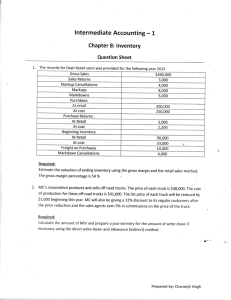

Document

Chapter 9 Inventories: Special

Valuation Issues

Intermediate Accounting 11th edition

COPYRIGHT © 2010 South-Western/Cengage Learning

Lower of Cost or Market

The lower of cost or market rule requires that a company write down its inventory to its market value when the inventory’s utility has declined.

2

Lower of Cost or Market

Inventory: Estimated selling price in completed condition

Less: Estimated costs to complete and sell

Net realizable value (ceiling)

Less: normal profit

NRV less normal profit (floor)

$1,150

150

$1,000

100

$ 900

3

Lower of Cost or Market

4

Lower of Cost or Market

(Ex. 9-1 p. 426)

A company’s unit of inventory has the following characteristics:

Selling price

Packaging cost

$165

10

Transportation cost 15

Profit margin 40

5

Case 1

Lower of Cost or Market

Selling price $165

Cost of completion (10)

Transportation cost (15)

Ceiling (NRV) $140

Normal Profit Margin = 40

Ceiling $140

Normal profit (40)

Floor $100

6

Case 1

Lower of Cost or Market

Selling price $165

Cost of completion (10)

Transportation cost (15)

Ceiling (NRV) $140

Cost =

$110

Current

Replacement Normal Profit Margin=$40

Cost = $120

Market =

$120

Ceiling $140

Normal profit (40)

Floor $100

LCM is the cost of

$110

7

Case 2

Lower of Cost or Market

Selling price $165

Cost of completion (10)

Transportation cost (15)

Ceiling (NRV) $140

Cost =

$110

Current

Replacement

Cost = $150

Normal Profit =$40

Ceiling $140

Normal profit (40)

Floor $100

Market =

$140

LCM is the cost of

$110

8

Lower of Cost or Market

Case 3

Selling price $165

Cost of completion (10)

Transportation cost (15)

Ceiling (NRV) $140

Cost =

$110

Current

Replacement

Cost = $75

Normal Profit Margin=$20

Market =

$120

Ceiling $140

Normal profit (20)

Floor $120

LCM is the cost of

$110

9

Case 4

Lower of Cost or Market

Selling price $165

Cost of completion (10)

Transportation cost (15)

Ceiling (NRV) $140

Cost =

$110

Current

Replacement Normal Profit Margin=$40

Cost = $105

Ceiling $140

Normal profit (40)

Floor $100

Market =

$105

LCM is the market of

$105

10

Case 5

Lower of Cost or Market

Selling price $115

Cost of completion (10)

Transportation cost (15)

Ceiling (NRV) $90

Current

Replacement

Cost = $105

Normal Profit = $10

Ceiling $90

Normal profit (10)

Floor $80

Cost =

$110

Market =

$90

LCM is the market of

$90

11

Case 6

Lower of Cost or Market

Selling price $165

Cost of completion (10)

Transportation cost (15)

Ceiling (NRV) $140

Current

Replacement

Cost = $80

Normal Profit=$40

Ceiling $140

Normal profit (40)

Floor $100

Cost =

$110

Market =

$100

LCM is the market of

$100

12

Lower of Cost or Market

The reduction of the value of the inventory to market and the recognition of a loss are appropriate for both a company’s balance sheet and income statement. GAAP defines assets as “probable future economic benefits.”

When the cost of the inventory exceeds the expected benefits, the lower market value is a better measure of the expected benefits. In other words, an unrecoverable cost is not an asset. A company should recognize the decline in value of the inventory as a reduction in the income of the period in which the loss occurs.

13

13

Estimating Inventory

Two commonly used methods of estimating inventory costs are (1) the gross profit method and (2) the retail inventory method.

14

14

Enhancing the Accuracy of the Gross Profit

Method

1.

A company should adjust the gross profit rate for known changes in the relationship between its gross profit and net sales.

2.

