How 3 Small Firms Are Coping With Health Law - WSJ.com

Dow Jones Reprints: This copy is for your personal, non -commercial use only. To order presentation-ready copies for distribution to your colleagues, clients or

customers, use the Order Reprints tool at the bottom of any article or visit www.djreprints.com

See a sample reprint in PDF format.

SMALL BUSINESS

Order a reprint of this article now

Updated May 29, 2013, 8:25 p.m. ET

How 3 Small Firms Are Coping With Health Law

By EMILY MALTBY and SARAH E. NEEDLEMAN

Small employers are struggling to make heads or tails of their health-care costs under the Affordable Care

Act. Sarah Needleman joins the News Hub with a look at their back-of-the-envelope calculations. Photo:

Jason Henry for The Wall Street Journal.

Small employers across the U.S. are struggling to get a handle on their health-care costs under the

Affordable Care Act.

Many of them say they expect their operating expenses to

jump in 2014, when the law's employee health-insurance

requirements take effect. But they acknowledge that their

forecasts are back-of-the-envelope calculations based on

only partial information.

Companies with fifty or more full-time employees

will soon have choices to make to comply with the

Affordable Care Act. WSJ’s Jason Bellini breaks

down the options.

Starting next year, the federal government will impose

penalties on any business with 50 or more full-time

equivalent employees that doesn't provide adequate

health-insurance coverage to workers who clock 30 or

more hours a week.

http://online.wsj.com/article/SB10001424127887324031404578483482290350740.html#printMode[5/30/2013 8:39:39 AM]

How 3 Small Firms Are Coping With Health Law - WSJ.com

Live Video Chat

@WSJSMALLBIZ: Have questions about how

the health-care law will impact your small

business? Join a live video chat Thursday at

noon EDT with Linda Sheppard, special

counsel for the Kansas Insurance Department;

Deborah Chollet, a senior fellow at

Mathematical Policy Research in Washington,

D.C.; and Paula Wilson, an insurance agent in

Temecula, Calif. Email questions in advance to

chat moderator Sarah E. Needleman at

sarah.needleman@wsj.com.

If such employers choose not to offer health coverage,

they will face a penalty of $2,000 for each full-time

worker, excluding the first 30.

If they do offer coverage, but the insurance doesn't meet

the law's minimum requirements, they face a penalty of

$3,000 for each worker who gets a federal subsidy

through state insurance exchanges.

Owners with between 50 and 200 full-time employees are

in a particularly tough spot. These businesses are big

enough to meet the government's threshold for penalties, but they lack the purchasing power to

negotiate the best rates with insurers.

The Obama administration says the law will help small

employers. It will let them "pool risk with other small

businesses to get more competitive rates, says Erin

Shields Britt, a spokeswoman for the Department of

Health and Human Services, through new small-business

insurance marketplaces, known as "exchanges," which are

expected to open this fall.

Here's a look at how three small employers are bracing for

the change:

Pickle for a Pizza Chain

Business: Ziegler's NYPD LLC, Phoenix

Rough Calculations: The local pizza chain figures providing health coverage could cost up to

$250,000 next year.

Options Considered: Using automation to boost productivity and buying less expensive

ingredients and supplies.

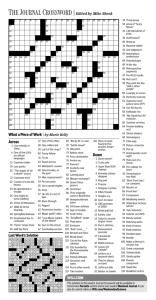

"We don't want to curtail expansion plans" because of the health-care law, says president Richard

Stark. But the business will need to find a way to absorb the law's costs.

Currently, the pizza chain doesn't offer its 350 workers an employer-sponsored health-insurance

plan. It does offer its 40 salaried managers reimbursements if they obtain health-insurance

coverage elsewhere.

Mr. Stark was a loyal patron of NYPD—short for New York

Pizza Department—for three years before becoming a part

owner in 2000.

The 58-year-old, who has a professional food-service

background, consulted the two brothers who founded

NYPD and helped them open a second location. Mr. Stark

became the majority owner in 2008. NYPD now has 11

locations, and Mr. Stark says he is on track to double the

http://online.wsj.com/article/SB10001424127887324031404578483482290350740.html#printMode[5/30/2013 8:39:39 AM]

How 3 Small Firms Are Coping With Health Law - WSJ.com

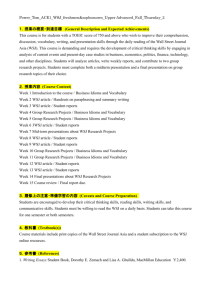

Brandon Sullivan for The Wall Street Journal

number of locations within five years.

Richard Stark, right, president of a small pizza

chain in Phoenix, says he doesn't want health

costs to curtail the business's expansion.

Next year, Mr. Stark intends to offer a health-insurance

plan for the first time to comply with the law. "At the end

of the day, if we take care of our team members, they will

take care of the guests," he says. "I philosophically believe people having health care, regardless of

age, is positive."

But it could be expensive. In addition to its 40 managers, NYPD has 90 hourly workers—mostly

kitchen staff—who are considered full-time under the law and who would therefore be eligible for

the benefits.

Mr. Stark isn't sure how many of those workers will opt into the company's new plan, considering

that most are younger, healthier and lower-paid workers who might go on a parent or a spouse's

plan, or who may forgo insurance coverage and pay a minimal penalty.

A Company Decides Health Coverage

Follow the decision-making process of a

small-business CEO as he explores options

for his company under the Patient Protection

and Affordable Care Act.

One way to offset the new expense is to negotiate with

vendors for lower-cost ingredients and packaging, such as

pizza boxes. Mr. Stark also plans to streamline business

operations, perhaps by preparing some items like sauces

and dressings at an off-site location, and by investing in

equipment like dough mixers and vegetable slicers to

automate certain tasks, he says.

