Part 1: Accounting Changes Introduction

advertisement

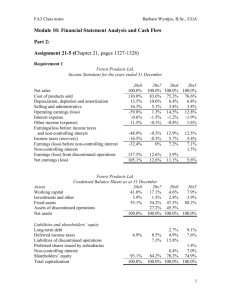

Financial Accounting: Liabilities & Equities (FA3) Module 8 Audio lecture presented by: Barbara M. Wyntjes, B.Sc., CGA FA3 Module 8 1 Part 1: Accounting Changes FA3 Module 8 2 Introduction Three types of accounting changes How to account for changes and errors Disclosure FA3 Module 8 Financial Accounting 3 Lesson summary 1 3 1 Types of Accounting Changes Three types of accounting changes: 1. Changes in accounting policy 2. Changes in accounting estimate 3. Correction of an error in previous periods’ financial statements FA3 Module 8 4 Accounting Changes Changes and errors will occur Standards set up to account for these changes FA3 Module 8 5 Accounting Changes Decrease consistency and comparability Manipulation of statements Financial statement objective Ethical litmus test User’s perspective FA3 Module 8 Financial Accounting 3 Lesson summary 1 6 2 Changes in Accounting Policy A change in the ‘way’ that a company accounts for a transaction, event, or the resulting asset or liability Voluntary - changes are made as a result of management decision Non voluntary - decision is the result of outside influences (change in the Accounting Standard recommendations). Ex: Goodwill FA3 Module 8 7 Changes in Accounting Policy Only if new policy is reliable and MORE relevant Reasons for voluntary changes: reporting objectives comply with the industry norm change way of doing business FA3 Module 8 8 Changes in Accounting Estimate Change is NOT a change in policy if the change in policy is based on a change in circumstances, experience or new information Example: Regular review of amortization suggests another method would better reflect usage FA3 Module 8 Financial Accounting 3 Lesson summary 1 9 3 Changes in Accounting Estimate Adopting a new accounting policy is not a change in policy if: events or transactions that are clearly different in substance from those previously recognized recognition of events or transactions occurring for the first time or that were previously immaterial in effect FA3 Module 8 10 Change in Accounting Estimate Is a change in the application of an accounting policy to a specific transaction or event Accounting measurements are based extensively on future expectations Accounting estimates often need revision because we can never predict future outcomes with certainty FA3 Module 8 11 Change in Accounting Estimate Reasons: the company’s economic environment has changed a shift in the nature of the company’s business operations new information auditors have raised questions FA3 Module 8 Financial Accounting 3 Lesson summary 1 12 4 Change in Accounting Estimate Examples: Uncollectable accounts receivable Useful lives, salvage value Fair value Recoverable value of an asset FA3 Module 8 13 Correction of Error Accidental or intentional mistake To comply with the qualitative criteria of comparability and consistency Require restatement of prior periods results Even if there is no impact on the period in which the error was discovered FA3 Module 8 14 Correction of Error Examples: Counterbalancing Miscount ending inventory Failure to accrue liabilities FA3 Module 8 Financial Accounting 3 Lesson summary 1 15 5 Correction of Error Examples: Failure to accrue assets Charge to wrong account or wrong amount FA3 Module 8 16 Correction of Error Correction depends on when error is caught Examples: Error in 2007 EI. Books not closed vs close If error not detected, 2008 BI incorrect Books not closed vs close FA3 Module 8 17 Correction of Error First classify change Apply accounting treatment FA3 Module 8 Financial Accounting 3 Lesson summary 1 18 6 Part 2: FA3 Module 8 19 Accounting for Changes Three ways of reporting accounting changes in the financial statements: 1. Retroactive application with restatement of prior period 2. Retroactive application without restatement of prior period 3. Prospective application FA3 Module 8 20 Retroactive with Restatement Recalculate from the period when the original transaction took place to reflect the change/error Restate financial statements that are used in comparative presentations Restate summary financial information for earlier periods (net income, total assets, EPS) FA3 Module 8 Financial Accounting 3 Lesson summary 1 21 7 Retroactive with Restatement Journal entries adjust balance sheet accounts directly Opening retained earnings retroactively restated Reported financial results appear as though the new policy had always been in effect or the error had never occurred Best method for changing a policy or correcting an error because it would make comparative data more relevant. FA3 Module 8 22 Retroactive without Restatement Use if Accounting Standards allow, or if the necessary data is incomplete or excessively expense to gather. Calculate the effect of the change from the period when the original transaction occurred Journalize a cumulative adjustment to change all beginning balances on accounts affected by the change in the period in which the change is made FA3 Module 8 23 Retroactive without Restatement Summary impact of the change for all periods is adjusted to beginning retained earnings in the current period Start applying new policy in current year Comparative financial statements are not restated (disclose) Financial analysis becomes unreliable and no longer compares consistent data. FA3 Module 8 Financial Accounting 3 Lesson summary 1 24 8 Retroactive Journal Entry Adjust balance sheet accounts – before-tax Adjust retained earnings – after-tax Difference creates a future income tax Example: tax rate = 40% Retained earnings 6,000 Future Income tax 4,000 Accumulated amort. 