Combining Prices and Quantities Pollution Controls Under

advertisement

June 8, 2015

Combining Prices and Quantities Pollution Controls Under

Partitioned Environmental Regulation

Jan Abrella , Sebastian Rauscha,b

a

Center for Economic Research at ETH (CER-ETH), Department of Management, Technology and Economics, ETH

Zurich, Zurich, Switzerland.

b

Joint Program of the Science and Policy of Global Change, Massachusetts Institute of Technology, Cambridge, USA.

Abstract

We argue that bounds on permit prices can improve the cost effectiveness of partitioned emissions

regulation under uncertainty if the price constraints are used to reallocate the abatement burden

across sectors. In posing the problem, we have in mind a situation where the regulatory authority

is uncertain about the abatement costs of polluting firms and cannot impose a uniform regulation

scheme. Therefore, one part of the economy is directly subjected to quantity regulation and complementary control measures are taken in the other to meet the overall environmental target. In

such a setting the introduction of a price floor and ceiling below and above the optimal price decreases the cost of regulation. We illustrate the cost savings in a quantitative model of European

carbon abatement in which some sectors are part of the European emission trading schemes and

the remaining are regulated by and additional cost-effective measure. We find that price bounds

have the potential to decrease the excess cost of regulation under uncertainty by around one half.

Keywords: Emissions Trading, Price Floors, EU ETS, Computable General Equilibrium

Modeling

JEL: Q48, Q54, C68

1. Introduction

It is well known that an ex-ante optimal permit (or tax) policy will in general yield ex-post inefficiency when the regulatory authority is uncertain what the actual costs of pollution control will

be (Weitzman, 1974). Several hybrid regulation strategies which combine elements of permit markets and price control and lead to ex-post efficiency have been proposed in the literature (Roberts

& Spence, 1976; Collinge & Oates, 1982; Unold & Requate, 2001; Pizer, 2002). In one way or

another, these hybrid strategies propose to implement a price-quantity relation for emissions that

∗

Corresponding author: Jan Abrell, Department of Management, Technology, and Economics, ETH Zurich,

Zürichbergstrasse 18, ZUE E, 8032 Zurich, Switzerland, Phone: +41 44 632-06-52. Email: jabrell@ethz.ch.

equals the marginal damage function. The welfare gains of ex-post efficient hybrid regulation

relative to using either pure price or quantity controls have shown to be substantial (Pizer, 2002).

Two critical features of real-world examples of quantity controls (or permit markets) seem,

however, to be at odds with the predominant view underlying the literature on ex-post efficient

permit markets. First, it is assumed that policymakers are confronted with the dual task of choosing the overall environmental target and selecting the policy instruments to achieve this target.

While this view unarguably describes the regulatory problem in more general terms, the problems

of target setting and instrument choice (or design) are often viewed separately in real-world policymaking. In particular, the question of how to choose policy instruments is typically investigated

under the assumption of a fixed environmental target. Second, none of the previous analyses have

considered the fact that many real-world examples of environmental regulation are characterized

by incomplete coverage of pollution sources. For example, most of todays carbon dioxide (CO2 )

emissions trading schemes (ETS) implemented in numerous countries around the world to combat

climate change cover only a relatively small fraction of total emissions; at the same time, complementary policy measures to control non-covered emissions are employed to meet a given overall

national environmental target.1

This paper examines the following question: how can hybrid (price and quantity) environmental regulation be designed in order to minimize aggregate compliance costs if the overall environmental goal is fixed and if there exists incomplete regulatory coverage? In posing the problem,

we have in mind a situation where the regulatory authority is uncertain about the (marginal) abatement costs of polluting firms in both parts of the economy, i.e. the one that is directly subjected

to quantity regulation and the one where complementary control measures are taken to meet the

overall environmental target. In particular, we are interested in the question how elements of price

control regulation can be introduced into an otherwise standard permit market system to enhance

ex-post welfare under for a given environmental target.2

As a motivating example for our analysis we take the European Unions 2020 Climate and

Energy Package (Commission, 2008). The central pillar is the EU ETS which represents today

the largest international trading system for greenhouse gases and is often conceived as a prototype

for other cap-and-trade systems now emerging all over the world (Convery, 2009). The EU ETS

covers only about 45% of emissions, mainly from electricity and energy-intensive installations.

The remainder of emissions to achieve overall EU reductions goals of 20% by 2020 (relative

to 1990 levels) has to be achieved outside of the EU ETS through complementary measures by

Member States.3

Permits markets, such as the EU ETS, have shown to suffer from two major structural problems

1

In fact, this situation is reflective of the current energy and climate policy context in many countries. Regulatory

approaches often comprise permit trading instruments and use additional, distinct instruments to regulate energy use

and emissions in non-covered sectors.

2

Given that we assume the overall environmental target to be fixed, we analyze ex-post “better” but not “efficient”

hybrid permit markets.

3

Under the so-called “Effort Sharing Decision”, Member States have taken on binding annual targets for reducing

their greenhouse gas emissions from the sectors not covered by the EU ETS. See Decision No 406/2009/EC of the

European Parliament and of the Council of 23 April 2009 on the effort of Member States to reduce their greenhouse

gas emissions to meet the Communitys greenhouse gas emission reduction commitments up to 2020.

2

that are directly related to incomplete regulatory coverage. First, the limited sectoral coverage can

severely undermine cost-effectiveness due to the failure to equalized marginal abatement costs

across all emissions sources (Böhringer et al., 2006, 2014).4 . Second, complementary climate and

energy policy measures in sectors not regulated under emissions trading have created substantial

downward pressure on the permit price. Too low carbon prices are often viewed as increasing

investment uncertainty, which is likely to have a negative impact on further investments in lowcarbon technologies. In fact, the Commission (2014) has proposed to introduce in phase 4 a

“Market Stability Reserve which aims at rectifying the structural problem of allowances surplus

by creating a mechanism that adjusts the supply of permits based on the demand for permits. This

feature can be interpreted as effectively introducing price control elements (i.e., a price bound and

ceiling) in the permit market.5

We argue in this paper that bounds on permit prices can improve the cost-effectiveness of hybrid emissions regulation if the price constraint is used to reallocate the abatement burden across

sectors. We find, that permit price floors below the theoretically optimal price decrease the cost of

regulation. Likewise, permit price ceilings are beneficial as long as the ceiling is above the optimal

price. Our results are consequential for the practical implementation of hybrid emission trading

system, particularly for the current discussion about the implementation of a market stability reserve for the EU ETS.

The paper is organized as follows. Section 2 presents theoretical background of price floors

or more general permit price bounds in regulation systems with partitioned environmental targets.

In section 4 analyzes the empirical implications of a price floor for EU-ETS allowances on the

welfare cost of reaching European carbon abatement targets. Section 5 summaries our findings

and draws conclusions for the future design of the EU-ETS.

