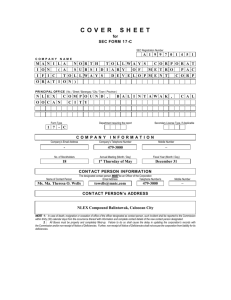

14chapter 14

advertisement