10,000 FA3 Module 8 25 Prospective The change in accounting is applied only to events and transactions occurring after the the date change Change in estimate or if Standards allow Previously reported results are not restated, and no cumulative catch-up adjustment FA3 Module 8 26 Prospective Use for changes in estimates Use for change in policy when allowed by Accounting Standards When there is doubt as to whether a change is a change in policy or a change in estimate, the CICA Handbook suggests that the change should be treated as a change in estimate (page 1217 of text) FA3 Module 8 Financial Accounting 3 Lesson summary 1 27 9 Review Exhibit 20-2 See text, page 1221 FA3 Module 8 28 Assignment A20-2 See Chapter 20, page 1249 And handout 1, page 1 FA3 Module 8 29 Summary Change in policy: new reporting objectives, conform with industry practices, meet user needs Change in estimate: new information, change in circumstances, or experience FA3 Module 8 Financial Accounting 3 Lesson summary 1 30 10 Part 3: FA3 Module 8 31 Disclosure Financial statements – communicate information to outsiders Accounting changes affect the consistency and comparability of financial statements and therefore their reliability Readers should be warned about the changes and their impacts FA3 Module 8 32 Disclosure Extensive disclosure is needed to inform financial statement users of the effect on current and past financial statements Change in policy FA3 Module 8 Financial Accounting 3 Lesson summary 1 33 11 Disclosure Change in estimate Correction of errors Review page 1234 FA3 Module 8 34 Cash Flow Accounting changes do not change cash flow May affect the way that cash flow are reported (reclassify) FA3 Module 8 35 All-inclusive Earnings Income statement represents all the changes in net assets = comprehensive income for the period Accounting changes would simply be included in the current income statement and no adjustment to retained earnings No restatement of prior periods FA3 Module 8 Financial Accounting 3 Lesson summary 1 36 12 Current Operations Income statement should reflect only items relating to the operations of the current period (not from prior periods) Recurring Predictive power FA3 Module 8 37 Current Operations Combination used in Canada FA3 Module 8 38 Part 4: Assignment A20-8 Req’d 1 See Chapter 20, page 1252 And handout 1, page 2 FA3 Module 8 Financial Accounting 3 Lesson summary 1 39 13 Assignment A20-8 Req’d 2 See Chapter 20, page 1252 And handout 1, page 2 FA3 Module 8 40 Assignment A20-8 Req’d 3 See Chapter 20, page 1252 And handout 1, page 2 FA3 Module 8 41 Part 5: FA3 Module 8 Financial Accounting 3 Lesson summary 1 42 14 Error - expensed capital asset Expensed capital asset on date of purchase Catch-up journal entry: record cost of capital asset and accumulated amortization Adjust opening retained earnings for net increase to date (cost – amortization expense that should have been recorded to date) FA3 Module 8 43 Class Example 1 See handout 1, page 3 FA3 Module 8 44 Part 6: Assignment A20-21 Req’d 1 See Chapter 20, pages 1258-1259 And handout 1, page 4 FA3 Module 8 Financial Accounting 3 Lesson summary 1 45 15 Assignment A20-21 Req’d 2 See Chapter 20, pages 1258-1259 And handout 1, page 4 FA3 Module 8 46 Assignment A20-21 Req’d 3 See Chapter 20, pages 1258-1259 And handout 1, page 4 FA3 Module 8 47 Assignment A20-21 Req’d 4 See Chapter 20, pages 1258-1259 And handout 1, page 4 FA3 Module 8 Financial Accounting 3 Lesson summary 1 48 16 Part 7: Assignment A20-24 Req’d 1 See Chapter 20, page 1260 And handout 1, pages 5-6 FA3 Module 8 49 Assignment A20-24 Req’d 2 See Chapter 20, page 1260 And handout 1, pages 5-6 FA3 Module 8 50 Assignment A20-24 Req’d 3 See Chapter 20, page 1260 And handout 1, pages 5-6 FA3 Module 8 Financial Accounting 3 Lesson summary 1 51 17 Assignment A20-24 Req’d 4 See Chapter 20, page 1260 And handout 1, pages 5-6 FA3 Module 8 52 Assignment A20-24 Req’d 5 See Chapter 20, page 1260 And handout 1, pages 5-6 FA3 Module 8 53 Part 8: Past Exam Questions: See Module 8 Handout 2 FA3 Module 8 Financial Accounting 3 Lesson summary 1 54 18 Blueprint: 6-10% Multiple Choice and long answer Past exam questions are NOT changed to reflect current material FA3 Module 8 55 Multiple Choice m See Module 8 Handout 2 FA3 Module 8 56 Multiple Choice n See Module 8 Handout 2 FA3 Module 8 Financial Accounting 3 Lesson summary 1 57 19 Multiple Choice o See Module 8 Handout 2 FA3 Module 8 58 Question 4a See Module 8 Handout 2 FA3 Module 8 59 Question 4b See Module 8 Handout 2 FA3 Module 8 Financial Accounting 3 Lesson summary 1 60 20 Question 4c See Module 8 Handout 2 FA3 Module 8 61 End of presentation FA3 Module 8 Financial Accounting 3 Lesson summary 1 62 21