2. Model

2.1. Setup

We consider an economy with two polluting sectors i ∈ {T, NT} and partitioned environmental regulation. Emissions in sector T are initially regulated by a pure quantity instrument, i.e. an

emissions trading scheme. Emissions in sector NT are not covered under the emissions trading

scheme but are assumed to be regulated by a separate instrument which is assumed to achieve costeffective abatement in sector NT (for example, through a carbon tax or sectoral permit market).

The regulator is uncertain about the(marginal) abatement cost curves in each sector. Before the

revelation of uncertainty the regulator has to decide about regulatory measures. I.e., the regulator

decides about the partition of the emission budget and (possibly) some a price floor and ceiling in

the permit market of the trading sector. In the case of price bounds, it is assumed that the regulator

can ex-post, i.e., after the revelation of marginal abatement cost curves (MAC),6 adjust the abate4

Cost-effectiveness may also be hampered by strategic partitioning (Böhringer & Rosendahl, 2009; Dijkstra et al.,

2011) While this was more likely to be an issue in first and second phases of the EU ETS, the current phase

5

Other cap-and-trade systems in the world, such as in California, RGGI, and Australia already have a minimum

price in place.

6

Throughout the remainder of the is article we refer to situation before (after) the revelation of uncertainty as

ex-ante (ex-post).

3

ment allocation according to an ex-ante specified reallocation rule such that overall abatement

remains constant.

Actual sectoral emissions are denoted by ei , and emissions before the introduction of regulation

are given by e0i . The overall environmental target in the economy is fixed throughout and given by

P

e, and assumed to be binding, i.e. e < i e0i . Sectoral abatement is defined by ai = e0i − ei , and

P

the total abatement requirement is a := i e0i − e > 0. The regulator decides how total abatement

is allocated across sectors by choosing sectoral abatement requirements ai . The fulfillment factor

is defined as the share of total abatement allocated to the sector T subject to emission trading:

λ := aaT .

The costs of abatement in sector i are denoted as Ci (ai , ηi ) and assumed to be strictly convex

in the abatement (∂Ci /∂ai > 0 and ∂2Ci /∂a2i > 0). ηi is a sector specific disturbance term which is

distributed over the compact support [−bi , bi ] with the distribution function fi (ηi ). Abatement cost

are assumed to be increasing in the disturbance term (∂Ci /∂ηi > 0). At the time when the regulator

decides over regulatory instruments the abatement cost functions and the disturbance distributions

are common knowledge. However, neither the regulator nor the firms knows the realization of the

random variables. After the realization of the disturbance terms, they are known by the firms as

well as by the regulator.

The regulatory authority’s decision problem is to choose a set of pollution control measures to

minimize expected total abatement cost:

(1)

Ψ = E CT (λa, ηT ) + CNT ({1 − λ}a, ηNT ) .

In posing this problem, we have in mind a world of partitioned environmental regulation where the

partition of the system is exogenously given in the sense that the assignment of firms to the trading

and non-trading sector is exogenous.7 The regulator seeks to optimize the regulatory scheme by

imposing additional price bounds in the sector that is subject to an ETS for a given instrument

choice in the other sector and given a fixed economy-wide environmental target for the entire

economy.

2.2. First-best

Before characterizing the optimal solutions in the presence of uncertainty, it is useful to define

the first-best situation as a reference point. In such a first best situation the regulator is able to

choose a state-dependent abatement allocation. I.e., for each state of the world (likewise possible

combination of ex-post abatement functions) the regulator can assign the abatement allocation

separately. Minimizing (1) by choosing a state-dependent fulfillment factor, yields the well known

condition that MAC are equalized across sectors in every state of the world:8

∂C NT (aNT , ηNT ) ∂CT (aT , ηT ) =

∀ηT , ηNT .

(2)

∂aT

∂aNT

aT =λa

aNT =(1−λ)a

Condition (2) implicitly defines the ex-post optimal fulfillment factor as a function of the state

variables: λ∗ex-post (ηT , ηNT )

7

Caillaud & Demange (2005) analyze the optimal assignment of activities to trading and tax systems under uncertainty.

8

An interior solution, i.e., λ ∈ (0, 1) is assumed.

4

2.3. Pure quantity control

In general, the regulators has to choose the regulatory measure ex-ante, i.e., before the realization of the marginal abatement cost curves. In this section it is assumed that the regulator can only

choose the abatement burden for the different sectors, likewise, the fulfillment factor λ. Note, that

as the fulfillment factor is chosen ex-ante, i.e., is independent from the state of the world. Minimizing total abatement cost (1) leads to the optimality condition that the expected MAC equalize

across the sectors:

#

"

#

"

∂C NT (aNT , ηNT ) ∂CT (aT , ηT ) =E

.

(3)

E

∂aT

∂aNT

aT =λa

aNT =(1−λ)a

Condition (3) implicitly defines the ex-ante optimal fulfillment factor under pure quantity control

λ∗ex-ante which is independent of the realization of the disturbance terms.

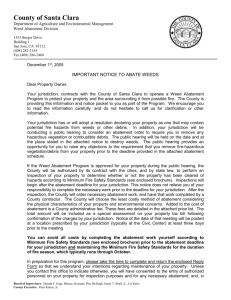

Figure 1: Emissions trading and price controls under partitioned environmental regulation

Given incomplete information about firms’ abatement costs, it is, however, unlikely that the

ex-ante optimal fulfillment factor will equate ex-post marginal abatement costs, i.e. after the realization of the random variable. Thus, in general λ∗ex-ante , λ∗ex-post (ηT , ηNT ). Figure 1 depicts

the ex-post sectoral marginal abatement cost functions and the ex-ante and ex-post optimal fulfillment factors for a given environmental target. Total abatement costs are minimized if abatement

burden is partitioned according to λ∗ex-post which leads to the optimal uniform carbon price P∗ . If

λ∗ex-ante , λ∗ex-post (ηT , ηNT ), the carbon prices in the T and NT sectors, PT and PNT differ and excess

abatement costs are given by the sum of the two gray shaded areas. Given partitioned environmental regulation and uncertainty about firms’ abatement costs, the deviation between ex-ante and

ex-post optimal fulfillment factors causes excess cost of second-best regulation which motivates

the introduction of price bounds in order to hedge against high differences in MAC.

5

2.4. Quantity control with permit price bounds

We now extend the regulators set of instruments by a price floor and ceiling. I.e., the regulator

chooses the fulfillment factor as well as the bounds on the permit price in the T sector before the

realization of the disturbance terms. As the environmental target is constant, a binding price floor

implies rationing of the emission budget in the T sector and shifting this amount to the remaining

sector. In contrast, a binding price ceiling will decrease (increase) the abatement requirement in the

T (NT ) sector. Thus, the ex-post fulfillment factor, i.e., after realization of abatement cost, will be

a function of the state variables. However, in contrast to the first-best case the ex-post fulfillment

factor is not a choice of the regulatory authority but indirectly influenced by the price collar chosen

before the revelation of uncertainty. We proceed by first analyzing the ex-post situation after the

realization of a specific state followed by a characterization the optimal choice of the fulfillment

factor and price collar.

