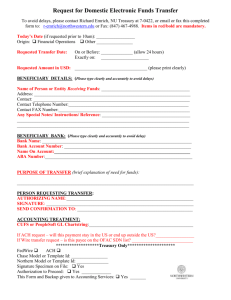

Cash Management

advertisement