On the Rapid Calculation of the Price of Options Embedded in

advertisement

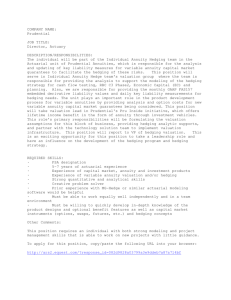

The Effect of Policyholder Transfer Behavior on the Value of Guaranteed Minimum Death Benefits Eric R. Ulm1 Georgia State University JEL Classification: G13 Keywords: Abstract Variable annuity contracts frequently include both Guaranteed Minimum Death Benefit options and options to transfer funds between fixed and variable accounts. We model the difference between fixed and variable rates as the primary determinant of policyholder transfer behavior. We find that people tend to transfer their money into variable accounts at about 39% of the rate that would be required to maintain constant percentage rebalancing, but with the opposite sign. If these transfers are not taken into account, the GMDB options on the variable accounts will be overvalued and over hedged. Ignoring this effect can have a substantial impact on the size of the futures portfolio needed to hedge this risk and a non-negligible impact on the earnings of the variable annuity portfolio. 1 Eric Ulm, FSA, is an Assistant Professor in the Department of Risk Management and Insurance, J. Mack Robinson College of Business, Georgia State University, Atlanta, GA. Phone: 404-463-4809. E-mail: inseuu@langate.gsu.edu. 1. Introduction Insurance contracts often contain two types of options, financial options and “real” options. Over the last ten to twenty years, insurance companies have become more adept at recognizing and hedging the financial options embedded in their contracts. One such option is the guaranteed minimum death benefit, or GMDB, embedded in variable annuity contracts. A GMDB pays the maximum of variable annuity contract value or initial premium on death. This acts as a put option on the fund with a random exercise time, the moment of the policyholder’s death. These options have been examined in some detail in, for instance, Milevsky and Posner (2001), Hardy (2003), Ulm (2004) and Ulm (2008). The valuation of these options is straightforward using numerical methods, and insurance companies have been steadily developing and implementing strategies for delta hedging the options. Less recognized, however, are the real options available to policyholders and how they interact with the financial options in the contracts. Milevsky and Salisbury (2001) have looked at the policyholder option to surrender a contract that is out-of-the-money and replace it with a new at-the-money contract. Ulm (2006) has looked at the option policyholders have to transfer money between funds that have different risk profiles. Both of these papers assume optimal exercise of these real options on the part of policyholders. The assumption of optimal exercise is usually considered reasonable in the case of tradeable options. In this situation, most market participants will be knowledgeable and exercise optimally, and the other participants will find it more cost effective to sell the option than to exercise it when they desire to cash out their position. On the other hand, optimal exercise is not considered reasonable when participants own assets that cannot be traded. Residential mortgages with prepayment options are one example. A number of models of mortgage prepayments exist (see, for example, Richard and Roll (1989), Schwartz and Torous (1989) or Hayre and Rajan (1995)), which do not posit optimal behavior on the part of the homeowners. Also, insurance companies regularly use nonoptimal policyholder lapse and transfer behavior in their pricing, cash flow testing and asset-liability management models. 2. The Model of Real Policyholder Transfer Behavior First, we will address the issue of whether policyholders tend to rebalance their portfolios to maintain a constant percentage in fixed and variable accounts, as recommended by financial planners, or they choose an initial allocation and then transfer rarely, allowing both accounts to grow independently at their separate rates. To answer this question, we used data supplied by Morningstar Inc. They report quarterly data on the breakdown of variable annuity assets between equity, fixed, balanced, bonds and money market funds, as well as quarterly returns on all classes except fixed. The return on fixed accounts can be inferred from NAIC Annual Statements. We assume that the fixed account contains the fixed and money market funds and the variable account contains the equity, bond and balanced funds. This information is available from 1st Quarter 1998 to 4th Quarter 2006. If the hypothesis of constant percentage rebalancing were true, you would expect the percentage in variable funds in one quarter to be the same as in the previous quarter. We find that the square root of the average squared deviation of this prediction is 0.0235 or