2.4.1. Ex-post effects of price bounds

Consider again the situation after the realization of specific state as shown in Figure 1. Exante, the regulator has chosen the fulfillment factor λ∗ex-ante as well as a the price floor Pmin . Without

price bounds, i.e., under pure quantity control, this would lead to emission prices PT and PNT in the

respective sectors. If the price in trading sector is above the price floor (PT > Pmin ), the price bound

has no impact. If, in contrast, the price in the T sector realizes below the price floor (PT < Pmin ),

the price bound becomes binding and abatement in the T sector needs to be increased in order to

increase the price. As the environmental target, i.e., total abatement, is constant, abatement in the

NT sector has to decline. Consequently, the allocation factor is adjusted to λmin . As abatement

in the non-trading sector decreases, the carbon price in this sector declines from PNT to Pmin

NT .

Therefore, the introduction of the price floor moves sectoral carbon prices, and, thus, marginal

abatement cost, closer to the uniform first-best carbon price P∗ as compared to a pure quantitybased regulation scheme. As a consequence the excess cost of second-best regulation decrease by

the light gray-shaded area. As a similar argumentation can be applied for a price ceiling above the

optimal first-best price, we obtain the following proposition.

Proposition 1. Given strictly convex sectoral abatement cost functions, a constant economy-wide

environmental target, and partitioned regulation with sectoral targets implied by a pre-determined

fulfillment factor λ

(a) an emission price floor in one partition (weakly) decreases total abatement costs if the price

bound is lower or equal to the optimal permit price P∗ .

(b) an emission price ceiling in one partition (weakly) decreases total abatement costs if the

price bound is greater or equal to the optimal permit price P∗ .

Proof. See Appendix A

Proposition 1 reflects a fundamental economic intuition: Under partitioned environmental regulation and given that the environmental target is assumed to be constant, the regulator cannot

be worse in terms of total abatement costs as long as the price floor is set below or equal to

the (ex-post) optimal environmental tax. If the initially chosen fulfillment factor was too high,

6

i.e. abatement in the trading sector is sub-optimally high, the permit price exceeds the optimal

level anyways but the price floor will not be binding. Thus, total abatement cost are not affected.

In contrast, if the fulfillment factor was set too low, the endogenous adjustment of the fulfillment

factor triggered by introducing a binding price floor will decrease total abatement cost.

Proposition 1 implies that if the regulatory authority faces partitioned environmental targets

and has access to an estimate of the optimal permit price in one of the sectors, imposing a price collar together with a mechanism that adjusts sectoral environmental targets under an overall constant

abatement effort has the potential to decrease total abatement costs. Put differently, introducing the

price collar endogenously reallocates carbon budgets such that abatement costs are reduced. As a

consequence, the optimal carbon price needs not to be known for sure, but estimating an interval

and imposing the respective price collar improves efficiency of environmental regulation.

2.4.2. Ex-ante choice of price bounds

Before the realization of marginal abatement cost curves the regulator decides about the fulfillment factor λ and lower (P) and upper (P) price bounds in the trading sector T . The objective is

to minimize expected total costs, consisting of abatement costs in both sectors. As shown, if one

of the price bounds becomes binding, the fulfillment factor adjusts endogenously such that total

abatement is held constant. Denote

the endogenous fulfillment factor for the case of a binding

floor and ceiling by λ̃ P and λ̃ P , respectively. For given levels of λ, P, and P, there will be two

critical levels of the cost shock ηT for which the price control is binding which are defined and

denoted as:

h

i

∂CT λa, η

∂CT λa, ηT

T

and

− P = 0 ⇒ η λ, P, P

− P = 0 ⇒ η λ, P, P . (4)

∂AT

∂aT

The regulator’s optimizing problem can then be written as:

h

i

min C λ, P, P := E CT (λa, η) + CNT ({1 − λ}a, ηNT ) | η < ηT < η

n

o

+ E CT λ̃ P a, η + CNT 1 − λ̃ P a, ηNT ηT < η

T

n

o

+ E CT λ̃ P a, η + CNT 1 − λ̃ P a, ηNT ηT > ηT

(5)

λ ∈ (0, 1), P, P ≥ 0

The first line part of (5) represents expected total abatement cost in the case when neither

the price floor nor the ceiling is binding. In the second part, the price floor is binding and the

fulfillment factor is endogenously adjusted. The third line expresses the opposite case of binding

price ceiling. If the price floor is equal to zero and the ceiling set a level such that it becomes never

binding, the expected total abatement cost function (5) is equivalent to the expected abatement

csot function under pure quantity control (1). Consequently, the regulator’s problem of choosing

the fulfillment factor and price bounds includes the optimal solution under pure quantity control.

Thus, expected cost under additional price controls are bounded above by the cost of the pure

quantity scheme. Put differently, the introduction of price bounds can never increase expected

7

abatement cost but has the potential of decreasing them. It has to be mentioned, however, that this

does not necessarily holds in all ex-post states of the world, i.e., the there might be states in which

price bounds increase ex-post cost.

The respective first order conditions become (see Appendix B for derivation):9

"

#

∂CT ∂C NT

∂C

=E

−

=0

(6)

∂λ

∂AT ∂ANT

!

∂C

∂C NT 1

ηT ≤ η = 0

= E ∂2C P −

(7)

T

T

a 2

∂P

∂ANT ∂aT

!

∂C

∂C

1

NT = 0 .

η

≥

= E − ∂2C P −

η

(8)

T

T

T

∂A

NT ∂P

a ∂a2

T

By comparing the first order condition for the optimal fulfillment factor (6) with the one under

pure quantity control (3), we observe that they are equivalent. Thus, the choice of the optimal

fulfillment factor is independent of the possible introduction of permit price bounds in the trading

sector. The first order conditions for the optimal price floor (7) (ceiling(8)) requires the equalization of the non-trading sector’s MAC with the price floor (ceiling) in expectations conditional on

the fact the price bound is binding.

Proposition (1) implies a lower and upper bound on the optimal price floor and ceiling. It states

that every price floor (ceiling) below (above) the first-best optimal permit price does not increase

abatement cost. Consequently, a price floor (ceiling) equal to the lowest (highest) first-best permit

price cannot increase abatement cost. The results are summarized in the following proposition:

Proposition 2. Under a hybrid regulation scheme in which the regulator imposes a quantity regulation in one sector and announces price bounds on the corresponding permit price:

(a) The ex-ante optimal fulfillment factor λ∗ex-ante is identical to the one under pure quantity control.The regulator chooses λ∗ex-ante such that the (unconditional) ex-ante expected difference

of marginal abatement costs across partitions is zero.

(b) The optimal ex-ante price floor (ceiling) is bounded below (above) by the lowest (highest)

first best (ex-post) optimal permit price.

(c) The expected cost under quantity regulation with price bounds are lower equal the expected

cost under pure quantity control.

Summarizing, we showed that the regulator can impose a price collar bounded by the lowest

and highest first-best permit price and will weakly decrease expected total abatement cost. However, that does not necessarily imply that ex-post abatement cost are always lower than under pure

quantity regulation. The result is derived under following main assumptions: First, the total abatement requirement is constant. While it is well known that an constant abatement effort is likely to

9

In the current version we assume the disturbance terms to be independently distributed.