A company may use a separate gross profit rate for each department or type of inventory that has a different markup percentage.

3.

A company may use an average gross profit rate based on several past periods to average out period-to-period fluctuations.

15

Expressing Gross Profit Percentages

Divide gross profit by sales to calculate profit as a percentage of sales.

Gross Profit Gross Profit as a

Sales

=

Percentage of Sales

16

Expressing Gross Profit

Percentages

If the gross margin percentage is expressed as a percentage of cost, it must be converted to a gross margin as a percentage of sales.

Gross Profit as a % of Cost Gross Profit as a

=

Cost + Gross Profit as a % of Cost % of Sales

17

Retail Inventory Method

Another method of estimating inventory is the retail inventory method, which is widely used because it is allowed under

GAAP and for income tax purposes.

18

Retail Inventory Method

Step 1: The total goods available for sale is computed at both cost and retail value.

Beginning inventory

Purchases

Goods available for sale

Cost Retail

$10,000

50,000

$60,000

$ 17,000

83,000

$100,000

19

Retail Inventory Method

Step 2: A cost-to-retail ratio is computed.

Beginning inventory

Purchases

Goods available for sale

Cost-to-retail ratio:

$ 60,000

$100,000

= 0.60

Cost Retail

$10,000

50,000

$60,000

$ 17,000

83,000

$100,000

20

Retail Inventory Method

computed.

Beginning inventory

Purchases

Goods available for sale

Less: Sales

Ending inventory at retail

Cost Retail

$10,000

50,000

$60,000

$ 17,000

83,000

$ 100,000

(80,000)

$ 20,000

21

Retail Inventory Method

Step 4: The ending inventory at cost is computed.

Beginning inventory

Purchases

Goods available for sale

Less: Sales

Ending inventory at retail

Ending inventory at cost

0.60 × $20,000

Cost Retail

$10,000

50,000

$60,000

$ 17,000

83,000

$ 100,000

(80,000)

$ 20,000

$12,000

22

Retail Inventory Method Terminology

Increased selling price to $12

Original selling price ($10)

Cost ($6)

Additional

Markup

Markup

23

Retail Inventory Method Terminology

Total Additional Markups

– Total Markup Cancellations

= Net Markup

Reduced selling price to $10.25

Markup

Cancellation

Cost ($6)

24

Retail Inventory Method Terminology

Markup

Cancellation

Reduced selling price to $9

Cost ($6)

Markdown

25

Retail Inventory Method Terminology

Total Additional Markdowns

– Total Markdown Cancellations

= Net Markdown

Increased selling price to $9.60

Cost ($6)

Markdown

Cancellation

26

Retail Inventory Method

For methods using cost, such as average cost, FIFO and

LIFO, the net markdowns are included in calculating the cost-to-retail ratio.

27

Retail Inventory Method — FIFO

The FIFO method excludes the beginning inventory in determining the cost-to-retail ratio.

FIFO

28

Retail Inventory Method — FIFO

Purchases

Net markups

Net markdowns

Beginning inventory

Goods available for sale

Less: Sales

Ending inventory at retail

Cost Retail

$40 $ 80

$40

20

$60

5

(10)

$ 75

35

$110

(66)

$ 44

$40

$75

= 0.533

Ending inventory at FIFO cost (0.533 × $44) = $23.45

29

Retail Inventory Method — Average Cost

The average cost method includes the beginning inventory in determining the cost-toretail ratio.

Average

Cost

30

Retail Inventory Method — Average Cost

Beginning inventory

Purchases

Net markups

Net markdowns

Goods available for sale

Less: Sales

Ending inventory at retail

Cost Retail

$20

40

$60

$ 35

80

5

(10)

$110

(66)

$ 44

$60

$110

= 0.545

Ending inventory at average cost (0.545 × $44) = $24

31

Retail Inventory Method — LIFO

Separate cost-to-retail ratios for the beginning inventory and the purchases must be calculated for the LIFO method.

