National Income PPT

NATIONAL INCOME

Macroeconomics

TOPIC 1

WHAT IS NATIONAL INCOME?

NI is the value of all goods and services produced in the economy in a year.

It measures the economic performance of a country.

MEASURING ECONOMIC PERFORMANCE

This can be done in 3 ways:

1.

GROSS DOMESTIC PRODUCT (GDP)

This measures the goods and services that are produced in the UK no matter who owns the resources.

2.

GROSS NATIONAL PRODUCT (GNP)

Measures the output produced by UK OWNED resources.

Differs from GDP in that output produced in this country by foreign firms is taken out and output by

UK firms producing abroad is added.

GNP = GDP + Net Property Income from Abroad –

Foreign Income from the UK

3.

NET NATIONAL PRODUCT (NNP)

GNP minus the loss in value of capital goods e.g. machinery. This is called DEPRECIATION

A rise in any of the 3 measures would be deemed to be

ECONOMIC GROWTH , most people would use GDP.

NOMINAL AND REAL TERMS

Each of the 3 measures of economic performance can be expressed in Nominal or Real Terms.

Nominal Terms

Nominal terms is also called money terms. Value is calculated using CURRENT PRICES

However by doing this it makes it difficult to compare one years output to another.

This is because of INFLATION . Which is the general increase in prices. This could mean that NI has gone up due to an increase in price and not an increase in output.

Real Terms

In order to measure changes in output you have to convert the figure into real terms.

This expresses the change in economic performance as if their was no inflation – CONSTANT PRICES

To adjust the figure you have to remove inflation.

Method: Real NI = Nominal National Income divided by 1 multiplied by Price Index of Base Year divided by

Price Index of Current Year

CALCULATING NATIONAL INCOME

There are 3 ways of calculating National Income.

1.

THE OUTPUT METHOD

Adds the value of all goods and services produced by all firms

Must ensure there is no DOUBLE COUNTING – this means counting the same output more than once

2.

THE INCOME METHOD

This is the total amount of incomes earned from the owners of resources e.g. rent, wages, profit

Does not include transfer income such as pensions or benefits as they are not involved in producing output

3.

THE EXPENDITURE METHOD

This is total expenditure of all individual citizens, firms and the Government on goods and services

It does not include expenditure on imports which are the output of another country

USES OF NI STATISTICS

NI stats which measures economic activity has many uses:

1.

Measure economic growth and changes in standard of living

2.

Aid government decision making – helps assess the state of the economy

3.

Comparison of economic growth and standard of living between countries.

4.

Identify countries that are in need of aid – those with low

NI

5.

Calculate contributions that countries should make to international organisations such as the World Bank and EU

PROBLEMS MEASURING NI

NI stats need to be accurate however there are problems

1.

Errors and omissions – data not collected or calculated incorrectly

2.

Black economy – people don’t show what they earn or

produce – to escape tax or claim benefit

3.

Under-recording of output - some goods and services not included because money doesn’t change hands e.g. housework, barter, DIY

4.

Over-recording through double counting

5.

Over-recording through including transfer incomes

DIFFICULTIES IN USING NI STATS FOR

MAKING COMPARISONS

NI figures are used to make comparisons over time and between countries but there are problems:

1.

Methods of calculating NI may differ over time or between countries

2.

Level of self-sufficiency may differ

3.

Standard of living is measured by income per head so population figures need to be correct as well

4.

Stats need to be adjusted for inflation so inflation figures need to be correct

5.

Stats do not show differences in range, design and quality of products

DIFFICULTIES IN USING NI STATS FOR

MAKING COMPARISONS

6.

Stats do not show differences in working conditions, leisure time or hours worked

7.

No differences in income distribution are shown

8.

Social costs such as pollution are not taken into account

9.

Spending on defence or space research may increase output but does little for standard of living of people

Macroeconomics

TOPIC 1

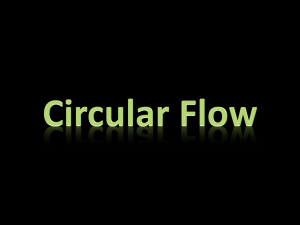

CIRCULAR FLOW OF INCOME

TWO SECTOR ECONOMY

In its simplest form an economy has firms and households.