8

lead to ex-post inefficiencies in term of deviating marginal abatement cost and marginal damage,

the assumption reflects a likely situation in a real world policy design in which the choice of the

target and the instruments is often separated. Second, the partition of the regulation system is

exogenously given, i.e., the regulator cannot change the assignment of firms to the different partitions. In a realistic policy environment such an partition is often influenced by monitoring cost

and political feasibility. Therefore, policy makers need to determine the partition and afterwards

determine the instruments. Third, the regulator is able to implement a rationing mechanism that

ex-post shifts abatement burden from one sector to the other. In the case of two parallel trading

systems, this is easily be achieved by converting permits of one system into the ones of the other.

In the case of an tax instrument, the resulting tax change has to be calculated. Whether such an

mechanism is political feasible depends on the associated change in expected cost and, moreover,

on the shift of price risks from one sector to the other. Forth, the regulator has access to a distribution of abatement cost. In an ex-ante assessment of political measures, MAC are always subject to

some uncertainty. Therefore, impact assessment usually perform sensitivity analysis of the most

important parameters. Such sensitivity analysis can be easily extended to provide distributions of

marginal abatement cost curves.

3. Numerical Framework

3.1. Marginal Abatement Cost Functions

Our numerical analysis requires a distribution of marginal abatement cost curves. In the case

of carbon abatement, such functions are usually derived in a top-down way using Computable

General Equilibrium (CGE) models. A series of carbon taxes is imposed in the sector of interest.

Given the resulting abatement, a MAC function can be derived by fitting a continuous curve on the

series of tax and abatement pairs (e.g Klepper & Peterson, 2006; Böhringer & Rosendahl, 2009;

Böhringer et al., 2014).

For the derivation of MAC curves, we apply standard static multi-sector, multi-region CGE

model.10 . The model relies on nested Constant Elasticity of Substitution (CES) functions with the

nesting structure shown in Figure 3.1 in which the σ indicate the respective substitution elasticity. For production sectors, we combine materials with an aggregate of value-added, i.e., a capital

labor bundle, and an energy composite which combines electricity with a bundle of fossil fuels.

On the consumption side, non-energy and energy-consumption bundles are combined to the final consumption commodity. Government and investment are included using Leontief functions.

International trade is modeled using the Armington (1969) approach, i.e., domestic and imported

commodities are treated as imperfect substitutes. The model is closed assuming a constant balance

of payment and a fixed investment closure.

The model is parameterized on the GTAP database (Narayanan et al., 2012) database, which

is aggregated to a European and rest of the world region. Energy sectors (electricity, coal, natural gas, refined oil, crude oil) are represented in a detailed manner while the remain sectors are

aggregated to energy intensive production, agriculture, services, transport, and manufacturing. In

10

A full algebraic description of the model is provided in Appendix C

9

Figure 2: Functional Forms

Y

σtop

VAE

vae

...

σ

VA

va

...

...

ENE

ene

σ

K

Materials

C

σ

L

ELE

FOF

COA

PC

σctop

CENE

cene

σfof

CCON

ccon

σ

...

GAS

σ

Energy Commodities

(a) Production

...

...

Non-Energy Commodities

...

(b) Final Consumption

the calibration of the CES function substitution elasticities enter as free parameters. Beside the

elasticities in Figure 3.1, elasticities for the Armington approach are needed. The Central column

in Table 1 lists the substitution elasticities and assumed parameter values in the model which are

in line with the literature (e.g. Paltsev et al., 2005b). Narayanan et al. (2012) provides Armington

elasticities and substitution elasticities for the value-added bundle.

Table 1: Parameter values for substitution elasticities in production and consumption

Parameter

Production

σYTOP

σYMAT

σKLE

σKL

σENE

σFOF

Consumption

σtop

σene

σoth

Description

Materials vs. energy/value-added bundle

Materials

Value-added vs. energy bundle

Capital vs. labor

Primary energy vs. electricity

Fossil fuels

Energy vs. non-energy consumption

Energy commodities

Non-energy commodities

Central

Min

Max

0

0.50

0.8

0.30-1.50

0.30

0.50

0

0

0.4

1

1

1.6

0

0.1

1

0.9

0.5

0.5

0.5

0.9

0.9

0.9

0.1

0.1

0.1

3.2. Quantitative Approach

Given a distribution of MAC curves, we compute the first-best optimum as well as the secondbest optimum of pure quantity control with and without additional price bounds.11 . The computation of the first-best and second-best under pure quantity solution is done using standard techniques

11

The computational approach is described in greater detail in Appendix D

10

of non-linear programming by minimizing expected abatement cost (1) under respective choice

variable. However, the computation of optimal price bounds in (5) is not as straight forward as

the condition in the expectation operator, i.e., the bounds of the integrals, need to be chosen. Our

strategy formulates the problem as Mathematical Program under Equilibrium Constraints (MPEC)

(Luo et al., 1996). As this class of problems is generally difficult to solve, we use Proposition 2

to first compute the optimal fulfillment factor under pure quantity control. Given the fulfillment

factor and an exogenous price floor and ceiling, we reformulate the problem as an Mixed Complementarity Problem (MCP) which can be easily solve. We the used the boundaries on the optimal

price bounds derived in Proposition 2 and perform grid search about the relevant range of price

floor and ceiling to find the cost minimal solution.

Figure 3: Marginal Abatement Cost Curves

Dotted lines and dark shaded areas represent expected value and 25 to 75% interval, respectively.

4. Minimum Prices in the European Emission Trading System

We analyze the introduction of price bounds in the EU ETS under parameter uncertainty in the

used policy assessment tool, i.e., the CGE model. As substitution elasticities are most influential

for the results and difficult to estimate as precise values depend on the model structure, there is a

high degree of parameter uncertainty regarding the choice of these elasticity. We thus, consider

the elasticities as uncertain and uniformly distributed between the minimum and maximum values

provided in Table 1. For value provided by Narayanan et al. (2012), i.e., Armington and value

added elasticities, we assume that they might change from half to 1.5 times the value provided. We

11

create a distribution of marginal abatement cost curves by randomly drawing all elasticities from

the respective distributions and imposing a carbon tax from zero to 150 $/tCO2 in the respective

sectors assuming lumpsum revenue recycling. The resulting tax-abatement pairs are then fitted

using the least square method assuming marginal abatement cost curves to be cubic in abatement.

Using a second draw, we then calculate the marginal abatement cost function for the next sector,

i.e., for each sectors’ function the elasticity are independently sampled. Following the design of

the EU ETS, we consider electricity, refined oils, and energy intensive industries to be part of the

trading system. All remaining sectors including final consumption are then part of the non-trading

sector.

Figure 4: Distribution Ex-post Abatement Cost

(a) Total

(b) Trading

(c) Non-Trading

Figure 3 show the resulting MAC curves using 1000 sample draws considering a policy to

reduce 30% of the benchmark carbon emissions which approximately equals 1000 MtCO2 . The

curve of the trading sector runs from the lower right right to the left. The dotted lines represented

the median value while the dark shaded area indicate the 25 to 75% quantiles, respectively. It

becomes evident that the variation in the estimates increases with the abatement requirement.