that this hypothesis typically mispredicts the variable funds by about 2.35%. To test the “buy and hold” hypothesis, we assumed that the fund performance agreed with that supplied by Morningstar Inc. and that there were no transfers. In this case, the square root of the average squared deviation of this prediction is 0.0112 or this hypothesis typically mispredicts the variable funds by about 1.12%. Table 1 contains the values of the variable account percentages and the two predicted percentages. These values are displayed graphically in Figure 1. It is clear from the graph that the “buy and hold” hypothesis predicts the account percentages better than the rebalancing hypothesis, especially in rapidly changing markets as was true in late 2002 and early 2004. It is also evident from the graph that both hypotheses underpredict the magnitude of the change in the variable account percentage. In the falling market of late 2002, both hypotheses predict more variable funds than are actually found, whereas in early 2004, both hypotheses predict fewer variable funds. This means that, relative to a buy and hold strategy, policyholders transfer into variable funds when the market is rising, and out of variable funds when the market is falling. This complements previous data on mutual fund sales, which have shown ambiguous results. Ippolito (1992) shows using annual data that investors direct investments toward individual funds that have performed well in the recent past. Warther (1995) studies the full market mutual fund flows and concludes that fund investors “do not follow positive feedback strategies”. That is, they do not in general direct more money to stock funds as a result of those funds performing well. Edelen and Warner (2001) find mutual fund flow responds to lagged returns with a positive correlation over 1 day and negative correlations after 2-3 days. There is still the complication that the base funds from one quarter to the next are not identical. New accounts have been sold, new premium added and some policies have lapsed. We will make the simplifying assumption that new premium is distributed proportionately to existing funds, and that lapses come proportionately from existing funds. 2.1 The Policyholder Transfer Model. We will start with a model of variable annuity fund performance. A percentage p of the funds will be invested in an variable account of size S , itself a stochastic process, and therefore 1 p will be invested in an account earning a fixed rate g . The fund value F obeys the following equation: dF g (1 p) Fdt pF dS S (1) In the case of constant rebalancing, the percentage p is constant. For the buy and hold case, p obeys the following equation, assuming that S is a differentiable function, rather than a Brownian motion: dS dp p(1 p) gdt S (2) If S follows a geometric Brownian motion process, then dS dp p(1 p) gdt p 2 (1 p ) 2 dt S (3) where the second term is present to correct for the drift caused by the quadratic variation in dS . When Equation 2 is treated as an ordinary differential equation, and Equation 3 is treated as a stochastic differential equation, both equations solve for S S0 p0 p (4) S (1 p0 )e p0 S0 gt which is the correct answer in the buy-and-hold case. The derivations of both equations can be found in Appendix A. We will assume transfers are proportional to the difference between the instantaneous difference in fund rates dS gdt . We will also assume that they are S proportional to the percentage in the fund being transferred from, and the fund being transferred into, i.e. proportional to p (1 p ) . This latter assumption is mathematically useful, as well as having some intuition behind it. Those policyholders with 0% in equity or 0% in fixed are unlikely to be making constant transfers. Only those near the middle seem likely to transfer. In addition, if either fund is at 100%, it is impossible to transfer more money into it. This transfer assumption prevents this situation from occurring. Finally, the values of p (1 p ) are between 0.16 and 0.24 when p is in the generally realized ranges from 60% to 80%, so the effect of this assumption is small. This means, in our model, with S differentiable, not stochastic: dS dS dS dp p(1 p) gdt qp(1 p) gdt p(1 p)(1 q) gdt S S S and, if S follows a geometric Brownian motion process, then (5) 1 dS 1 dp p(1 p)(1 q) gdt p 2 (1 p) 2 dt qp(1 p) 2 p q p 2 dt (6) S 2 2 with the last two terms correcting for the drift from the quadratic variation in S as in Equation 3. When Equation 5 is treated as an ordinary differential equation, and Equation 6 is treated as a stochastic differential equation, both equations solve for p S p0 S0 (1 q ) S (1 p0 )e g (1 q )t p 0 S0 (7) 1 q Now, assuming the stock market follows a standard geometric Brownian motion, dS dt dZ S (8) We