Households own the factors of production which they provide to firms.

In return firms give households income, such are rent and wages.

Households then spend this income on the output that firms produce.

This expenditure becomes income for firms, which is used to pay incomes to households.

This creates the circular flow of income.

RESOURCES

FIRMS

INCOME CONSUMER

SPENDING

HOUSEHOLDS

OUTPUT

CONSUMER SPENDING

This is how much consumers demand in goods and services over a period of time.

When incomes increase so does consumer spending.

Average propensity to consume

APC = consumption/income

Marginal propensity to consume

MPC = Increase in consumption/Increase in income

Macroeconomics

TOPIC 1

LEAKAGES AND INJECTIONS

INJECTIONS

Injections to the circular flow of income is any spending that is not consumer spending.

Three types of injections exist.

Investment

Exports

Government Spending

INVESTMENT (I)

This is spending by firms. This is normally on capital goods, e.g. machinery.

EXPORTS (X)

This is the money spent by overseas firms and individuals on British goods.

The amount spent is determined by the national income in foreign countries.

Can also be determined by the price and quality of our exports compared to domestic products and the delivery times and after sales service provided.

GOVERNMENT SPENDING (G)

This is the spending in the economy of the public sector.

The level spent is determined by government decisions

LEAKAGES

This is a withdrawal of money from the circular flow of income. It is any money that does not go on as consumer spending.

There are 3 types:

Savings

Imports

Taxation

SAVINGS (S)

This is money that consumers save from their income.

The higher the level of income the higher the proportion saved.

IMPORTS (M)

This is the amount spent by UK firms and individuals on foreign goods and services.

The amount spent on imports is determined by the level of income in the UK, prices of imports compared to UK goods and the quality of the imports.

TAXATION (T)

This is the amount of revenue collected from central and local government.

The amount of tax collected is dependent on the level of income and the level of spending in the economy.

The higher the income the more revenue the government gets. The higher the spending the more revenue the government needs.

Macroeconomics

TOPIC 1

DETERMINING NATIONAL

INCOME

KEYNESIANISM

Named after the economist John Maynard Keynes.

This theory states that it is aggregate demand that determines national income.

Is looking at the DEMAND SIDE OF THE ECONOMY

KEY POINTS

Link between national income and employment – the higher the level of national income, the greater the number of workers needed to produce it.

Full employment level of national income – this is the maximum output that could be made if all resources are employed in producing products which an economy is best at.

NATIONAL INCOME IN A TWO-SECTOR

ECONOMY

A two-sector economy assumes there is no government sector and there is no foreign trade. This is called a CLOSED ECONOMY.

Therefore the only injection is investment and the only leakage is savings.

The equilibrium level is where aggregate demand

(C+I) is equal to income/output or where savings equal investments.

CHANGES IN EQUILIBRIUM

Changes in propensity to save. If consumers save more of their income, then consumption will fall.

This means that Aggregate Demand will fall, income/output will fall, as will employment. National

Income will fall until a new equilibrium is achieved.

Changes in investment. If firms increase investment then Aggregate Demand will also rise.

National Income will increase until a new equilibrium has been reached.

However, any change in investment will result in a bigger change in national income. This is due to the

MULTIPLIER EFFECT.

THE MULTIPLIER

Any change in any component of aggregate demand will have a multiplier effect.

Often explained by looking at the INVESTMENT

MULTIPLIER

The investment multiplier measures the change in national income resulting in a change in investment.

Change in national income = change in investment x multiplier

Assume we have a closed economy with no imports or government.

MPC is 0.9 and MPS is 0.1

A car manufacturer invests £1000 in new equipment. This

£1000 becomes income to households. Households will save £100 and spend £900.

The £900 of consumer spending becomes £900 of income to households. These households will save £90 and spend

£810.