Figure 3 suggest that the main abatement burden is imposed on the trading sector. This result is

mainly caused by the inclusion of the transport sector and final consumption into the non-trading

sector. The European transport sector is already subject to high fuel tax causing high tax interaction

costs (Paltsev et al., 2005a; Abrell, 2010). Furthermore, we exclude non-CO2 greenhouse gases in

particular methane emissions of agriculture which have a high abatement potential (Hyman et al.,

2002).

The main results are summarized in Table 2 showing the resulting expected abatement cost,

the fulfillment factor, and carbon prices as well as the standard deviations thereof. In the first-best

optimum the total abatement cost become 25.13 Billion $ which are mainly imposed on the trading

sector (17.5 Billion $). The standard deviation of total cost realizes at 5.35 Billion $ with standard

deviation of 3.21 Billion $ in the trading sector. Figure 4 shows the distribution of abatement

cost. The expected carbon price is 67.44 $/tCO2 with a standard deviation of 12.05 $/tCO2 and the

distribution of carbon prices is shown Figure 5. The minimum and maximum first-best optimal

carbon price are 43.35 and 108.11 $/tCO2 , respectively.

The second-best optimum under pure quantity control increases the expected abatement cost

by 0.42 Billion $. As the 76% of the abatement burden is allocated to the trading sector and as

12

Figure 5: Distribution Ex-post Carbon Prices

(a) Trading

(b) Non-Trading

The y-axis showing the frequency is capped at 100. The frequency of a binding price floor (ceiling) is 270 (170).

Table 2: Expected cost and carbon prices under different regulatory instruments

Expected Cost [Billion $]

First-Best

Pure Quantity

Price Collar

Trading

Non-Trading

Total

17.496 (3.213)

7.630 (2.350)

25.126 (5.355)

Trading

Non-Trading

Trading

Non-Trading

Trading

Non-Trading

67.44 (12.05)

67.44 (12.05)

43.35

43.35

108.11

108.11

17.900 (5.516)

7.650 (1.072)

25.550 (5.560)

75.8%

68.55 (10.19)

68.55 (19.20)

37.22

49.05

151.04

105.88

17.625 (3.273)

7.678 (2.860)

25.303 (5.404)

75.8%

67.86 (12.37)

67.84 (16.25)

54.69

25.52

86.75

147.54

Fulfillment Factor [%]

Expected Price [$/tCO2]

Minimum Price [$/tCO2]

Maximum Price [$/tCO2]

Standard deviation are given in parenthesis. Highlighted cells contain price floor and ceiling.

the uncertainty in the MAC estimated is increasing in the abatement effort, the cost uncertainty

in this sector is increasing as indicated by the increase in the trading sector’s standard deviation

of cost. The effect also becomes evident inspecting the cost distributions in Figure 4: While the

cost distribution is narrowing the in non-trading sector, extreme cost events become more likely in

the trading sector. The expected permit price increases by around 3 $/tCO2 . The minimum (maximum) price in the trading sector lies below (above) the counterpart in the first-best equilibrium

indicating the potential of cost savings by introducing additional price control.

Allowing for the additional introduction of permit price bounds in the trading sector, reduces

the excess cost of second-best regulation to 0.18 Billion$. Put differently, the introduction of a

price floor and ceiling decreases the excess cost of second-best regulation by around 58%. The

optimal price floor an ceiling are set to 54,69 and 86,75 $/tCO2 . As it becomes evident in Figure

13

Figure 6: Cost Difference Pure Quantity Control without and with Price Bounds

The y-axis showing the frequency is capped at 100. The frequency of zero cost savings is 558.

4 the price bounds decrease expected cost in the trading sector. In particular, the cost distribution

in the trading sector narrows, i.e., the uncertainty about future cost is reduced as also shown by an

40% decrease in the standard deviation. As a consequence the cost uncertainty in the non-trading

sector increase and expected non-trading sector cost are also increasing. The imposition of permit

price bounds becomes most evident in distribution of the trading-sector’s carbon price in Figure

5 which shows a high probability mass at the minimum and maximum price. The probability of

binding price floor (ceiling) becomes 27% (17%). In contrast, the price distribution in the nontrading sector is widening. However, the expected price in both sector is increasing.

As noted, the introduction of a permit price collar does not necessarily leads to an decrease of

total abatement cost in all states of the world. Figure 4 shows the distribution of the cost savings

due to the introduction of price bounds. Naturally, the distribution shows a high mass at zero cost

savings, i.e., the probability of non-binding price controls is 56%. With a probability of 39% cost

savings are realized, however, with a 5% probability cost are increasing. In total, expected cost

savings are equal to 0.25 Billion $.

Summarizing,the introduction of price bounds decreases the excess cost due to uncertainty by

approximately one half. The regulator uses the additional instrument to decrease cost uncertainty

in the trading sector at the expense of increasing uncertainty in the non-trading sector. This behavior makes intuitively sense, as the trading sector is bearing the main abatement burden. As

uncertainty is increasing in the abatement burden, the trading sector is also bearing the main un14

certainty which is decreased using the price collar.

5. Conclusions

This paper examined the introduction of a permit price collar in a hybrid regulation scheme

under uncertainty over future marginal abatement cost. Assuming a constant abatement burden,

a binding price floor or collar implies shifting abatement burden from one regulation scheme to

the other. Thus, the price collar introduces state contingency of the ex-post abatement burden.

We showed that the mechanism has the potential to decrease expected abatement cost in a save

way, i.e., without the risk of increasing expected cost. In order to implement such an scheme the

regulator needs to have access to an estimate of the distribution of abatement cost functions in the

respective sectors. As such uncertainty assessments are part of nearly policy impact assessments,

we see this as an rather low information requirement.

We quantitatively analyzed the implications of introducing price bounds in a stylized model of

the EU ETS. The results show that the excess cost of regulation under uncertainty can be reduced

by approximately one half. As the trading sector carries the main abatement burden and the optimal allocation of the abatement burden and as uncertainty in the abatement cost is increasing in

the abatement burden, the trading sector also bears the main cost uncertainty in a pure emission

trading system. The optimal price bounds decrease this uncertainty at the expense of increasing

the risk in the non-trading sector.

Acknowledgments

We thank Renger van Nieuwkoop we very helpful discussions and constructive comments.

We acknowledge the support of the Swiss Competence Centers for Energy Research, Competence

Center for Research in Energy, Society and Transition (SCCER-CREST) and the Commission for

Technology and Innovation (CTI).

References

Abrell, J. (2010). Regulating CO2 emissions of transportation in europe: a cge-analysis using market-based instruments. Transportation Research Part D: Transport and Environment, 15, 235–239.

Armington, P. (1969). A theory of demand for products distinguished by place of production. International Monetary

Fund Staff Papers, 16, 159–76.

Böhringer, C., Dijkstra, B., & Rosendahl, K. E. (2014). Sectoral and regional expansion of emissions trading. Resource and Energy Economics, .

