What is the maximum level of income which can be sustained by an

advertisement

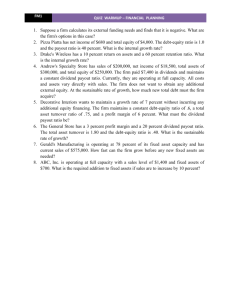

What is the maximum level of income which can be sustained by an equity income fund? By Rudi Minbatiwala, Senior Portfolio Manager, Australian Equities, Core Colonial First State Global Asset Management The stated objectives of the Colonial First State Wholesale Equity Income Fund (the Fund) are designed to provide a balance between investors’ requirements for a greater level of cash flow today and the provision of modest growth of their capital base in order to provide a growing income stream over time. The Fund’s stated objective is to deliver ‘expected annual income of 2.5% above the S&P/ASX 100 dividend yield over rolling three year periods’. Based on a long-run expected market dividend yield of 4.5%, the Fund’s income objective is equivalent to 7% per annum plus franking credit income (say, a total income return of 8% per annum). This raises an interesting question: What is the maximum level of income which can be produced and sustained by an equity income fund? In other words, what level of income can be paid before the Fund effectively starts paying back clients their own capital? One way of addressing this question is to consider an equivalent concept relating to shares – the dividend payout ratio. Dividend payout ratio =Percentage of earnings paid to shareholders in dividends = Annual dividends/annual net profit = Dividend per share/earnings per share Company directors determine an appropriate dividend payout ratio that seeks to balance shareholders’ desire for both personal income and the reinvestment of profits in the business in order to grow earnings over time. Companies with modest reinvestment requirements are able to pay a greater proportion of earnings as dividends and, therefore, exhibit high dividend payout ratios. Investors should be concerned if a company’s dividend payout ratio consistently exceeds 100%, ie pays dividends which exceed profits over the long term, as this is clearly unsustainable. For listed companies, maintaining a dividend payout ratio above Adviser use only 100% can be achieved by either paying a ‘capital return’ or frequently re-gearing the balance sheet. The most commonly referenced examples of this approach include the former Macquarie or Babcock & Brown listed fund models and highly geared REITs, which fell heavily during the global financial crisis. The income received from shares simply cannot exceed the earnings generated by the firm on a sustainable basis over the long term. The income distribution return of a managed fund can be considered the equivalent concept to the dividends paid by shares of listed companies, while a fund’s annual total return is the equivalent concept to a company’s net profit. Applying the same payout ratio concept, investors should be concerned if a fund’s ‘income payout ratio of total returns’ exceeds 100% over the long term. Given that most funds do not use gearing, a fund’s total return therefore limits the value of income that can be distributed before managers are inefficiently drawing down capital and, in effect, simply returning clients’ money back to them. In short, a fund’s maximum sustainable level of income return is the total return of the fund. Given that share prices reflect a combination of a company’s net profits and an earnings multiple, share prices (and, therefore, equity fund total returns) will have greater variability over time compared to company profits. As a result, the income payout ratio for a fund will be more variable compared to a share’s dividend payout ratio over time. In order to determine the maximum sustainable level of income return for an equity income fund, it is necessary to form a view about the long-term expected total return that the fund will generate. The long-term expected total return for any Australian equities fund consists of*: 1 Long-term Australian equity market accumulation index return, plus 2 Franking credit income, plus 3 Expected alpha, less 4 Management costs * Funds distribute taxable income. Therefore the level of total return and potential distribution is pre-tax. Source: Colonial First State Global Asset Management. Most industry participants consider 8% per annum to be a reasonable guide for the expected long-term return from Australian equities. Therefore, for funds that simply invest in a broad mix of Australian shares and capture this market exposure, this 8% return is the maximum sustainable level of income return that could be distributed over the long-term without simply paying back capital. In order to pay an income return above this 8% per annum level, a fund must focus on the other two elements of total return. The Colonial First State Wholesale Equity Income Fund employs the proven stock selection process of the Australian Equities, Core team that has delivered alpha of 2.84% per annum over the 10 years to June 2010. This alpha is an important source of additional total return and will allow the Colonial First State Wholesale Equity Income Fund to pay a higher level of income return to investors on a sustainable basis over time. Many competitor funds in the equity income space modify their stock selection process to focus on companies that pay a high level of dividends. These funds may, therefore, be unable to realise the alpha benefits that the managers’ underlying stock selection process may provide. Colonial First State Global Asset Management recently undertook research on the benefits of franking credits. The research found that market prices