EQUILIBRIUM CONDITIONS IN THE OPEN ECONOMY AND THE

advertisement

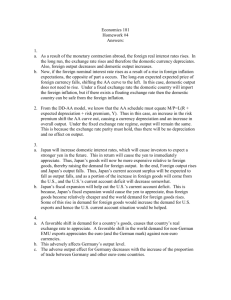

EQUILIBRIUM CONDITIONS IN THE OPEN ECONOMY AND THE MONETARY MODEL OF EXCHANGE RATE DETERMINATION Sarantis Kalyvitis The Nominal Exchange Rate Definition: The exchange rate is the relative price of different currencies An increase in S means that it takes more units of domestic currency to purchase a unit of foreign currency. This is called depreciation (devaluation). A fall in S is called an appreciation (revaluation). The Real Exchange Rate Definition: The relative price of goods in different countries is the Real Exchange Rate (and is an index of competitiveness!). S t Pt ∗ Qt = Pt A real depreciation (improvement in competitiveness) can occur if: The domestic price level falls The foreign price level rises The nominal exchange rate depreciates 1 Equilibrium in International Goods Markets: Arbitrage and Purchasing Power Parity S t Pt ∗ Qt = =1 Pt In equilibrium, Taking logs we get: ⇒ q = st + pt∗ − pt = ln(1) = 0 st + pt∗ = pt Purchasing Power Parity (PPP or Law of One Price) PPP is an equilibrium condition that applies to the goods market. Very important note: PPP does depend on the rapid adjustment of prices in response to arbitrage opportunities! If PPP would apply in the very short run then given a constant foreign price level fluctuations in the nominal exchange rate lead to equivalent variations in the price level. ⇒ The real exchange rate is constant and the nominal side of the economy does not affect the real side (under continuous PPP, money does not affect output). This short-run adjustment is not supported by the evidence though! BP/US relative prices 0,4 2 1,5 0,35 0,3 0,25 1 1975 1980 1985 1990 1995 0,2 1,40 1,20 1,00 0,80 0,60 0,40 0,20 0,00 BP/USD relative prices BP/USD exchange rate 12 10 8 6 4 2 0 18 20 18 40 18 60 18 80 19 00 19 20 19 40 19 60 19 80 2,5 BP/USD exchange rate 0,45 2 A simple application in PPP Suppose we differentiate PPP with respect to time, ds dp dp ∗ = − dt dt dt Since PPP is a log equation the coefficients (they are all 1) are elasticities (written as): ε t = π t − π t∗ Relative Purchasing Power Parity (PPP) ε where t = rate of currency depreciation and domestic inflation πt = rate of To maintain competitiveness the exchange rate must depreciate at a rate equal to the inflation differential between the two countries (by the way, what are the implications for monetary union?) 3 Equilibrium in International Financial Market: Uncovered Interest Parity Question: How do private investors decide how much to invest in each currency assuming domestic and foreign assets are perfect substitutes? Answer: Choose the asset with the highest expected rate of return. The return on domestic assets equals the (nominal) domestic interest rate i on those assets The expected return on foreign assets in domestic currency ∗ equals the i t = foreign interest rate plus the expected capital gain caused by expected exchange rate depreciation. For example at its low the Euro traded at: 1 Euro = 0.9 USDollars It is currently worth: 1 Euro = 0.95 USDollars ⇒ Had an investor used USDs to buy Euros at the lower rate and sold at the higher rate, he would have gained 5 cents (capital gain). In .95 − .90 × 100 ≈ 5.6% percentage terms: .90 Total return it∗ + from foreign Et (S t +1 ) − S t St assets equals in discrete time: If the assets are perfect substitutes then if: it > it∗ + E (S t +1 ) − S t St ⇒ Investors can make expected profits by borrowing abroad and then investing in domestic assets. (Note: since the investor makes a profit for each unit of investment the capital flow toward domestic assets is potentially infinite). 4 Similarly if: i t < it∗ + Et (St +1 ) − St St ⇒ Only foreign currency assets will be held in international portfolios and the capital flow towards foreign assets is infinite. Equilibrium requires the expected return on foreign and domestic assets is equal. Uncovered Interest Parity it = it∗ + Et (S t +1 ) − S t St UIP is a fundamental parity condition that applies to financial markets in an open economy when domestic and foreign assets are perfect substitutes. UIP is an equilibrium condition that applies to financial markets. Very important notes: UIP depends on the expected exchange rate which is unobservable! If foreign assets carry some extra risk then UIP needs to be modified to include a risk premium. Any test on the UIP is a joint test on the UIP and the hypothesis on the formation of expectations. ∆se = (i - i* ) ⇒ Uncovered Interest Parity: Expected Depreciation = Interest Differential The domestic interest rate must be higher (lower) than the foreign interest rate by an amount equal to the expected depreciation (appreciation) of the domestic currency. 