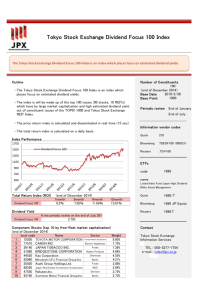

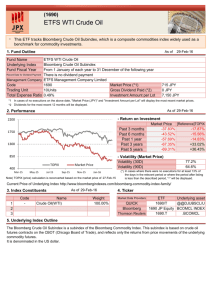

Tokyo Stock Exchange Index Guidebook

advertisement