find from Equations 6 and 8: 1 dp p(1 p)(1 q) g p 2 q 2 p 2 dt p(1 p)(1 q)dZ (9) 2.2 Empirical Determination of the Value of the Transfer Parameter We will now turn our attention to the determination of the transfer parameter q . It can be seen from Equation 9 that a value of q 1 sets dp 0 and therefore q 1 corresponds to constant percentage rebalancing (CPR hereafter). A value of q 0 corresponds by design to the buy-and-hold strategy. Positive values of q imply policyholders transfer into a rising market, and negative values of q implies transfers into a falling market. Table 2 contains 35 quarterly values of p and returns determined by the change in values of the Morningstar catagories over the quarter weighted by the starting percentages. Milevsky and Posner (2001) find an industry average of 115 basis points of asset fees, so S is determined as the returns less 115 bp in asset fees. We can S0 adjust q in Equation 7 to fit these values. We will begin by transforming equation 7 to a linear equation, obtaining: S q ln S0 p(1 p 0 )e gt S 0 gt ln (1 p) p 0 S (10) Performing a regression with slope q and intercept c gives q 0.39 and c 0.0044 with standard errors of 0.10 and 0.0082. The value of q is significant at the 0.001 level with a 95% confidence interval 0.19 q 0.60 . The constant is not significant with a 95% confidence interval 0.0121 c 0.0210 , so there is no evidence of a bias to transfer one way or the other. A plot of the regression is shown in Figure 2. Figure 3 contains a comparison of the percentage of funds that would be predicted if q 0 , the buy and hold strategy, and q 0.39 . The raw data can be seen in table 1. The sum of the squared deviation goes down as you move from right to left across the table. For the CPR model, the sum of the squared deviations is 0.01932 (off by 2.35% on average). For the buy and hold model it is 0.004451 (off by 1.12% on average) and for q 0.39 it is 0.003048 (off by 0.93% on average). A second estimate of the parameters can be obtained by minimizing the sum of the squared deviations. This produces a value of q 0.41 , well within the range given by the linear fit. The sum of the squared deviations is 0.003045, negligibly different from that produced by the best linear fit. 3. GMDB Values under the Constant Percentage Rebalancing and Buy-and-Hold Assumptions. It is relatively straightforward to calculate the values of the GMDB option under the constant percentage rebalancing assumption. The fund value obeys Equation 1 with p constant. If S follows a Geometric Brownian Motion process, this leads to: dF g (1 p) pFdt pFdZ (11) Since p is constant, this is just a Geometric Brownian Motion with variance p . The GMDB can be calculated in the usual way from the integral: f a ( F0 , t ) Xe rw N d 2 ( F0 , w) SN d1 ( F0 , w) w p x()t x (t w)dw (12) 0 where p 2 2 F w ln 0 r 2 X d1 ( F0 , w) p w (13a) and p 2 2 F w ln 0 r 2 X d 2 ( F0 , w) p w Where w (13b) p x()t includes both mortality and lapse decrements (see Hardy 2003). The values of d1 and d 2 are calculated with a variance of p . The calculation of GMDB values under the buy and hold assumption is only slightly more difficult. At any given time, the fixed fund amount is known to be (1 p 0 ) F0 e gt . If this value is larger than the strike, the GMDB value will have no contribution from the put option based on death at time t . On the other hand, if the fixed fund is smaller than the strike at time t , the contribution to the GMDB at that time can be converted to a put option at that time with an adjusted strike price J (t ) assuming an initial stock level of 1, where: J (t ) S 0 X (1 p0 ) F0 e gt p0 F0 (14) The value of the contribution at time t needs be multiplied by p0 F0 . Equation 14 comes S0 from the fact that S MaxX F ,0 Max X (1 p0 ) F0 e gt p0 F0 ,0 S0 S X (1 p0 ) F0 e gt p0 F0 Max 0 S ,0 S0 p0 F0 (15) This leads to the following integral for the GMDB Value: p F f a ( F0 , t ) 0 0 S0 J (w)e t0 rw N d 2 ( J ( w), w) S 0 N d1 ( J ( w), w) 0 w p x()t x (t w)dw (16) where S 2 ln 0 r 2 J ( w) d1 ( J ( w), w) w w (17a) S0 2 r ln 2 J ( w) d 2 ( J ( w), w) w w (17b) and X ln F (1 p 0 ) t0 0 g (17c) The integral in equation 16 is zero if t 0 0 . The next step is to determining the values of f a to be used in hedging. The S calculation of delta in the constant percentage rebalancing case is straightforward. Since p is constant, f a F F f f p 0 a . The remaining partial derivative, a , can be F F S S 0 F calculated numerically from equation 12. The value of in the buy and hold case is a little more difficult, as p can vary as S changes. Therefore, f a F f a p F f p(1 p) f a , with the p 0 a F S p S S 0 F S0 p remaining partial derivatives calculated numerically from equation 16. It requires fewer calculations to calculate f a numerically by increasing and decreasing S by some S small amount, calculating F (1 p 0 ) F0 e gt p 0 F0 S and p S0 p0 S S0 S (1 p0 )e p0 S0 in gt both the up and down cases, and then using equation 16 to calculate the value. 