adjust for dividends and a large proportion of franking value. It demonstrated that equity managers should neither chase franking credits in the pursuit of income nor ignore the value of franking credits. Rather, the research suggested equity managers should develop systems that assist in the capture of the franking credits by fulfilling all the ATO requirements for claiming credits. The Australian Equities, Core team has developed its investment process to maximise the capture of franking credits and therefore further improve the income return available to investors. The active approach to income generation via the use of sold equity call options (buy-write strategy) that is utilised by the Colonial First State Wholesale Equity Income Fund and many of its peers seeks to efficiently convert the total return generated from the underlying share investments into a smoother income stream over time. The options market is reasonably efficiently priced. Therefore the expected return on an option will match the expected return on the underlying asset. Evidence that the option positions do not change the long-term expected returns of the equity portfolio is shown by comparing the realised returns of two series: the S&P 500 Total Return Index (SPXT) and the S&P 500 Buy Write Index (BXM). Based on the daily long-term data over the period from 1/1/1990 to 30/06/2010 the average annual return of 9.1% on the Buy Write Index compares closely to the average annual return of 9.3% on the Total Return Index. We have used US data for this comparison as it has a longer term track record but we have seen similar results in the Australian market. This paper has explained why the management of total return should remain a fundamental concept for equity income funds. Calculating the expected long-term total return from the Colonial First State Wholesale Equity Income Fund enables us to return to our original question – what is the maximum level of income which can be produced and sustained by an equity income fund? Equity income return components 12% 10% 10% 10% -1% 8% 8% 2% 1% 6% 4% 2% 0% Long-term Franking Australian equity credit market accumulation income index return Expected alpha Management costs Total equity Maximum income fund sustainable return income return * Stylised concept chart. Past performance is no indication of future performance. The maximum level of sustainable income that can be paid by an equity income fund over time is equivalent to the total return generated after fees. The importance of alpha generation should also be highlighted as an important factor that ensures a higher level of income can be generated over the long term. The stylised chart shows an extreme case whereby all the total return is distributed as income. The Colonial First State Wholesale Equity Income Fund objectives are to simultaneously deliver a consistently high level of income each year and provide conservative capital growth over time by reinvesting some of the surplus total return. This reinvestment seeks to ensure that the actual dollar value of the cashflow generated by the Fund grows over time in order to maintain the purchasing power of the income. About the author About Colonial First State Rudi Minbatiwala is Senior Portfolio Manager in the Australian Equities, Core team. He is responsible for the management of the Enhanced Yield Fund and Equity Income Fund. This role involves analysis of structured equities such as equity derivative strategies and hybrid securities. Colonial First State has been helping Australians with their investment needs since 1988 and now has more than A$90 billion under management globally1. Rudi has been part of the Australian Equities, Core team since January 2000. During that time, his roles have included Portfolio Manager for the index Australian equities portfolios, Senior Quantitative Analyst for the Core active portfolios and Equity Analyst covering the diversified financials sector and small companies. Our wide range of investment management expertise spans Australian and global shares, property, fixed interest, credit, infrastructure and resources. We launched the Colonial First State Wholesale Equity Income Fund in March 2008. Rudi has a Bachelor of Commerce degree (Actuarial Studies) and a Bachelor of Applied Finance from Macquarie University. Rudi is also a CFA charterholder. 1 Colonial First State Investments Limited and its licenced related entities to which it has delegated investment or administrative functions. Want more information? 15797/FS4663/1110 For more information on the Colonial First State Equity Income Fund, contact your local Business Development Manager or call Adviser Services on 13 18 36, 8am to 7pm, Sydney time. This document has been prepared by Colonial First State Investments Limited ABN 98 002 348 352, AFS Licence 232468 (Colonial First State). Colonial First State is a subsidiary of Commonwealth Bank of Australia ABN 48 123 123 124 (‘the Bank’). The Bank and its subsidiaries do not guarantee the performance of Colonial First State’s products or the repayment of capital by Colonial First State. While all care has been taken in the preparation of this document (using sources believed to be reliable and accurate), to the maximum extent permitted by law, no person including Colonial First State or the Bank (or its subsidiaries) accepts responsibility for any loss suffered by any person arising from reliance on this information. This document is general information only does not take into account your individual objectives, financial situation or needs. Adviser use only