5 Foreign Exchange Market Equilibrium The exchange rate is determined in the foreign exchange market. Demand for foreign currency: Domestic and Foreign Public agents require foreign currency for: imports and exports portfolio investment foreign direct investment (for instance, domestic importers require foreign currency to buy foreign goods) These agents can be treated as price takers. Supply for foreign currency: The central bank is a monopoly supplier of domestic currency. The Balance Sheet of the Central Bank ASSETS (claims held by the CB on foreign or domestic entities) Domestic government bonds (Domestic Credit) Foreign Currency (Reserves) Also: Foreign currency denominated bonds, Gold LIABILITIES Monetary base (amount of currency it has issued and is held by the public) MB =D+R MB = Monetary Base D = Domestic Credit R = Reserves 6 Monetary Policy Suppose that the central bank sells one of its assets for domestic money. If it sells a foreign (domestic) asset reserves (domestic credit) falls. On the other hand, MB also falls. ⇒ The money supply falls via the appropriate multiplier. (If it buys an asset from the public or the government the money supply expands.) Note: The Central Bank raises the money supply by: Step 1: buying government bonds from the public and thus increasing the monetary base Step 2: the money supply increases through the money multiplier Step 3: the demand for government bond has risen, which drives their price up and the interest rate down. Exchange Rate Regimes If the central bank does not intervene in the foreign exchange market (i.e. it does not use the amount of foreign reserves to influence the price of the foreign currency) the exchange rate is said to be in a floating rate regime. If the central bank intervenes via its reserves to keep the exchange rate constant, there is a fixed exchange rate regime. Intermediate cases: managed floating, target zones Fixed vs. Floating Exchange Rate Regimes: A Comparison Floating systems Fixed systems - stability in trade (growth) - flexibility for national policies - absence of speculation - no need for reserves - absence of ‘bubbles’ - immediate adjustment - no imported inflation - no excess volatility ⇒ STABILITY ⇒ INDEPENDENCE 7 Monetary approach to exchange rate determination 95% of daily transactions in the foreign exchange market are caused by financial flows resulting from portfolio diversification. The exchange rate is the relative price of different currencies. Therefore the demand and supply for currencies will determine the exchange rate. ⇒ To build a model of a small open economy we need to consider the goods market, the financial market and the money market, as well as the relationship between them. Assumptions Goods Market Equilibrium PPP condition is the equilibrium condition that applies to the goods market and holds continuously (very strong assumption!) – this can be modified later on by assuming sticky prices, i.e. short-run rigidity in the goods market. Financial Market Equilibrium UIP condition is the equilibrium condition that applies to the financial market and holds continuously– this is easier to believe as it deals with nominal variables that can be adjusted instantaneously. The Money Market The exchange rate is the price of domestic money relative to foreign money: the money market is central to the determination of the exchange rate. Ms =Md The money supply is determined by the central bank and is exogenous to the model. Money demand depends upon (standard assumptions): Real Money Demand: As the price level increases, aggregate money demand increases roughly by the same amount. Opportunity Cost of Money: The economy has three financial assets: domestic and foreign bonds, and domestic money. By assumption the bonds are perfect substitutes. Bonds represent interest bearing illiquid assets whilst money is a liquid asset bearing no interest. As the interest rate rises a greater fraction of aggregate wealth is held in the form of bonds and less in the form of money. Transactions: As individuals become wealthier in real terms they purchase more goods. Thus, as real GDP rises the demand for money increases. 1 Money demand equation mt − pt = φyt − λit (all variables in logs except of the interest rate) φ = elasticity of real money demand with respect to output. λ = semi-elasticity of real money demand with respect to the interest rate. Typical values are φ = 1 and λ = .2 , which imply that persistent inflation is always caused by expansion of the money supply. The four fundamental equilibrium (PPP, UIP, Money demand equation, Money market equilibrium) equations can be combined to form a –monetary- model of the open economy. Additional assumptions: The foreign money market matters too, because the exchange rate between any two currencies depends on the demand and supply for both currencies. The domestic economy is small, so it cannot affect foreign variables, which are exogenous. There is perfect foresight, i.e. the future behaviour of all the variables in the above system of equations is known with certainty (obviously not very realistic!). 