Böhringer, C., Hoffmann, T., & Manrique-de Lara-Penate, C. (2006). The efficiency costs of separating carbon

markets under the eu emissions trading scheme: A quantitative assessment for germany. Energy Economics, 28,

44–61.

Böhringer, C., & Rosendahl, K. E. (2009). Strategic partitioning of emission allowances under the eu emission trading

scheme. Resource and energy economics, 31, 182–197.

Caillaud, B., & Demange, G. (2005). Joint desing of emission tax and trading systems. PSE Working Paper, 2005-03.

Collinge, R. A., & Oates, W. E. (1982). Efficiency in pollution control in the short and long runs: A system of rental

emission permits. Canadian Journal of Economics, 15, 346–354.

Commission, E. (2008). The 2020 climate and energy package. http://ec.europa.eu/clima/policies/package/index en.htm,

accessed on Jan 2015.

15

Commission, E. (2014). Proposal for a decision of the european parliament and of the council concerning the establishment and operation of a market stability reserve for the union greenhouse gas emission trading scheme and

amending directive 2003/87/ec. http://ec.europa.eu/clima/policies/ets/reform/docs/com 2014 20 en.pdf.

Dijkstra, B. R., Manderson, E., & Lee, T.-Y. (2011). Extending the sectoral coverage of an international emission

trading scheme. Environmental and Resource Economics, 50, 243–266.

Dirkse, S. P., & Ferris, M. C. (1995). The PATH solver: a non-monontone stabilization scheme for mixed complementarity problems. Optimization Methods and Software, 5, 123–156.

Drud, A. (1985). CONOPT: A GRG code for large sparse dynamic nonlinear optimization problems. Mathematical

Programming, 31, 153–191.

Hyman, R., Reilly, J., Babiker, M., Valpergue De Masin, A., & Jacoby, H. (2002). Modeling non-co2 greenhouse gas

abatement. Environmental Modeling and Assessment, 8, 175–186.

Klepper, G., & Peterson, S. (2006). Marginal abatement cost curves in general equilibrium: The influence of world

energy prices. Resource and Energy Economics, 28, 1–23.

Luo, Z.-Q., Pang, J.-S., & Ralph, D. (1996). Mathematical programs with equilibrium constraints. Cambridge

University Press.

Mathiesen, L. (1985). Computation of economic equilibria by a sequence of linear complementarity problems. Mathematical Programming Study, 23, 144–162.

Narayanan, G., Badri, A., & McDougall, R. (Eds.) (2012). Global Trade, Assistance, and Production: The GTAP 8

Data Base. Center for Global Trade Analysis, Purdue University.

Paltsev, S., Jacoby, H. D., Reilly, J. M., Viguier, L., & Babiker, M. (2005a). Transport and climate policy modeling

the transport sector: The role of existing fuel taxes in climate policy. Springer.

Paltsev, S., Reilly, J. M., Jacoby, H., Eckhaus, R., McFarland, J., Sarofim, M., Asadoorian, M., & Babiker, M. (2005b).

The MIT emissions prediction and policy analysis (EPPA) model: Version 4. MIT Joint Program on the Science

and Policy of Global Change, Report 125, Cambridge, MA.

Pizer, W. A. (2002). Combining price and quantity controls to mitigate global climate change. Journal of Public

Economics, 85, 409–434.

Roberts, M. J., & Spence, M. (1976). Effluent charges and licenses under uncertainty. Journal of Public Economics,

5, 193–208.

Rutherford, T. F. (1995). Extension of GAMS for complementarity problems arising in applied economics. Journal

of Economic Dynamics and Control, 19, 1299–1324.

Unold, W., & Requate, T. (2001). Pollution control by options trading. Economics Letters, 73.

Weitzman, M. L. (1974). Prices vs. quantities. The Review of Economic Studies, 41(4), 477–491.

16

Appendix

Appendix A. Proof of Proposition 1

We proof the first part of the proposition for the case of price floor. For a price ceiling, the

proof proceeds along the same reasoning.

We distinguish two cases. First, if Pmin ≤ PT , the price floor is non-binding, and hence does

not affect firms’ abatement behavior. Consequently, abatement in each sector stays constant and

total abatement cost are unchanged.

Second, with a binding price floor (Pmin > PT ) , a constant environmental target (de = 0)

implies that the change of abatement in one of the sectors needs to be offset by the change in the

T

other.daT = −daNT . The first-order condition for emissions abatement in sector T is PT = ∂C

∂aT

implying that a change of the permit price in sector T leads to a change in abatement:

daT =

dPT / ∂∂aC2T . The corresponding change of the fulfillment factor is given by dλ = dPT / ∂∂aC2T a . Thus,

T

T

an increase in the price floor induces an increase in the fulfillment factor, i.e., more abatement in

the trading sector. Differentiating the regulator’s

h ∂Cobjective

i(1) for a given state with respect to the

∂C NT

∂C

T

price in sector T and substituting yields: ∂PT = ∂aT − ∂aNT ∂21CT = [PT − PNT ] ∂21CT . Introducing a

2

2

∂a2

T

∂a2

T

binding price floor below the optimal price implies that PT < PNT . As ∂Ci /∂ai > 0 and ∂2Ci /∂a2i >

∂C

0, it follows that ∂P

> 0. Hence, introducing a binding price floor decreases total abatement costs.

T

Appendix B. Derivation of first-order conditions for regulator’s optimization problem (5)

Using Leibniz’s rule, the derivative of the expected cost function with respect to the fulfillment

factor becomes:

#

Z η(λ) "

∂η

∂C

∂CT ∂C NT

=

−

f (η) dη + f (η) (CT + C NT )

∂λ

∂AT ∂ANT

∂λ

−b

η=η, λ=λ∗

#

Z η(λ) "

∂η

∂CT ∂C NT

−

f (η) dη − f (η) (CT + C NT )

+

∂AT ∂ANT

∂λ

η(λ)

η=η, λ=λ∗

"

#

Z

b

∂η

∂CT ∂C NT

+ f (η) (CT + C NT )

+

−

f (η) dη

∂λ

∂ANT

η(λ) ∂AT

η=η, λ=λ∗

∂η

− f (η) (CT + C NT )

∂λ

η=η, λ=λ∗

#

Z b"

∂CT ∂C NT

=

−

f (η) dη

∂ANT

−b ∂AT

"

#

∂CT ∂C NT

=E

−

∂AT ∂ANT

17

Similarly, the derivative with respect to the price floor is given as:

#

"

Z η(λ)

∂η

∂C

∂λ ∂CT ∂C NT

−

f (η) dη + f (η) (CT + C NT )

=

∂P

∂P ∂AT ∂ANT

∂P

−b

η=η, λ=λ∗

∂η

− f (η) (CT + C NT )

∂P

η=η, λ=λ∗

"

#

Z η(λ)

∂λ ∂CT ∂C NT

=

−

f (η) dη

∂P ∂AT ∂ANT

−b

!

