Intermediate Accounting II, ACCT 3322 Solutions to Review

advertisement

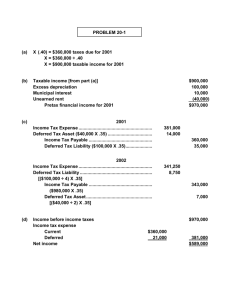

Intermediate Accounting II, ACCT 3322 Solutions to Review Questions for Chapters 15 and 16 Exercise #1 Spencer Company leases equipment to its customers under direct-financing leases. Typically the equipment has no residual value at the end of the lease and the contract call for payments at the beginning of each year. Spencer’s target rate of return is 10%. On a ten-year lease of equipment with a fair value of $1,351,805, the annual payments would be how much? How much interest will Spencer Company earn over the life of the lease? PV 1,351,805 R R = = = = R 1,351,805 200,000 Pmt * Periods 200,000 * 10 Less PV of minimum lease payments Interest expense Date 1 1 2 3 4 5 6 7 8 9 10 Payment $200,000 200,000 200,000 200,000 200,000 200,000 200,000 200,000 200,000 200,000 $2,000,000 Interest $115,181 106,699 97,369 87,105 75,816 63,398 49,737 34,711 18,179 $648,195 * * ÷ PVAD, n = 10, i = 10% 6.75902 6.75902 = = Total Payments $2,000,000 1,351,805 $648,195 Principal $200,000 84,819 93,301 102,631 112,895 124,184 136,602 150,263 165,289 181,821 $1,351,805 Page 1 Balance $1,351,805 1,151,805 1,066,986 973,685 871,054 758,159 633,975 497,373 347,110 181,821 0 Exercise #2 Spencer Manufacturing leased equipment to Sophia Company on September 1, 2001. Spencer recorded the lease as a sales-type lease at $405,391, the present value of the minimum lease payments discounted at 5%. The lease called for 10 annual lease payments of $50,000 due at the beginning of each year. The first payment was received on September 1, 2001. Spencer had manufactured the equipment at a cost of $182,425. The total pretax earnings in 2001 to Spencer as a result of this lease contract would be: Sales price Cost of goods sold Gross profit $405,391 182,425 $222,966 PV of minimum lease payments Initial payment Carrying value at inception Annual interest rate Annual interest earned Short period Interest earning in short period Increase in pretax earnings Date 9/1/01 9/1/01 9/1/02 9/1/03 9/1/04 9/1/05 9/1/06 9/1/07 9/1/08 9/1/09 9/1/10 Payment $50,000 50,000 50,000 50,000 50,000 50,000 50,000 50,000 50,000 50,000 $500,000 405,391 50,000 355,391 5% 17,770 4/12 5,923 $228,889 Interest $17,770 $16,158 $14,466 $12,689 $10,824 $8,865 $6,808 $4,649 $2,380 $94,609 Page 2 Principal $50,000 32,230 33,842 35,534 37,311 39,176 41,135 43,192 45,351 47,620 $405,391 Balance $405,391 355,391 323,161 289,319 253,785 216,474 177,298 136,163 92,971 47,620 0 Exercise #3 Spencer Company had taxable income of $100,000 in the current year. The amount of MACRS depreciation was $50,000 while the amount of depreciation reported on the income statement was $5,000. Assuming no other temporary differences What would Spencer Company’s pretax accounting income be? $145,000 Pretax accounting income Temporary differences: Accounting depreciation MACRS depreciation Excess depreciation Taxable income $5,000 50,000 (45,000) $100,000 Exercise #4 The following is a reconciliation of pretax financial statement income to taxable income for Spencer Company for the year ended December 31, 2004, its first year of operations. Pretax accounting income Interest revenue on municipal securities Warranty expense in excess of deductible amount Depreciation in excess of financial statement amount Taxable income $900,000 (10,000) 25,000 (200,000) $715,000 The company’s effective income tax rate is 25%. Prepare a schedule of deferred tax assets and liabilities at December 31, 2004. Temporary Difference Warranty expense Excess depreciation Totals Deferred Tax Future Deductable (Taxable) Amount Tax Rate Asset (Liability) 25,000 25% 6,250 (200,000) 25% (50,000) (175,000) 6,250 (50,000) Page 3 Prepare a t-account analysis of Spencer Company’s deferred tax asset as of December 31, 2004. Deferred Tax Asset Description Beginning balance Adjusting journal entry Ending balance Debit Credit 0 6,250 6,250 Prepare a t-account analysis of Spencer Company’s deferred tax liability as of December 31, 2004. Deferred Tax Liability Description Beginning balance Adjusting journal entry Ending balance Page 4 Debit Credit 0 50,000 50,000 Prepare a schedule of net deferred tax expense (benefit) for Spencer Company for the year. Analysis of net deferred tax expense: Deferred tax benefit Deferred tax expense Net deferred tax expense (6,250) 50,000 43,750 Prepare a schedule of Spencer Company’s income tax payable. Income Tax Payable Taxable income Income tax rate Income tax payable 715,000 25% 178,750 Prepare a schedule of Spencer Company’s income tax expense. Income Tax Expense Deferred tax expense Income tax payable Income tax expense 43,750 178,750 222,500 Prepare the year end journal entry to record income tax expense. Account Income tax expense Deferred tax assets Deferred tax liabilities Income tax payable Debit 222,500 6,250 Credit 50,000 178,750 Page 5 Exercise #5 Spencer Company reported the following pretax accounting income and taxable income for its first three years of operations. Pretax and Taxable Income $100,000 (500,000) 600,000 Year 2002 2003 2004 The enacted tax for all years was 35%. Spencer Company elected to carryback the original loss to 2002 and then carryforward the excess to 2004. Prepare a schedule of NOL carryback and NOL carryforward. Description 2003 NOL carryback NOL (500,000) 2003 NOL carryforward 100,000 (400,000) Taxable Year Income 2002 100,000 (100,000) 0 Tax Rate Tax Paid Refund 35% 35,000 35% 0 35,000 Prepare an analysis of the deferred tax asset. Temporary Difference NOL Carryforward Deferred Tax Future Tax Amounts Rate Asset Liability 400,000 35% 140,000 Prepare a partial balance sheet for Spencer Company at December 31, 2003 demonstrating how the effects of the NOL will be reported. Partial Balance Sheet December 31, 2003 Income tax refund receivable Deferred tax asset $35,000 140,000 Page 6 Prepare a partial income statement for Spencer Company for the year ended December 31, 2003 demonstrating how the effects of the NOL carryback and carryforward would be reported. Partial Income Statement For the Year Ended December 31, 2003 loss before income tax benefit Income tax benefit: Deferred tax benefit Current tax benefit Net loss (500,000) $140,000 35,000 175,000 (325,000) Prepare a partial income statement for Spencer Company for the year ended December 31, 2004 demonstrating how the effects of the NOL carryforward would be reported. Partial Income Statement For the Year Ended December 31, 2004 Income before income taxes Income taxes: Deferred tax expense Current tax expense Net income $600,000 $140,000 70,000 210,000 $390,000 Exercise #6 Spencer Company reports bad debt expense using the allowance method. For tax purposes the direct write-off method is used. At the end of the current year, Spencer Company has accounts receivable and an allowance for uncollectible accounts of $200,000 and $16,000 respectively, and taxable income for the year is $15,000. At the beginning of the current year, Spencer Company reported a deferred tax asset of $7,000 related to the difference in reporting bad debts, its only temporary difference. The enacted tax rate is 25% each year. Prepare an analysis of the deferred tax asset or deferred tax liability related to this temporary difference. Temporary Difference Bad debt expense Future Deductable (Taxable) Amount 16,000 Page 7 Tax Rate 25% Asset 4,000 Prepare a t-account analysis of the deferred tax asset and/or deferred tax liability account as of the end of year. Deferred Tax Asset Description Debit Beginning balance 7,000 Adjusting journal entry Ending balance 4,000 Credit 3,000 Calculate income tax payable Income Tax Payable Taxable income Income tax rate Income tax payable 15,000 25% 3,750 Calculate income tax expense Income Tax Expense Deferred tax expense Income tax payable Income tax expense 3,000 3,750 6,750 Prepare the year-end journal entry to record income tax expense. ACCOUNT Income tax expense Deferred tax asset Income tax payable To record income tax for the year DEBIT 6,750 CREDIT 3,000 3,750 Page 8 Exercise #7 Spencer Company leased a machine on December 31, 2004, for a five-year period. The lease agreement calls for annual payments in the amount of $25,000 on December 31 of each year beginning on December 31, 2004. Spencer Company has the option to purchase the machine on December 31, 2009, for $5,000 when its fair value is expected to be $15,000. The machine's estimated useful life is expected to be 10 years with no residual value. Spencer Company uses straight-line depreciation for this type of machinery. The appropriate interest rate for this lease is 8%. Calculate the amount to be recorded as a leased asset and the associated lease liability. PV of minimum lease payments: Payments PVOA, n = 5, i = 8% 1 + 8% PVAD, n = 5, i = 8% PV of minimum lease payments PV of bargain purchase option Bargain purchase PV of $1, n = 5, i = 8% PV of bargain purchase option PV of lease contract 25,000 3.99271 1.08000 4.31213 107,803 5,000 0.68058 3,403 111,206 In the space prepare the amortization schedule of 2004 and 2005. Amortization Schedule for Bond Investment Date 12/31/04 12/31/04 12/31/05 12/31/06 12/31/07 12/31/08 12/31/09 Payment 25,000 25,000 25,000 25,000 25,000 5,000 Interest 0 6,896 5,448 3,884 2,195 371 Page 9 Amortization of Principal 25,000 18,104 19,552 21,116 22,805 4,629 Balance 111,206 86,206 68,102 48,550 27,434 4,629 0 Prepare all of the necessary journal entries associated with this lease for 2004 and 2005. ACCOUNT DEBIT 111,206 CREDIT Leased asset Lease payable 111,206 To record the capitalized lease of an asset on December 31, 2004 Lease payable 25,000 Cash 25,000 To record the initial payment on the lease on December 31, 2004 Interest expense 6,896 Lease payable 18,104 Cash 25,000 To record the payment on the lease and the amortization of interest on December 31, 2005 ACCOUNT Depreciation expense Accumulated depreciation To record depreciation expense for 2005 Analysis of depreciation expense: Value of leased asset Salvage value Depreciable base Service life (economic life) Annual depreciation DEBIT 11,121 CREDIT 11,121 111,206 0 111,206 10 11,121 Page 10