LIFO

32

Retail Inventory Method — LIFO

Beginning inventory

Purchases

$20

Net markups $35

Net markdowns $40

= 0.57

= 0.533

$75

Goods available for sale

Less: Sales

Ending inventory at retail

Cost Retail

$20

40

$60

$ 35

80

5

(10)

75

$110

(66)

$ 44

$35 × 0.57 (beginning inventory layer)

$ 9 × 0.533 (added layer)

Ending inventory at LIFO cost

$20.00

4.80

$24.80

33

Retail Inventory Method — Lower of

Average Cost or Market

The lower of cost or market method includes the beginning inventory, but excludes any net markdowns in determining the cost-to-retail ratio.

Lower of Cost or Market

34

Retail Inventory Method — Lower of Average

Cost or Market

Cost Retail

Beginning inventory

Purchases

Net markups

$60

$120

Net markdowns

Goods available for sale

Less sales

Ending inventory at retail

= 0.50

$20

40

$60

$60

$ 35

80

5

$120

(10)

$110

(66)

$ 44

Ending inventory at lower of cost or market (0.50 × $44) =

$22

35

Conceptual Evaluation — Lower of

Average Cost or Market

The lower of cost or market method is accurate only if either markups and markdowns do not exist at the time or if all the markeddown items has been sold.

Under other conditions, the lower of average cost or market produces an inventory value that is less than cost but only approximates the lower of cost or market.

36

Dollar-Value LIFO Retail Method

Information for following slides

37

Dollar-Value LIFO Retail Method

Step 1: Calculate the ending inventory at retail.

Beginning inventory

Purchases

Net markups

Net markdowns

Goods available for sale

Sales

Ending inventory at retail

Cost Retail

$ 8,000

20,400

$28,400

$ 12,000

32,000

3,000

(1,000)

$ 46,000

(29,800)

$ 16,200

38

Dollar-Value LIFO Retail Method

Step 2: Compute ending inventory to base-year retail prices by applying the base-year conversion index.

Ending

Inventory at

Base-Year

Retail Prices

=

Ending

Inventory at Retail

×

Current-Year Price Index

Base-Year Price Index

$15,000 = $16,200

×

100

108

39

Dollar-Value LIFO Retail Method

Step 3: The increase (decrease) in the inventory at retail is computed by comparing the ending inventory with the beginning inventory.

Ending inventory at base-year retail price……

Beginning inventory, 1/1/2010

Increase

$15,000

12,000

$ 3,000

40

Dollar-Value LIFO Retail Method

Step 4: The increase (decrease) in the inventory at retail is converted to current-year retail prices.

Layer Increase at Current-Year

=

Retail Prices

Increase at

Base-Year

Retail

Prices

×

Current-Year Price Index

Base-Year Price Index

$3,240 = $3,000

×

100

108

41

Dollar-Value LIFO Retail Method

Step 5: The increase (decrease) at current-year retail prices is converted to cost.

$3,240 × 0.60 = $1,944

Cost of purchases was $20,400 in 2010 while purchases adjusted for net markups and net markdowns was $34,000 (32,000 +

$3,000 – $1,000)

$20,400 ÷ $34,000 = 60%

42

Dollar-Value LIFO Retail Method

• Step 6: The ending inventory at cost is computed by adding (subtracting) the increase

(decrease) at cost to the beginning inventory at cost. $1,944 + $8,000 = $9,944

Beginning

Inventory at Cost

43

P9-11

•

• P9-11

• 1.

Cost Retail

•

• Purchases

• Less: Purchases discounts taken

• Freight-in

• Net markups ($60,000 - $12,000)

•

• Net markdowns ($15,000 - $4,000)

• $330,000 $637,000

(6,000)

•

•

• Cost-to-retail ratio:

•

• Beginning inventory 100,000

•

• Goods available for sale

• Less: Net sales ($610,000 - $30,000) a

• Ending inventory at retail

• Ending inventory at cost ($237,000 x 0.518)

$430,000

$122,766

•

• a Note: Sales discounts are ignored because they are considered

• to be financing items and not part of the original markup.

48,000

(11,000)

180,000

$817,000

(580,000)

$237,000

$320,000

16,000

$600,000

44