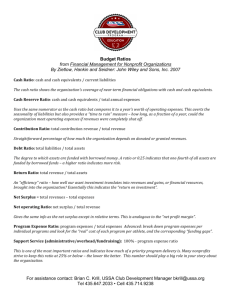

The Complete

Income Statement

Presentations for Chapter 13 by Glenn Owen

Key Points

Economic consequences associated with reporting

net income.

A framework for financing, investing, and operating

transactions.

Categories that constitute the complete income

statement and how they provide measures of income

that address the objectives of financial reporting.

Intraperiod tax allocation.

Earnings per share disclosure on the income

statement.

Economic Consequences

Income as a measure of company performance

Income’s affect on stock prices

Income’s affect on bond prices

Elements of the

Financial Statements

Assets

Liabilities

Equity

Investments by owners

Distributions to owners

Comprehensive income

Revenues

Expenses

Gains

Losses

Classifying Financing, Investing,

and Operating Transactions

Financing and Investing

Transactions

Operating

Transactions

Income

Statement

Balance Sheet

1

2

3

4

1. Exchanges with stockholders

2. Exchanges of liabilities and stockholders’ equity

3. Issues and payments of debt

4. Purchases, sales, and exchanges of assets

5. Revenues and expenses

5

Classifying Operating

Transactions

Transitory

Group C

Gains and losses due

to change in

accounting

principles

Extraordinary

items

Persistent

Group B

Group A

Revenues and Normal and recurring

expenses from

operating revenues

activities not

and expenses

germane to a

company’s primary

activity

Disposals of

segments

Other revenues

and expenses

Disclosure and Presentation

Operating revenues and expenses: usual and frequent

Other revenues and expenses: unusual or infrequent

Disposal of a business segment

Extraordinary items: unusual and infrequent

Changes in accounting principles

Earnings-Per-Share

Disclosure

Separate EPS disclosure for:

– Net income from continuing operations (after tax)

– Disposals of business segments

– Extraordinary items

– Changes in accounting principles

Calculation

– Separate dollar amount (from above categories)

divided by number of

common shares outstanding

Diluted earnings per share

Review Problem

Machinery with an original cost of $14,000 and a

book value of $11,000 was sold for $9,000.

(Unusual but not infrequent)

Cash (+A)

Accumulated Depreciation (+A)

Loss on Sale (Lo, -SE)

Machinery (-A)

Sold machinery.

9,000

3,000

2,000

14,000

Review Problem

A separate line of business (segment) was sold on March

14, 2003, for $18,000 cash. The book values of the assets

and liabilities of the segment as of the date of the sale were

$10,000 and $4,000, respectively. The business segment

reported revenues of $18,500 and expenses of $14,000.

Gain on

Revenues

Income

Cash

(+A)

Summary

Sale

of the

(-Ga,

Segment

(E,

-SE)

-SE)

18,500

18,000

1,530

4,080

Liabilities

Expenses

Income

(-L) Tax

ofLiability

the Segment

(+L)

4,000 14,000

1,530

4,080

Recognized

Income

Assets

income

(-A)

Summary

tax liability ($12,000

related tox2003

34%).operations

10,000

4,500

Recognized

($4,500

Gain

x 34%).

on

business

Sale (Ga,

segment

+SE) income.

12,000

Sold business segment.

Review Problem

On September 12, 2000, Panawin retired, before maturity,

outstanding bonds with a face value of $120,000, for a cash

payment of $130,000. The bonds were originally issued at a

premium, and the unamortized premium as of the date of

retirement was $3,000. (Extraordinary)

IncomePayable

Bonds

Tax Liability

(-L) (-L)

Unamortized

Loss onPremium

Retirement

(-L)(-Lo, +SE)

Loss on Retirement

Recognized

tax benefit

(Lo,($7,000

-SE) x 34%).

Cash (-A)

Retired outstanding bonds.

120,000

2,380

3,000

7,000

2,380

130,000

Review Problem

The company changed its inventory flow assumption

from the last-in, first-out (LIFO) to first-in, first out

(FIFO). This change increased the ending inventory

balance for 2003 by $8,000.

Income from

Inventory

(+A)

Accounting

8,000

Change

Income

(-Ga,from

-SE)

2,720

Income

Accounting

Tax Liability

Change

(+L)

(Ga, +SE)

Recognized additional

change from

taxLIFO

liability

to FIFO.

($8,000 x 34%).

8,000

2,720

COPYRIGHT

Copyright © 2003, John Wiley & Sons, Inc. All rights reserved.

Reproduction or translation of this work beyond that permitted in

Section 117 of the 1976 United States Copyright Act without the

express written permission of the copyright owner is unlawful.

Request for further information should be addressed to the

Permissions Department, John Wiley & Sons, Inc. The purchaser

may make back-up copies for his/her own use only and not for

distribution or resale. The Publisher assumes no responsibility

for errors, omissions, or damages, caused by the use of these

programs or from the use of the information contained herein.