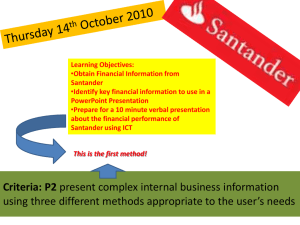

General Terms & Conditions

advertisement