3.1 GMDB Values under q 1, q 0 assumptions. We now tackle the much more difficult problem of calculating the value of the GMDB option for arbitrary values of the transfer parameter q . There are three basic methods of calculating GMDB values. The first is by using an analytic formula. Only a few exact formulas exist (see Ulm 2008), but if the value of the option given death at a specific time t is known analytically, the problem can be solved through integration, as in equations 12 and 16. If the probability distribution of the fund values f F ( y) is known at time t , the GMDB value can be determined by double integration, for example: f a ( F0 ) e rt Max( X y,0) f F ( y) t p x( ) x (t )dydt (18) 0 0 The second method is through simulation. A number of Brownian Motion Paths can be produced, and the fund value determined from Equations 8 and 9. This is equivalent to determining the interior integral in Equation 18 stochastically, and then computing the exterior integral numerically. Unfortunately, this method can take a considerable amount of time. The third method would be to solve the differential equation obeyed by the GMDB: f a f 2 fa 1 rS a 2 S 2 [r x (t ) ( S , t )] f a [ x (t )]Max( X S ,0) t S 2 S 2 (19) either analytically or numerically. For a derivation of this equation, see Milevsky and Salisbury (2001). We implement the first method by finding a good approximation to the probability density of the fund distribution under the transfer assumptions of the model in Section 2. The second method is implemented directly, and acts as a check on the first method. We also derive the differential equation satisfied by the GMDB value under those transfer assumptions. In general, the differential equation is too difficult to solve directly. We first turn our attention to the determination of the fund values F (t ) . It is shown in Appendix B that, under risk neutral growth assumptions, 1 1 q 1 q q 2 p 2 p dt S 2 F (t ) F0 (1 p0 )e r (1 q )t p0 e 0 S 0 t (20) Unfortunately, the value is path dependent in the general case, due to the stochastic integral in the last term. In practice, this isn’t as bad as it at first seems. If q 0 , the stochastic term disappears and equation 20 reduces to the value of the fund in the buyand-hold case. If q 1 , the integral is non-stochastic as p p0 . The integral is also zero when p 0 0 and p0 1 . With so many anchor points, you might expect that replacing the stochastic integral with the approximation e q 2 2 p t 0 2 p dt e q 2 2 p0 p0 dt t 2 0 q e2 2 p02 p0 t (21) would be reasonable. This approximation is exact in the four cases mentioned above. It is very good when q is small or p 0 is near the extremes. Even when p 0 is not extreme, if p remains in the range from 60%-80%, as is typical, and 20% as is typical, the integral would fall in the range e .0048qt e q 2 2 p t 2 p dt 0 e .0032qt . If qt 7.8 , about 20 years at the fitted value of q 0.39 , the integral will fall between 0.9632 and 0.9753, an error of about 1.2%. In fact, the difference between the largest and smallest physically possible values of the integral is only 4.3% after 20 years. We also show the following approximation: 1 1 q S 1 q q2 2 p02 p0 t r (1 q ) t F (t ) F0 (1 p0 )e p0 e S 0 (22) agrees very well with simulated results, both in the determination of fund values along simulated Brownian paths, and in the determination of option values. The error is certainly substantially less than the error introduced in the determination of the input parameters q and . The approximation could be improved somewhat by using a weighted average of the beginning value of p , that is, p 0 , and the ending value of p , which can be determined from S from Equation 7. This increases the complexity of the calculations considerably, with little gain in the accuracy of the approximation. Now that the fund value is known as a function of S , we can use the lognormal density of S to compute the option value from the integral in equation 18. The integral then becomes: 1 f a ( F0 ) e rt Max ( X F0 e 0 q 2 p0 (1 p0 ) t 2 1 q ( r )(1 q ) t r (1 q ) t p0 e 2 e (1 q ) t y ,0) (1 p 0 )e 2 1 2 e y2 2 t p x( ) x (t )dydt (23) which can now be evaluated numerically. Figure 4 shows the results of this evaluation for typical parameters. While there is a substantial difference between the values for the CPR and buy-and-hold cases, there is little added effect from increasing q above zero. We now turn our attention to the calculation of the delta values. As before, f a F f a p F f p(1 p)(1 q) f a p 0 a F S p S S 0 F S0 p with the partial derivatives with respect