Employees may see less take-home pay "because their

total compensation is increasing, from our perspective," if

they take health benefits, Mr. Stark says. Managers'

bonuses are tied to company profits, so if the law erodes

profit, managers may get smaller bonuses, he says.

More photos and interactive graphics

And as a last resort, NYPD would raise prices of some

menu items, Mr. Stark says.

"We will have to work smarter to be more efficient and

more profitable," he says. "We will need to find the pennies and nickels and dimes everywhere."

Consultant Asks a Broker

Business: Future State Inc., Walnut Creek, Calif.

Rough calculations: Health-care costs could rise by $200,000 to about $400,000 a year.

Options considered: Dropping insurance and paying a $2,000-per-employee penalty.

"I could make more money in the short term if I cut benefits," says Steven Laine, president and

chief executive of business consulting firm Future State, but he fears he would lose employees.

His 93-person firm now pays more than 50% of the premiums for 32 employees who currently take

the coverage it offers, spending roughly $200,000 total a year.

If all 77 full-timers were to participate in the company's plan next year, its health-care costs likely

would more than double, he says. But he doesn't know how many will join the company plan, which

http://online.wsj.com/article/SB10001424127887324031404578483482290350740.html#printMode[5/30/2013 8:39:39 AM]

How 3 Small Firms Are Coping With Health Law - WSJ.com

makes it very difficult to estimate and plan for the costs.

"Some of the folks have other sources of insurance, like a

spouse," he says. "But right now I can't predict how many

that might be."

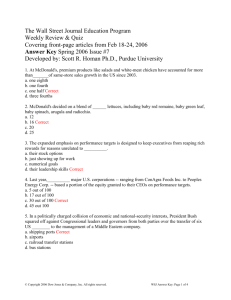

Jason Henry for The Wall Street Journal

Steven Laine, CEO of a consulting firm in

Walnut Creek, Calif., decided against dropping

health coverage, partly for fear of losing

employees.

Mr. Laine, 52, a University of California Los Angeles

graduate with three children, says he spoke to his

insurance broker in December and was told that when he

renews his company's health plan for 2014, his premiums

could go up by anywhere from 15% to 60%—regardless of

whether more employees choose to be covered by his firm.

"The message is, 'We really don't know; we have no way to

predict for you what it will cost in any reasonable way,' "

he says.

On the other hand, his firm could drop insurance, and face $94,000 in penalties. But the decision is

a lot more complicated than which option is cheaper. Insurance benefits are tax-free, and a lot of

firms don't want to risk losing workers to competitors—or getting bad publicity for ditching

coverage.

Mr. Laine is worried that it would be difficult to attract or retain staffers without a health plan.

Moreover, dropping insurance "fundamentally goes against our organization's values," he says.

IT Firm Foresees an Edge

Business: Pro Computer Service LLC, Moorestown, N.J.

Rough calculations: Premiums stabilize, or perhaps even decrease.

Options Considered: No changes because the company hopes it will gain a competitive boost.

Anthony W. Mongeluzo believes the health law will lower and stabilize insurance premiums for his

13-year-old information-technology-services firm. He also thinks it could give his business a leg up

against rivals.

Mr. Mongeluzo, the company's 32-year-old president, has roughly 40 employees today, but since his

firm is growing—he says revenue is on track to reach $7 million in 2013, up from $6 million last

year—he is hiring. He expects his head count to be above 50 by January, when the employer

provisions of the health law go into effect.

The company already offers a health-insurance plan that covers hospitalizations, doctor visits,

maternity care and prescriptions, so the law "isn't going to hit my wallet," he says.

Related

Insurance Bills Could Be Lower for Some

Firms

Bringing Workers Into the Loop Early

Mr. Mongeluzo relies on technology and streamlined

business processes to keep his overhead low, so he can

afford to cover 55% of premiums for employees and their

families.

"My understanding from talking to my broker is that we

will be in compliance" with the law, he adds.

http://online.wsj.com/article/SB10001424127887324031404578483482290350740.html#printMode[5/30/2013 8:39:39 AM]

How 3 Small Firms Are Coping With Health Law - WSJ.com

Under the health law, insurers must justify to regulators any plans to increase premiums more than

10% a year. For this reason, Mr. Mongeluzo, who started Pro Computer Service after graduating

from college in 2000, says he doesn't expect his firm's future premiums to increase as much as they

have in the past, an average of roughly 20% a year.

Mr. Mongeluzo says he has always offered his employees health benefits, in part because he believes

it helps with retention, and he stresses that turnover at his firm is low.

His staff also enjoys regular office videogame competitions. "You'll see squishy balls flying around

the office," he says, adding that he is a pretty eccentric entrepreneur, often working out of a sportutility vehicle retrofitted with a three-foot-long desk, two computer screens, a fax machine and

shredder.

Because many of his competitors currently don't provide health benefits to their employees, he

thinks some will be forced to raise prices, or lay off workers to avoid the law. That, he figures, might

give him the opportunity to offer lower rates than his rivals and land more clients.

—Christopher Weaver contributed to this article.

Write to Emily Maltby at emily.maltby@wsj.com and Sarah E. Needleman at

sarah.needleman@wsj.com

A version of this article appeared May 30, 2013, on page B1 in the U.S. edition of The Wall Street

Journal, with the headline: Sizing Up Health Costs.

Copyright 2012 Dow Jones & Company, Inc. All Rights Reserved

This copy is for your personal, non-commercial use only. Distribution and use of this material are governed by our Subscriber Agreement and by

copyright law. For non-personal use or to order multiple copies, please contact Dow Jones Reprints at 1-800-843-0008 or visit

www.djreprints.com

http://online.wsj.com/article/SB10001424127887324031404578483482290350740.html#printMode[5/30/2013 8:39:39 AM]