CLASS REVIEW (Chp 5

advertisement

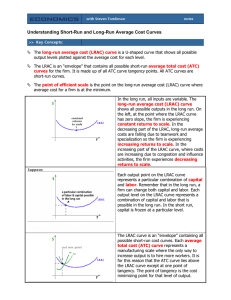

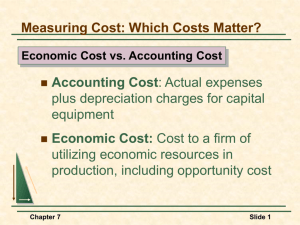

ECON 301 SUMMER 2004 XUE QIAO CLASS REVIEW (Chp 5-Chp 7) June 23, 2004 Chapter 5: Applying Consumer Theory ► Deriving demand curve: For any given price, we can apply consumer constrained choice to derive the optimal consumption bundle. Find the combination of ( px , Qx ), and plot it, then we derive the demand curve. --------To derive it numerically, use formula MRS MRT which can also be rewritten as MU X PX MU Y PY The above formula will derive a equation about optimal consumption bundle, then put this equation back into budget constraint, then we can find ( x , y ). ► Income change: cause Budget constraint to shift. --------------- optimal consumption --------------- Income-consumption curve --------------- Engle curve: upward sloping implies normal good, downward sloping: inferior good. QY --------------- Income elasticity: : >0, then normal good Y Q <0, then inferior good. ► Price change: Total effect = substitution effect + income effect --------------- Decompose TE into SE and IE: Step 1: draw a budget line BL* parallel to the new BL, and tangent to Initial indifference curve, then we have a new tangent point e*. Step 2: The movement from e0 (the tangent point between initial IC and Initial budget constraint) to e measures the SE. Step 3: The movement from e* to e1 ( the tangent point between new BC And new IC) measures the IE. Note: Be careful about the direction. SE= e e0 IE= e1 e TE= e1 e 0 --------------- Consider the case when price of good x drops: Normal good: SE: Q 0 IE: Q 0 Then TE >0 Inferior good: SE: Q 0 IE: Q0 Then TE > 0 if | SE || IE | TE < 0 if | SE || IE | (Giffen good) ► Derive Labor supply curve --------------- H=24-N --------------- Derive leisure demand curve by applying consumer constrained choice --------------- Labor supply =24-demand curve of leisure --------------- Properties of leisure decides the shape of labor supply curve When wage is low, people view leisure as an inferior good: W increases, labor supply increase When wage is high, people view leisure as a normal good: W increases, labor supply decrease So labor supply will increase first then start to decrease, i.e., upward Sloping first, then downward sloping. Chapter 6: Firm and production ► Production function is defined as the maximum output by using existing inputs, so this definition implies efficient production process. ------------ short-run: capital is fixed ------------ long-run: labor and capital can both be varied. ► Short-run production: ----------- TP, MPL ,AP ----------- the shapes of these three definitions ----------- properties of these three definitions and how to show them graphically ----------- Diminishing marginal returns: MPL is decreasing when L increases. ► Long-run production: ----------- isoquant: q f ( L, K ) MPL , and MRTS is decreasing MPK ----------- shape of isoquant: straight line: perfect substitutes right-angle : perfect complement convex: imperfect substitutes ----------- slope of isoquant: MRTS ► Return to scales: f (tK , tL) tf ( K , L ) IRS ----------- Def: f (tK , tL) tf ( K , L ) CRS f (tK , tL) tf ( K , L ) DRS ----------- Tell the “return to scales” from graph: given several isoquants and corresponding inputs bundles. ----------- Return to scales can be varied across firm’s size: IRS for small CRS for moderate DRS for large Chapter 7: Costs ► Measuring cost: economical cost=explicit cost + opportunity cost ► Short-run cost: capital is fixed, so we have a nonzero FC. ----------- 7 Defs: FC, VC, TC, AFC, AVC, AC, MC TC=VC+FC, AC=AVC+AFC, AFC=FC/Q, AVC=VC/Q, TC MC= Q ----------- Properties of these 7 curves and relationship among them ----------- Be able to show them graphically. ----------- Effect on cost of a government specific tax & franchise fee. ► Long-run cost: FC=0 ----------- isocost line: C wL rK w ----------- slope of isocost: r w r or Lowest isocost line or Last dollar rule. ----------- Shape of Long-run cost(LRC), Long-run Average cost(LRAC), MC -------- depends on “return to scales”: CRS: LRC: upward-sloping straight line LRAC & MC: constant IRS: LRC: increasing, but slope is decreasing LRAC & MC: decreasing DRS: LRC: increasing, but slope is increasing LRAC & MC: increasing -------- the part where LRAC is decreasing is called “economies of scale” increasing “diseconomies ….” Constant “ no economies …” ------------ Long-run expansion path and short-run expansion path Read practice IV. ----------- derive the cost-minimizing bundles of inputs: MRTS ►