2 Flexible Price Monetary Model Financial Markets (Perfect Substitutes) it = it∗ • + Et ( s t ) (1) Goods Markets (One good world, flexible prices) st = pt − pt∗ (2) Domestic Money Market mt − pt = φyt − λit (3) Foreign Money Market mt∗ − pt∗ = φyt∗ − λit∗ (4) 3 What are we interested in? Question 1: What are the determinants of the exchange rate? Question 2: What is the relationship between real GDP and the nominal variables such as the money supply and output? The answer to question (2) is that there is no relationship at all, because the PPP condition is assumed to hold at all times and the real exchange rate is constant. ⇒ The real exchange rate is the relative price of identical products expressed in a single currency. If this is not affected by variations in the domestic money supply then money cannot affect output. Notice that the assumption of PPP is contradicted by the data. It is even difficult to show that PPP holds in the long run. (Reasons: differentiated products and/or sticky prices). ⇒ Relaxing PPP is therefore likely to give effects of nominal on real variables. Still, although we know the model is hard to believe it still provides a useful vehicle for analysing many issues. 4 Solving the model ∗ Solve for pt and pt from (3) and (4) and then substitute into (2). Then use (1) to replace the interest differential to obtain: ds st = mt − mt∗ − φ ( yt − yt∗ ) + λEt t dt (4) An alternative is to simply ignore the foreign money market and write (4) as, dst st = mt − φyt − p + λi + λEt dt ∗ t ∗ t (5) The exchange rate depends upon four variables plus the expected rate of depreciation. Question: What causes the exchange rate to depreciate? The exchange rate will depreciate if the money supply rises, real GDP falls, the foreign price level falls or the foreign interest rate rises. It is reasonable to suppose that the expected rate of depreciation depends upon the four variables that precede it in equation (5). These are called "fundamentals" (fundt). 5 Method of Solution Step 1. Write the exchange rate as, ds st = fundt + λEt dt ∗ ∗ where the "fundamentals" are fundt = mt − φyt − pt + λit (1) (2) Step 2. Specify the behaviour of fundamentals appropriately in (2). For example, if a variable such as the money supply is growing over time this must be explicitly recognised. Step 3. Postulate that: d ( fund ) ds Et = Et =? dt dt Substitute the results from steps 2 and 3 back into 1. 6 Example 1: constant fundamentals dst st = mt − φyt − p + λi + λEt dt ∗ t ∗ t Denote the fact that the fundamentals are constant by: f t = f = m − φy − p ∗ + λ i ∗ Given that none of the fundamental determinants of the exchange rate are changing or indeed expected then it is reasonable to suppose that: ds Et t = 0 dt So that the solution for the exchange rate is: s = m − φy − p ∗ + λ i ∗ 7 Example 2: A constant rise in the money supply Now suppose that the money supply grows at the rate be constant. µ. All other fundamentals are assumed to If a variable X(t) grows at a constant rate µ then the log of X(t) will equal after time t: x(t ) = x(0) + µt where X(0) is the value at time 0 and µt the growth that has since occurred. The money supply at time t is equal to, mt = m0 + µt (8) All other fundamentals are constant. Because the money supply is growing over time it is easy to infer that the exchange rate should depreciate. But by how much? 8 Money Market Equilibrium The depreciation reflects the excess money supply but if there is an excess money supply the money market cannot be in equilibrium. The depreciation of the exchange rate cures this. Since PPP holds prices rise at the same rate as the currency. ds dp dp∗ = − dt dt dt Foreign inflation is constant by assumption ⇒ ds = dp dt dt As the exchange rate depreciates aggregate demand rises. However because prices are perfectly flexible prices instantly rise at the same rate µ . ⇒ money demand increases at the same rate the money supply rises ⇒ • • • mt = p t = s t If the domestic money supply is expanded by 10% the nominal exchange rate depreciates by 10% and the rate of inflation is 10%. The real exchange rate is constant. 9 The rate of currency depreciation ∗ ∗ Step 2 implies that: f t = m0 + µt − φy − p + λi The long-run solution implies that: ds • = st = µ dt Given pt , yt , it money demand is constant so rate of money growth of µ creates an excess supply of domestic currency and an expected exchange rate depreciation of rate µ. st = m0 + µt − φy − p ∗ + λi ∗ + λµ 10 Why is there a jump depreciation of λµ ? Consider the last example in terms of our original equations: it = it∗ • + Et ( s t ) st = pt − pt∗ mt − pt = φyt − λit With perfect foresight the exchange rate depreciation is common knowledge. ⇒ A rise in the rate of expected depreciation raises the return on foreign assets. ⇒ To maintain UIP the domestic interest rate must rise by the same amount. A once-off increase in the domestic interest rate creates a downward jump in money demand and a discrete depreciation of the nominal exchange rate: ds Et = µ ⇒ ∆i = µ ⇒ ∆md = − λµ ⇒ ∆s = λµ dt 11 Summary of Results The real and nominal sectors are by assumption independent (classical ‘dichotomy’). This is a consequence of price flexibility through PPP. Changes in the variables comprising the fundamentals affect the current exchange rate. The monetary model may be a good theory of long-run exchange rate determination (depending on the validity of PPP), but is very unlikely to be confirmed in the short run. The expected exchange rate matters for the determination of the current exchange rate (‘forward-looking’ variable). 12