to S obtained from equations 1 and 6. The remaining partial derivatives can be evaluated numerically from equation 23, by (24) increasing and decreasing F and p independently by some small amount. It requires fewer calculations to simply increase and decrease S directly, calculate the corresponding F and p from equations 7 and 24, and then calculate the derivative numerically from equation 25. Figure 5 shows the results of this evaluation for typical parameters. Figure 6 shows the delta values as a percentage of fund value. The effect on the delta values is somewhat larger than the effect on the GMDB values themselves, through the existence of the second term in Equation 24. We next determine the value of the options through simulation. We ran 1000 simulations of the Brownian process Z with a time step of 0.01 for 100 years. At each time step, the stock level was determined from: St e 2 r 2 t Z (25) p was determined from Equation 7, and the fund level F was determined from Equation 1. The integrated results agree very well with the simulated ones as can be seen in Figure 7 and Figure 8. In addition, Figure 9 shows a comparison of the cumulative probability distribution of F after 20 years determined through simulation with that obtained from Equation 22. At this scale the lines are indistinguishable. Figure 10 shows a closer view of the most relevant area. Finally, there is the possibility of valuing the GMDB from the differential equation that the value satisfies. We will start from Equations 9 and 11 and then construct a riskless portfolio. If f a is any function of the state variables F and p and time, then: df a ( F , p, t ) 1 2 fa f a f f 2 fa 1 2 fa 2 2 dt a dF a dp dF dFdp dp 2 t F p Fp 2 p 2 2 F (26) We can then substitute Equations 9 and 11 for the differentials dF and dp into Equation 26. The second order terms only affect the results through the dZ 2 dt terms. This leads to: f f 1 f df a a g (1 p) pF a p(1 p)(1 q) g p 2 q p 2 a F 2 p t 2 2 2 fa 2 fa 1 2 2 2 2 fa 2 2 2 2 (1 q) p F p ( 1 p )( 1 q ) F p ( 1 p ) dt 2 Fp 2 F 2 p 2 f f pF a p(1 p)(1 q) a dZ F p (27) Then, we set up the portfolio f a S to hedge, so d df a dS df a Sdt SdZ (28) And then, if we require the dZ term to vanish, p F f a p (1 p )(1 q) f a S F S p (29) Since is riskless, d rdt . Substituting Equations 29 and 30 into this relationship and canceling the dt leads to: f a f 1 f g (1 p) rp F a p(1 p)(1 q) r g p 2 q p 2 a t F p 2 2 fa 1 2 2 2 2 fa 2 2 p F p ( 1 p )( 1 q ) F 2 Fp F 2 (1 q) 2 2 2 f a p (1 p) rf a 2 p 2 2 2 (30) Equation 30 represents the value of the put at given time of death t . An analysis similar to that in Ulm (2006) for the value of the full GMDB yields: f a f 1 f g (r g ) p F a p(1 p)(1 q) r g p 2 q p 2 a t F 2 p 2 fa 1 2 2 2 2 fa 2 2 p F p ( 1 p )( 1 q ) F 2 Fp F 2 p 2 (1 p) 2 (1 q) 2 2 2 f a r x (t ) ( F , t ) f a x (t ) Max ( X F ,0) (31) 2 p 2 This equation could be solved by working backwards in time in a 3 dimensional lattice. It can also be made easier by assuming the fund growth rate g is equal to the risk free rate, and that the forces of mortality and lapse are constant, which eliminates the f a t term. This leads to: (r ) f a rF f a 1 f p(1 p)(1 q) q 2 (1 q) p 2 a F 2 p 2 fa 1 2 2 2 2 fa 2 2 p F p ( 1 p )( 1 q ) F 2 Fp F 2 p 2 (1 p) 2 (1 q) 2 2 2 f a Max ( X F ,0) 2 p 2 (32) Equation 32 can be put into a form resembling the heat equation by using the substitutions: F 1 q (1 p) X ln (33a) 1 1 q p ln 1 p (33b) And f a ( X , p) H ( , )e 16( r ) 2 2 2 (33c) This leads to: e (1 q ) 2r (1 q) q ( 1 q ) 2 1 e (1 q ) (1 q) e 2 H 2 H 2 2 16( r ) 2 2 2 Max 1 e e (1 q ) 1,0 (34) which can be solved numerically, or through Green’s functions and Sturm-Liouville theory (see Polyanin 2002, pg. 151). In practice, Equation 34 is of limited use, as it is not analytically solvable, and the integral methods of Equation 23 are faster. In addition, it was derived for unrealistic constant force of mortality and lapse assumptions. One advantage of equation 34 is that if the equation is solved on a lattice, many values of f a ( X , p) would be obtained simultaneously. These values could be stored in memory, and values at non-lattice points could be obtained through interpolation. 