∂C NT 1

= E ∂2C P −

η ≤ η

a 2T

∂ANT ∂a

T

Where we used the first order condition of the trading sector in the case of binding price constraint

and the derivative of the fulfillment factor with respect to a price constraint (derived in Proposition

1). The derivative of the expected cost function with respect to the price ceiling can be equivalently

derived.

Appendix C. Equilibrium conditions for Numerical General Equilibrium Model

In this Appendix we present the equilibrium conditions of the macro-economic CGE model.

We employ numerical methods to solve for general equilibrium prices and quantities. More specifically, we formulate the model as a system of nonlinear inequalities and represent the economic

equilibrium through two classes of conditions: zero profit and market clearance. The former class

determines activity levels and the latter determines price levels. In equilibrium, each of these variables is linked to one inequality condition: an activity level to an exhaustion of product constraint

and a commodity price to a market clearance condition. Following Mathiesen (1985) and Rutherford (1995), we formulate the model as a mixed complementarity problem. A characteristic of

many economic models is that they can be cast as a complementary problem, i.e. given a function

F: Rn −→ Rn , find z ∈ Rn such that F(z) ≥ 0, z ≥ 0, and zT F(z) = 0, or, in short-hand notation,

F(z) ≥ 0 ⊥ z ≥ 0. The complementarity format embodies weak inequalities and complementary

slackness, relevant features for models that contain bounds on specific variables, e.g. activity levels which cannot a priori be assumed to operate at positive intensity. Numerically, we solve the

model in GAMS using the PATH solver (Dirkse & Ferris, 1995).

According to Figure 3.1 we define the expenditure function cCON as:

h

i 1ctop

ctop

ctop

cCr := θCON

(cCENE

)1−σ + 1 − θCON

(cCCON

)1−σ 1−σ

r

r

r

r

!1−σcene 1−σ1cene

X

PAE

ir

CENE

cCENE

:=

θ

r

ir

pae

ir

i∈cene

! ccon 1

X CON PAEir 1−σ 1−σccon

CCON

θir

cr

:=

pae

ir

i∈ccon

18

(C.1)

(C.2)

(C.3)

cCr denotes the private expenditure function in region r and cCENE

and cCCON

the sub-level expenr

r

CON

diture functions. θ generally refers to share parameters. Thus, θr

denotes the budget share of

energy commodities in the total expenditure of the consumer living in region r. Similarly, θCENE

ir

and θCON

refer

to

the

expenditure

share

of

commodity

i

in

the

energy

and

non-energy

expendiir

ture in region r. The set ene and con are used to identify energy and non-energy consumption

commodities. PAEir denotes the tax inclusive Armington prices defined as:12

PAEir := (1 + tiir ) PAir

(C.4)

Prices denoted with an upper bar generally refer to baseline prices observed in the benchmark

equilibrium.

Unit cost functions for productions are given as:

1top

!1−σtop

X

X

1−σ

PAE

top

jr

ytop

ytop

V

AE

1−σ

cir :=

− 1 −

θ jir

θ jir (cir )

pae

jr

j∈mat

j∈mat

h

i 1vae

vae

vae

cVir AE := θirV AE (cVir A )1−σ + 1 − θirV AE (cirENE )1−σ 1−σ

1−σva

1−σva 1−σ1 va

(1

+

tl

)PL

(1

+

tk

)PK

ir

r

ir

r

cVir A := θirV A

+ 1 − θirV A

plir

pkir

1−σ1ene

!1−σene

X

X

PAE

ene

jr

ENE

FOF 1−σ

1 −

cirENE :=

θ ENE

+

θ

(c

)

jir

jir

pae

jr

j∈ele

j∈ele

!1−σ f o f 1−σ1f o f

X

PAE

jr

cirFOF :=

θ FOF

jir

pae

jr

j∈ f o f

(C.5)

(C.6)

(C.7)

(C.8)

(C.9)

For government and investment consumption, fixed production shares are assumed:

cGr :=

X

θGir

PAEir

paeir

(C.10)

θirI

PAEir

paeir

(C.11)

i

crI :=

X

i

Trading commodity i from region r to region s requires the usage of transport margin j. Accordingly, the tax and transport margin inclusive import price for commodity i produced in region

r and shipped to region s is given as:

PMirs := (1 + teir ) PYir + φTjirs PT j

12

(C.12)

The price also includes carbon cost which we skip for the ease of notation. Furthermore, taxes are differentiated

by agent which we also neglect in the algebraic exposition in order to suppress an additional index.

19

teir is the export tax raised in region r and θTjirs is the amount of commodity j needed to transport

the commodity. We assume that imports from different regions are imperfect substitutes as well

as the import commodity bundle is and imperfect substitute to domestic produced commodities.

Thus, the unit cost index for the Armington commodity becomes:

h

i 1dm

dm

dm

cirA := θirA PYir1−σ + 1 − θirA (cirM )1−σ 1−σ

!1−σm 1−σ1 m

X

PM

is

cirM := θisM (1 + tmir )

pm

is

s

(C.13)

(C.14)

International transport services are assumed to be produced with transport services from each

region according to a Cobb-Douglas function:

Y θT

cTi :=

PYisis

(C.15)

s

According to these function definitions, the zero-profit conditions for the model can be written

as:

cir ≥ PYir

⊥ Yir ≥ 0

∀i, r

(C.16)

cCr

cGr

crI

cirA

cTi

≥ PCr

⊥ Cr ≥ 0

∀r

(C.17)

≥ PGr

⊥ Gr ≥ 0

∀r

(C.18)

≥ PIr

⊥

Ir ≥ 0

∀r

(C.19)

≥ PAir

⊥

Air ≥ 0

∀i, r

(C.20)

≥ PT i

⊥ Ti ≥ 0

∀r

(C.21)

Yir denotes the production index of sector i in region r. Cr is the consumption index and PCr the

corresponding consumer price index in region r. Similarly, Gr and Ir are the public and investment

activity indexes and PGr and PIr the corresponding price indexes. Air is the Armington index and

T i the production evel of international transport service i

Denoting consumers’ initial endowments of labor and capital as Lr and K r , respectively, and

20

using Shephard’s lemma, market clearing equations become:

Yir

Air

Lr

Kr

X ∂cA

∂cTi

is

≥

Ais +

Ti

∂PYir

∂PYir

s

X ∂c jr

∂cCr

∂cGr

∂crI

≥

Y jr +

Cr +

Gr +

Ir

∂PAir

∂PAir

∂PAir

∂PAir

j

X ∂cir

≥

Yir

∂PLr

i

X ∂cir

≥

Yir

∂PKr

i

Ti ≥

X ∂cAjr

j,r

∂PT i

A jr

Ir ≥ ir

INCrC

Cr ≥

PCr

INCrG

Gr ≥

PGr

⊥

PYir ≥ 0

∀i, r

(C.22)

⊥

PAir ≥ 0

∀i, r

(C.23)

⊥

PLr ≥ 0

∀r

(C.24)

⊥

PKr ≥ 0

∀r

(C.25)

⊥

PT i ≥ 0

∀r

(C.26)