The £810 of consumer spending becomes the income to households, who would save £81 and spend £729

This process continues until national income is back at equilibrium. At this point savings will equal investment. In this example once savings is £1000.

The size of the multiplier is dependent on the % of income that is spent and % saved with each round of income.

All depends on the marginal propensity to save

(MPS).

MPS = Change in savings

Change in income

Multiplier = 1

MPS or 1

1-MPC

If the MPS is 0.1 then the multiplier would be 10. This means that national income would increase by ten times the amount of the increase in investment.

In our example this means that the new equilibrium of national income would be £10000 more than it was before.

Savings would have increased by £1000 to equal the increase in investment.

NATIONAL INCOME IN AN OPEN

ECONOMY

An open economy means that there is government activity and international trade.

This changes the components of aggregate demand.

AD in a closed economy is C+I

AD in an open economy is C+I+G+(X-M)

Equilibrium is still when AD equals income/output.

Or where leakages = injections. However it is more than just savings and investments.

In an open economy leakages are Savings (S), Imports

(M) and Taxation (T) and injections are Investment (I),

Exports (X) and Government Spending (G).

THE MULTIPLIER IN AN OPEN

ECONOMY

The theory of the multiplier remains the same.

Any increase in an injection will lead to a bigger increase in national income.

However, this time it is not only Investment that might have a multiplier effect; it is also Government

Spending and Exports.

Working out the multiplier is still the same, however, this time you have to take in to consideration not only

MPS, but also Marginal Propensity to Import (MPM) and the Marginal Rate of Tax (MRT).

Therefore the multiplier can be worked out as:

1

1-MPC or 1

MPS+MPM+MRT

THE IMPORTANCE OF THE

MULTIPLIER

An increase in any injection into the circular flow of income will increase national income by more than the increase in injection.

A decrease in any injection will decrease national income by more than the initial decrease.

MONETARISM

This theory differs from Keynesianism as this believes that the main determinant of national income is aggregate supply not aggregate demand.

They believe that it is the quantity of resources available and how productive they are.

Keynesians believe that demand creates supply

Monetarists believe that supply creates demand.

QUANTITY AND EFFICIENCY

Monetarists believe that an economy can increase the quantity and efficiency of its resources if it has the following characteristics.

1.

Private enterprise – having competitive markets, with little government involvement. Producers will be profit driven.

2.

Low taxes on incomes – having high taxes does not encourage firms to earn high profits and discourages workers from earning high incomes.

3.

A flexible labour market – it should be easy for firms to change level of wages and staffing dependent on demand. There should be low unemployment benefit.

4.

Governments should keep regulations to a minimum – this is very important if it would add to the costs of a firm.

5.

Governments should concentrate its efforts on improving the quality and efficiency of the workforce through training and education.

TRADE CYCLES

UNIT 2

TOPIC 1

Every economy will see income and employment fluctuate regularly over time.

These fluctuations are called BUSINESS CYCLES or

TRADE CYCLES.

An economy can be experiencing one of four cycles.

1.

PEAK OR BOOM

The following would be experienced:

High income and employment

Wages and profits will be increasing

Consumption and investment spending will be high

There will be inflationary pressure

Demand for imports will be high

Tax revenues will be high

2.

RECESSION

A recession is said to exist when there has been 2 successive quarters of negative growth in real GDP.

This means that real GDP is falling.

Following things may happen:

Income and employment will fall. Although unemployment is a “lagging indicator”.

Wage demands are moderate

Consumption and investment spending falls

Inflationary pressures are moderate

Tax revenues begin to fall and government spending increases. (BENEFITS)

3.

SLUMP

This is when economic activity is low compared to surrounding years.

These things happen:

Mass unemployment

Consumption and investment are low

Few inflationary pressures

Demand for imports are low

Tax revenues are low and large demand for state benefits.

4.

RECOVERY

Income, output and employment begin to increase.

Consumption and investment rise

Inflationary pressures mount as workers feel more confident about asking for increases

Import spending rises

Tax revenues start to rise and spending on benefits falls.