4. Effect of Transfers on Hedging Effectiveness Insurance companies are in the business of taking on risk. However, they are much more comfortable with risks that are well understood and independent. Mortality risk is the most typical example. In these cases, the law of large numbers will allow the insurance company to make a consistent profit with little actual risk. GMDB riders on variable annuities, however, are based on market risk, which is not diversifiable. Adding more GMDBs to an insurance portfolio will only increase the risk in a falling market, as the GMDB payoffs are not independent. Therefore, insurance companies will often attempt to transfer the market portion of the risk to another entity, either through reinsurance or delta hedging with futures contracts. In this section, we will show how the transfer model should affect hedging strategy, and how serious the consequences of failing to incorporate transfer behavior into the hedging model are. The typical hedging program consists of calculating the dependence of the entire portfolio of GMDB options on the market (i.e., the values of delta) and then buying or shorting futures contracts of the appropriate size to leave the economic value of the company unchanged when the market moves. Figure 5 shows the values of delta that would be calculated under each of the three assumptions (CPR, Buy-and-Hold and q 0.39 ). In this section, we will examine the consequences if an insurance company attempts to hedge on either the CPR or Buy-and-Hold model when the q 0.39 model is actually the correct one. As can be seen in the figures, delta is smallest for the q 0.39 transfer model. This implies that if an insurance company is hedging on the basis of the other two models, it will invest in too many futures contracts, and therefore be over hedged. This may not be that bad in practice, however. Additional futures contracts will lead to additional transaction costs, but there are also some benefits to being slightly over hedged. GMDB options are not the only equity exposure assumed by insurance companies. Asset fees on variable products are also highly dependent on stock market performance, and this is often a larger effect than the GMDB option exposure. Being slightly over hedged will mitigate some of the risk of reduced asset fees, and the magnitude of the error in delta is not large enough to result in the entire company being over hedged. Aside from transaction costs, the overvaluing and over hedging of the GMDB options does not change the long-term earnings of the company. It merely redistributes the earnings to different time periods. It can also be seen from the figures that that advantage of going from Constant Percentage Rebalancing assumptions to Buy-and-Hold assumptions is significant (up to 0.66% of fund value when the fund is at 60% of the strike value). The additional gain from including transfers is smaller (another 0.22% of fund value, which is approximately 0.39 0.71% ), but could easily still be important. If an insurance company has $10,000,000,000 in variable annuity funds with at-the-money GMDB riders, the change in the futures value from a 1% change in the S&P if CPR assumptions are used is $4,003,000. The change from Buy-and-Hold assumptions is $3,431,000 and the change from q 0.39 assumptions is $3,226,000. The effect on the hedge from a change in assumptions could be on the order of $5,000,000 a year, assuming a typical 8% change in the S&P, and even more in years with particularly large positive or negative equity moves. Assuming an operating margin of 20 - 50 bp, which is about $20,000,000 $50,000,000 per year in income, the effect of the incorrect hedge assumptions would be a non-negligible part of the total income of the variable annuity segment, and care should be taken to insure that the futures position is hedging the actual exposure, including transfer effects. 5. Conclusions A model of variable annuity subaccounts where transfers are primarily determined by recent fund returns is a good fit to empirical data on fund allocation percentages. This is consistent with previous studies of mutual funds that show that individual cash flows to mutual funds are positively related to recent fund performance. A model based on these assumptions shows that people tend to transfer their money into variable accounts at about 39% of the rate that would be required to maintain constant percentage rebalancing, but with the opposite sign. If these transfers are not taken into account, the GMDB options on the variable accounts will be overvalued and over hedged. Ignoring this effect can have a substantial impact on the size of the futures portfolio needed to hedge this risk and a non-negligible impact on the earnings of the variable annuity portfolio. 