⊥

PIr ≥ 0

∀r

(C.27)

⊥

PCr ≥ 0

∀r

(C.28)

⊥

PGr ≥ 0

∀r

(C.29)

ir is the investment level in the benchmark equilibrium which is assumed to be constant across all

scenarios; INCrC and INCrG are the private and public income in region r. Private income is given

as factor income net of investment expenditure and a lumpsum or direct tax payment to the local

government, htaxr . Public income is given as the sum of all tax revenues:

INCrC :=PLr Lr + PKr K r − PIr ir − htaxr

C

G

I

X

X ∂c jr

∂c

∂c

∂c

r

r

r

INCrG :=

tiir PAir

Y jr +

Cr +

Gr +

Ir

∂PAir

∂PAir

∂PAir

∂PAir

i

j

"

#

X

∂cir

∂cir

+

Yir tlr PLr

+ tkr PKr

∂PLr

∂PKr

i

"

#

A

X

∂cis

∂cirA

+

teir PYir

Ais + tmir (1 + teis ) PYis

Air

∂PYir

∂PYis

i,s

+ htaxr

(C.30)

(C.31)

(C.32)

(C.33)

(C.34)

Appendix D. Computational Strategy for Price-Bound Computation

Marginal abatement cost functions of the trading and non-trading sector i ∈ {T, NT } are assumed to be cubic. Accordingly, we define the total and marginal abatement cost functions for a

21

given state of the world s ∈ S as:

αis 2 βis 3 γis 4

A + A + A

2 is 3 is 4 is

Cis0 (Ais ) := αis Ais + βis A2is + γis A3is ,

Cis (Ais ) :=

(D.1)

(D.2)

where the coefficients αis , βis , and γis are obtained by our sampling procedure (see Section 3.1)

and Ais denotes abatement taking place in sector i in state s. The probability of state s is denoted

P

as π s and sums to one over all states ( s π s = 1).

Appendix D.1. First-Best

In the first-best situation, the regulator is able to choose abatement for each sector in each state

of the world. I.e., the regulator directly chooses Ais minimizing expected total abatement cost by

fulfilling the total abatemetn requirement a:

X X

min

πs

Cis (Ais )

(D.3)

s

s.t.

s

X

Ais ≥ a

(P s )

∀s

(D.4)

i

Ais ≥ 0

(D.4) ensures sufficient abatement in each state s and the associated dual variable P s is interpreted

as the (uniform) optimal first-best emission permit price. This states an non-linear problem (NLP)

which can be solved by standard techniques.13

Appendix D.2. Pure Quantity Control

In the second-best situation the regulator has to choose sectors’ abatement quantities before

the revelation of uncertainty. Denoting ex-ante abatement burdens by Ai , the regulator minimizes

total expected cost:

X X

min

πs

Cis (Ais )

(D.5)

s

s.t.

Xs

Ai ≥ a

(P)

(D.6)

∀i, s

(D.7)

i

(Pis )

Ais ≥ Ai

Ai , Ais ≥ 0

. (D.6) ensures that the total abatement requirement is achieved and the associated dual variable

P is the expected permit price. (D.7) ensures that abatement in each scenario equals the ex-ante

chosen sectoral requirements. The associated dual variable are sectoral ex-post carbon prices. This

NLP can also be solved using standard techniques.

13

We use the CONOPT solve (Drud, 1985) to solve NLP problems.

The problem is separable in the set of states. Thus, it could be solved by equating MAC for each state separately.

22

Appendix D.3. Quantity Control with Price Bounds

Extending the set of choice variables by allowing for price bounds and an associated rationing

mechanism, requires choosing the condition (i.e. the integral bounds) in (5). Put differently, we

need to implement a rationing mechanism that shifts abatement burden from one sector to the

other in the case of a binding price bound. Let P and P denote the the upper and lower permit

price bound in the trading sector T and µ and µ s the respective rationing factors. The regulator’s

s

problem of minimizing expected total abatement cost becomes:14

X X

min

πs

Cis (Ais )

(D.8)

s

s.t.

Xs

Ai ≥ a

(P)

(D.9)

i

AT s ≥ AT + µ s − µ s

A(NT )s ≥ A(NT ) − µ s − µ s

⊥

⊥

PT s ≥ P

PT s ≥ 0

∀s

(D.10)

P(NT )s ≥ 0

∀s

(D.11)

⊥ µ ≥0

∀s

(D.12)

⊥ µs ≥ 0

∀s

(D.13)

s

P ≥ PT s

P, P, Ai , Ais ≥ 0

. Again, (D.9) ensures that the ex-ante allocation of the abatement burden complies with the total

abatement requirement. (D.10) and (D.10) ensure that the ex-post abatement is aligned to the exante abatement burden allocation. In that sense they are similar to (D.7) in the pure quantity control

case. However, they are formulated as complementarity constraints in order to allow for a explicit

representation of the dual variables, i.e. prices, which are restricted by the price bounds. Moreover,

they also include the rationing factors which are determined by the price constraints (D.12) and

(D.13). If, e.g., the price floor becomes binding, complementarity requires that µ > 0 becomes

s

positive and, as long as the upper bound lies above the lower, µ s = 0. Thus, the abatement burden

in the T (NT ) sector is increasing (decreasing) and, in turn, the price in the T sector is increasing.

Problem (D.8) to (D.13) falls in the class of Mathematical Problems under Equilibrium Constraints (MPEC) for which no stable general solution algorithm exists (Luo et al., 1996). Thus,

we make use of Proposition 2 to transform the program into a Mixed Complementarity Problem

(MCP) and use grid search to find optimal prices.15 From Proposition 2 (a) we know that the optimal abatement allocation is equal under quantity control with and without bounds. Consequently,

we use the pure quantity control program (D.5) to (D.7) to compute to optimal ex-ante abatement

allocation and eliminate the upper level constraint (D.9). The first order conditions of firms imply

(weak) equality of marginal cost and carbon prices. Consequently, given the ex-ante allocation

14

We use the perpendicular sign ⊥ to denote complementarity, i.e., f (x) ≥ c

0, x ( f (x) − x) = 0

15

We use the PATH solver for MCP problems (Dirkse & Ferris, 1995).

23

⊥

x ≥ 0 ⇔ f (x) ≥ c, x ≥

and permit price bounds in the T sector, the equilibrium is formulated as:

AT s ≥ aT + µ s − µ s

⊥ PT s ≥ 0

A(NT )s ≥ a(NT ) − µ s − µ s

⊥ P(NT )s ≥ 0

Cis0

∀s

(D.14)

∀s

(D.15)

PT s ≥ p

⊥ µ ≥0

∀s

(D.16)

p ≥ PT s

(Ais ) ≥ Pis

⊥ µs ≥ 0

⊥ Ais ≥ 0

∀s

∀i ∈ T, NT , s

(D.17)

(D.18)

(D.19)

s

, where (D.18) is the sectors’ first order or zero-profit condition which determines the abatement

amount. To derive optimal price bounds, we perform grid search for the price bounds and compare

total cost. The relevant range for our search is given by Proposition 2 (c).

24