (critical event) and realized (measurability) when all of the following are met: Pervasive evidence of an exchange agreement exists. Delivery has occurred or services have been rendered. The seller’s price to the buyer is fixed or determinable. Collectibility is reasonably assured. SEC Staff Accounting Bulletin (SAB) No. 104 illustrates troublesome areas of revenue recognition. RCJ: Chapter 3 © 2005 40 Revenue recognition abuses: SAB No. 104 examples Goods shipped on consignment No revenue can be recognized at delivery. Sales with delayed delivery Seller can’t recognize revenue until delivery… except certain buy and hold transactions. Goods sold on lay-away RCJ: Chapter 3 © 2005 Postpone revenue recognition until merchandise is delivered to customer. 41 Revenue recognition abuses: SAB No. 104 examples Non refundable up-front fees Earned as services are delivered over the full term of service engagement. Gross vs. net basis for internet resellers Revenue should be recognized on a “net” basis as commission revenue. Capacity swaps RCJ: Chapter 3 © 2005 Revenue should be recognized over time as the capacity is brought on line and used by customers. 42 Accounting errors Accounting errors and “irregularities” can occur for several reasons: Simple oversight. Unintentional misapplication of GAAP, especially where judgment is required. Intentional attempts to exploit the flexibility in GAAP. Outright financial fraud. Parties charged with discovering accounting errors and irregularities: The company’s internal audit staff and audit committee. External auditors. SEC staff surveillance of filings. Once discovered, accounting errors and irregularities must be corrected and disclosed. Most are corrected through a prior period adjustment. RCJ: Chapter 3 © 2005 43 Accounting restatements: GAO study of irregularities for 1997-2002 Total number of restatement announcements, 1997 - 2002 RCJ: Chapter 3 © 2005 Reasons for earnings restatements, 1997 - 2002 44 Accounting restatements: Share price reaction to announced restatements RCJ: Chapter 3 © 2005 45 Accounting restatement disclosures: An example RCJ: Chapter 3 © 2005 46 Accounting restatement disclosures: Footnote details RCJ: Chapter 3 © 2005 47 Accounting restatement disclosures: Footnote details RCJ: Chapter 3 © 2005 48 Summary The “critical event” and “measurability” conditions for revenue recognition are typically satisfied at the point of sale. There are circumstances—long-term construction contracts, production of natural resources and agricultural commodities— where it is appropriate to recognize revenue prior to the sale. There are also circumstances where revenue recognition may be delayed until after the sale—installment sales and cost recovery methods: There is considerable uncertainty about collectibility. There are significant costs that will be incurred after the sale that are difficult to predict. RCJ: Chapter 3 © 2005 49 Summary concluded Franchise sales, sales with right of return, and bundled sales pose challenging revenue recognition issues. Management can sometimes exploit the flexibility in GAAP revenue recognition rules to hide or misrepresent economic performance. Once discovered, accounting errors and irregularities must be corrected and disclosed. Most are corrected through a prior period adjustment. RCJ: Chapter 3 © 2005 50