6. Acknowledgements This research was supported, in part, by a research grant from the Robinson College of Business, Georgia State University and by a grant from The Actuarial Foundation. The data on mutual fund percentages and returns was provided by Morningstar Inc. We would like to thank Conrad Ciccotello, Steven Craighead and Ajay Subramanian for useful discussions. References: Edelen, R.M. and Warner, J.B. 2001. Aggregate Price Effects of Institutional Trading: A Study of Mutual Fund Flow and Market Returns, Journal of Financial Economics 59(2):195-220 Hardy, M. 2003. Investment Guarantees, Hoboken, N.J.: John Wiley and Sons. Hayre, L. and Rajan, A. 1995, Anatomy of Prepayments: The Salomon Brothers Prepayment Model, Salomon Brothers. Ippolito, R.A. 1992. Consumer Reaction to Measures of Poor Quality: Evidence from the Mutual Fund Industry, Journal of Law and Economics 35:45-70. Milevsky, M.A., and Posner, S.E. 2001. The Titanic Option: Valuation of the Guaranteed Minimum Death Benefit in Variable Annuities and Mutual Funds, Journal of Risk and Insurance 68(1):93-128 Milevsky, M.A., and Salisbury, T.S. 2001. The Real Option to Lapse and the Valuation of Death-Protected Investments, Conference Proceedings of the 11th Annual International AFIR Colloquium, Sep 2001, pg 537 Polyanin, Andrei D. 2002, Handbook of Linear Partial Differential Equations for Engineers and Scientists, Boca Raton, Fl: Chapman & Hall/CRC. Richard, S. and Roll, R. 1989, “Prepayments on Fixed Rate Mortgage Backed Securities”, Journal of Portfolio Management 15(3):73-83 Schwartz, E. and Torous, W. 1989, “Prepayment and the Valuation of Mortgage Backed Securities”, Journal of Finance 44(2):375-392 Ulm, E.R. 2004. “Rapid Calculation of the Price of Guaranteed Minimum Death Benefit Ratchet Options Embedded In Annuities”, Journal of Actuarial Practice 11, 169195 Ulm, E.R. 2006. The Effect of the Real Option to Transfer on the Value of Guaranteed Minimum Death Benefits, Journal of Risk and Insurance 73(1), 43-69 Ulm, E.R. 2008. Analytic Solution for Return of Premium and Rollup Guaranteed Minimum Death Benefit Options Under Some Simple Mortality Laws, Submitted. Warther, V.A. 1995. Aggregate Mutual Fund Flows and Security Returns, Journal of Financial Economics 39(2-3):209-235. Appendix A. Derivation of Equations 2 and 3, the stochastic equation followed by the variable fund percentage under a buy and hold strategy. Neglecting terms of order 2 or higher: dS pX (t ) 1 S p dp p (t dt ) p (t ) dS (1 p ) X (t )(1 gdt ) pX (t ) 1 S (A1) Now, cancel X (t ) , place the terms over a common denominator and subtract: dp dS p(1 p) gdt S dS 1 (1 p) gdt p S p(1 p) (A2) The differentials in the denominator are nearly zero, so: dp p (1 p ) dS p (1 p ) gdt S (A3) Equation 3 can be derived in several ways. The simplest is to assume p0 p S S0 S (1 p0 )e p0 S0 (A4) gt and dp p p 1 2 p 2 dt dS dS t S 2 S 2 2 p p 1 2 p 2 2 2 p p 2 2 1 p dt dt dS S dZ S dS 2 2 t S 2 S 2 S S t We find: (A5) p gp(1 p) t (A6) p 1 p (1 p ) S S (A7) and 2 p 2 2 p 2 (1 p) 2 S S (A8) Substitution into Equation A5 yields: dS dp p(1 p) gdt p 2 (1 p ) 2 dt S (A9) Appendix B. Derivation of the equation for the fund value associated with the transfer model. We start from Equation 11 under risk neutral growth assumptions: dF rFdt pFdZ (B1) Ito’s Lemma implies that: 2 p2 dt pdZ d ln F r 2 (B2) Or, integrating, ln F ln F0 rt 2 2 p 2 dt pdZ (B3) The last two terms can be put into a form that can be more easily approximated by showing that: 2 2 p 2 dt pdZ 1 2 (1 q ) t q 2 1 (1 q ) Z 2 d ln ( 1 p ) p e e 0 0 1 q 2 p 2 p dt (B4) To prove Equation B4, we will use Ito’s Lemma on the differential in the first integral on the right hand side, that is: 1 2 (1 q ) t 1 d ln (1 p 0 ) p 0 e 2 e (1 q ) Z 1 q 1 2 (1 q ) t 1 2 (1 q) p0 e 2 e (1 q ) Z 1 2 1 2 (1 q ) t 1 q 2 ( 1 p ) p e e (1 q ) Z 0 0 dt 1 2 (1 q ) t e (1 q ) Z 1 (1 q) p0 e 2 1 2 (1 q ) t 1 q (1 p0 ) p0 e 2 e (1 q ) Z dZ 1 2 (1 q ) t 2 2 e (1 q ) Z 1 1 (1 q) p0 e 2 1 2 (1 q ) t 1 q 2 2 ( 1 p ) p e e (1 q ) Z 0 0 2 12 2 (1 q )t (1 q ) Z (1 q) p e e dt 2 1 2 (1 q ) t 2 e (1 q ) Z (1 p 0 ) p 0 e 2 2 2 0 (B5) Now, since from Equation 7 (again, risk neutral growth assumptions), p S p0 S0 (1 q ) S (1 p0 )e r (1 q )t p0 S0 1 q p0 e 1 2 (1 q ) t (1 q ) Z 2 e (1 p0 ) p0 e (B6) 1 2 (1 q ) t (1 q ) Z 2 e Equation B5 becomes: 1 2 (1 q ) t 1 d ln (1 p 0 ) p 0 e 2 e (1 q ) Z 1 q 2 2 pdt pdZ 2 (1 q) 2 pdt 2 (1 q) 2 p 2 dt (B7) Or, with appropriate cancellations: 1 2 (1 q ) t 1 2 2 q 2 2 d ln (1 p 0 ) p 0 e 2 e (1 q ) Z p dt pdZ p p dt 1 q 2 2 (B8) (B9) This proves Equation B4. Substituting into Equation B3 produces: ln F ln F0 rt 1 2 (1 q ) t q 2 1 (1 q ) Z 2 d ln ( 1 p ) p e e 0 0 1 q 2 p 2 p dt The logarithm in the differential is zero at time zero, so: ln F ln F0 rt 1 2 (1 q ) t q 2 1 ln (1 p 0 ) p 0 e 2 e (1 q ) Z 1 q 2 p 2 p dt (B10) or 1 1 2 (1 q ) t 1 q q p 2 p dt F (t ) F0 e rt (1 p0 ) p0 e 2 e (1 q ) Z e 2 2 (B11) Moving e rt inside the square brackets yields Equation 20: S F (t ) F0 (1 p0 )e r (1 q )t p0 S0 1 q 1 1 q q2 2 p 2 p dt e 0 t (B12) Table 1. Percentage of Variable Annuity Funds held in Variable Accounts Quarter 6/30/1998 9/30/1998 12/31/1998 3/31/1999 6/30/1999 9/30/1999 12/31/1999 3/31/2000 6/30/2000 9/30/2000 12/31/2000 3/31/2001 6/30/2001 9/30/2001 12/31/2001 3/31/2002 6/30/2002 9/30/2002 12/31/2002 3/31/2003 6/30/2003 9/30/2003 12/31/2003 3/31/2004 6/30/2004 