The Operation of Markets PPT

advertisement

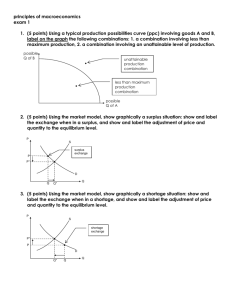

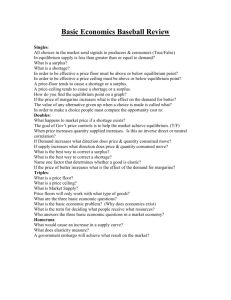

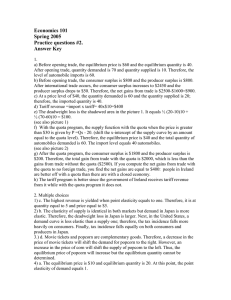

MICROECONOMICS TOPIC 4 Economics 2013/2014 THE OPERATION OF MARKETS WHAT IS A MARKET? This is a place where buyers and sellers come together to exchange goods and services for a price. FREE MARKET This is a market that has: No barriers to entry Price is set in the market by demand and supply, firms accept this price No government intervention EQUILIBRIUM PRICE Price in a free market is called the equilibrium price. It is where demand and supply are equal. The market is cleared, no unsold stock (surplus) or unhappy customers (shortage). Can be called the MARKET CLEARING PRICE. Equilibrium Price Price D SURPLUS S P1 P P2 SHORTAGE D S Q Quantity At P1, the market is not in equilibrium. Suppliers are willing to supply more than customers wish to buy. This creates excess supply/surplus in the market. Firms will have to cut production and lower their price in order to get rid of the excess stock At P2, customers wish to buy more of the product than suppliers wish to supply. There is excess demand/shortage in the market. Consumers will compete with each other for what is available by offering a higher price and suppliers will produce more. At P there is no upward or downward pressure on price The market is in equilibrium. CHANGES IN PRICE Equilibrium price will only change if there is a change in a condition of demand or supply. Please note there could be a change in both. An increase in demand, a shift to the right, will lead to a rise in price, A decrease in demand, a shift to the left, will lead to a fall in price. Change in Condition of Demand D1 Price D S P1 P D1 D S Q Q1 Quantity An increase in supply, a shift to the right, will lower price An decrease in supply, a shift to the left, will increase price. Change in Condition of Supply Price D S S1 P P1 S D S1 Q Q1 Quantity REMEMBER!!! In the exam if a question talks about the price in a market, you must draw a market graph, i.e. have demand and supply curves in it. INTERVENTION IN A FREE MARKET 1. Setting a minimum price This is when the government feels that the price in the market is too low. A minimum price is set above the equilibrium price. However, it can create a surplus in the market. MINIMUM PRICE Price D S MINIMUM PRICE P D S Q Quantity EXAMPLES OF MINIMUM PRICE The Common Agriculture Policy of the EU. Set a minimum price for agricultural products produced in the EU. The setting of the Minimum Wage for low paid workers. Can however create unemployment. 2. Setting a Maximum Price The government sets a price below equilibrium price when it feels the market price is too high. This may have been done to help low income consumers or part of an anti-inflation strategy. It can lead to a black market due to excess demand in the market. MAXIMUM PRICE Price D S P MAXIMUM PRICE D S Q Quantity 3. Imposing Expenditure Taxes This has the same affect as an increase in cost of production. Producers will raise their selling price in order to covered the increased cost. Supply will shift to the left and a new equilibrium price will be determined. How much they can pass on to the consumer depends on the elasticity of demand. 4. Giving Subsidies This has the opposite affect of a tax. Given to encourage supply and lower prices. E.g. rural bus services It reduces cost of production and therefore lowers price and shifts supply curve to the right. 5. Quota This is when the government intervenes and restricts the number of products supplied to the market. For example fishing quotas that limits how much fish can be caught. QUOTA QUOTA Price D S P1 P D S Q Quantity