9/30/2004 12/31/2004 3/31/2005 6/30/2005 9/30/2005 12/31/2005 3/31/2006 6/30/2006 9/30/2006 12/31/2006 Var Pct 76.63% 73.97% 78.32% 76.63% 77.68% 76.92% 80.35% 81.20% 80.49% 80.32% 79.94% 76.67% 77.62% 72.88% 75.32% 75.40% 71.43% 66.27% 64.56% 63.20% 68.38% 66.92% 70.06% 72.22% 71.96% 71.44% 74.16% 73.12% 73.78% 74.75% 74.94% 76.71% 76.03% 77.01% 78.93% q=0.39 Buy and Hold CPR Prediction Prediction Prediction 75.95% 72.95% 77.59% 78.49% 78.21% 76.43% 80.60% 81.18% 80.16% 80.32% 78.37% 76.78% 77.73% 73.16% 75.55% 75.10% 72.34% 66.66% 67.59% 63.33% 67.09% 69.19% 69.61% 70.59% 71.87% 71.30% 73.69% 73.24% 73.40% 74.75% 75.07% 76.02% 75.78% 76.46% 78.28% 75.95% 73.95% 76.54% 78.38% 77.71% 76.73% 79.55% 80.89% 80.40% 80.31% 78.87% 77.64% 77.37% 74.41% 74.76% 75.11% 73.16% 67.97% 67.15% 63.61% 65.95% 68.90% 68.80% 70.39% 71.91% 71.43% 73.01% 73.45% 73.26% 74.43% 74.93% 75.67% 75.99% 76.29% 77.88% 76.17% 76.63% 73.97% 78.32% 76.63% 77.68% 76.92% 80.35% 81.20% 80.49% 80.32% 79.94% 76.67% 77.62% 72.88% 75.32% 75.40% 71.43% 66.27% 64.56% 63.20% 68.38% 66.92% 70.06% 72.22% 71.96% 71.44% 74.16% 73.12% 73.78% 74.75% 74.94% 76.71% 76.03% 77.01% Table 2. Variable Percentages and Variable Returns from Data Supplied by Morningstar Inc. Quarter 3/31/1998 6/30/1998 9/30/1998 12/31/1998 3/31/1999 6/30/1999 9/30/1999 12/31/1999 3/31/2000 6/30/2000 9/30/2000 12/31/2000 3/31/2001 6/30/2001 9/30/2001 12/31/2001 3/31/2002 6/30/2002 9/30/2002 12/31/2002 3/31/2003 6/30/2003 9/30/2003 12/31/2003 3/31/2004 6/30/2004 9/30/2004 12/31/2004 3/31/2005 6/30/2005 9/30/2005 12/31/2005 3/31/2006 6/30/2006 9/30/2006 12/31/2006 Variable Variable Percentage Return 76.17% 76.63% 73.97% 78.32% 76.63% 77.68% 76.92% 80.35% 81.20% 80.49% 80.32% 79.94% 76.67% 77.62% 72.88% 75.32% 75.40% 71.43% 66.27% 64.56% 63.20% 68.38% 66.92% 70.06% 72.22% 71.96% 71.44% 74.16% 73.12% 73.78% 74.75% 74.94% 76.71% 76.03% 77.01% 78.93% 0.37% -12.02% 16.58% 1.93% 7.98% -3.80% 18.54% 5.12% -3.53% 0.41% -7.05% -11.50% 5.61% -14.92% 11.72% 0.24% -9.80% -13.89% 5.53% -2.75% 14.24% 3.82% 10.49% 2.86% -0.23% -1.32% 9.58% -2.35% 2.05% 4.74% 2.26% 5.35% -2.62% 2.78% 6.44% Figure 1. Percentage of variable annuity funds held in equity accounts 85% 80% 75% Var Pct 70% Buy and Hold Prediction CPR Prediction 65% 60% 12/31/1997 12/31/1998 12/31/1999 12/30/2000 12/30/2001 12/30/2002 12/30/2003 12/29/2004 12/29/2005 S Figure 2. Best fit line to c q ln S0 p (1 p 0 )e gt S 0 gt ln (1 p ) p 0 S . Dependent Variable 0.1 0.05 0 -0.2 -0.1 0 0.1 -0.05 -0.1 -0.15 Variable Rate minus Fixed Rate 0.2 Empirical Values Regression Figure 3. Percentage of variable annuity funds held in equity accounts. Comparison of predictions for buy-and-hold and q=0.39. 85% 80% 75% Var Pct 70% Buy and Hold Prediction q=0.39 Prediction 65% 60% 12/31/1997 12/31/1998 12/31/1999 12/30/2000 12/30/2001 12/30/2002 12/30/2003 12/29/2004 12/29/2005 Figure 4. Comparison of GMDB Values for a strike price of 1 with parameters r 5% , 20% , p0 0.70 , constant force of mortality 2% and constant force of lapse 10% . 0.025 GMDB Value 0.02 0.015 CPR, q=-1 0.01 Buy And Hold, q=0 q=0.39 0.005 0 0.7 0.8 0.9 1 Fund Value 1.1 1.2 1.3 Figure 5. Comparison of GMDB deltas for a strike price of 1 with parameters r 5% , 20% , p0 0.70 , constant force of mortality 2% and constant force of lapse 10% . 0 -0.01 0 0.5 1 1.5 2 -0.02 Delta -0.03 -0.04 CPR, q=-1 -0.05 -0.06 Buy And Hold, q=0 q=0.39 -0.07 -0.08 -0.09 -0.1 Fund Value Figure 6. Comparison of GMDB deltas per fund for a strike price of 1 with parameters r 5% , 20% , p0 0.50 , constant force of mortality 2% and constant force of lapse 10% . 0 0 0.5 1 1.5 2 Delta per Fund -0.05 -0.1 CPR, q=-1 -0.15 Buy And Hold, q=0 q=0.39 -0.2 -0.25 Fund Value Figure 7. Comparison of GMDB Values obtained from simulation and integration for a strike price of 1 with parameters r 5% , 20% , p0 0.70 , constant force of mortality 2% and constant force of lapse 10% . 0.05 GMDB 0.04 0.03 Integral, q=0 0.02 Simulation q=0 0.01 0 0.5 1 Fund Value 1.5 Figure 8. Comparison of GMDB Values obtained from simulation and integration for a strike price of 1 with parameters r 5% , 20% , p0 0.70 , constant force of mortality 2% and constant force of lapse 10% . 0.05 GMDB 0.04 0.03 Integral, q=0.39 0.02 Simulation q=0.39 0.01 0 0.5 1 Fund Value 1.5 Figure 9. Comparison of GMDB Values obtained from simulation and integration for an initial fund of 1 with parameters r 5% , 20% , p0 0.70 after 20 years. Cumulative Probability 1.2 1 0.8 Simulated 0.6 Approximated 0.4 0.2 0 0 2 4 6 Fund Value 8 10 Figure 10. Comparison of GMDB Values obtained from simulation and integration for an initial fund of 1 with parameters r 5% , 20% , p0 0.70 after 20 years at small fund values. Cumulative Probability 0.3 0.2 Simulated Approximated 0.1 0 1.1 1.2 1.3 Fund Value 1.4 1.5