Calculation of Variances & Reconciliation of Fixed Overhead Costs

advertisement

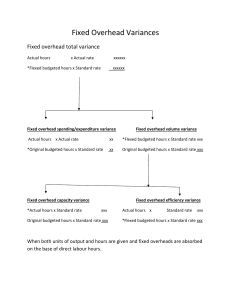

Calculation of Variances & Reconciliation of Fixed Overhead Costs The treatment of fixed overheads in standard costing is not very clearly presented in some text books. This note describes an alternative presentation based on cost reconciliation, which only needs 2 simple formulas and should be easier to remember. The table below starts with the Actual Cost of Fixed Overheads and adds variances to get to the Fixed O/H Absorbed by Volume, which is the overhead absorbed in Standard Costing. It is favourable to absorb more than is spent so this means that favourable variances are positive and unfavourable variances are negative in this table. In the table, different figures for the value of overheads are shown by XXX and variances are shown by xxx. The calculation procedure is in 4 steps as follows: 1. Fill in the two given costs. i.e. Actual Cost / Budgeted Cost of Fixed Overheads. 2. Calculate the overhead absorbed by the actual volume of output. (Check: if the actual volume is different from the budgeted volume, then the overhead absorbed should increase or decrease by the same percentage.) 3. If information on the resource capacity used is available, calculate the expected overhead absorption due to the change in capacity. (Check: if the actual capacity is different from the budgeted capacity, then the overhead absorbed should increase or decrease by the same percentage.) 4. The variances are the missing xxx figures in the vertical sums, and are each calculated by taking the XXX figure above the variance away from the XXX figure below the variance. A B C Actual Cost of Fixed Overheads (step 1) XXX XXX XXX Expenditure Variance (step 4) xxx -----XXX xxx -----XXX - xxx -----XXX - - - - xxx - - - xxx - -----XXX -----XXX xxx -----XXX Budgeted Cost of Fixed Overheads (step 1) Capacity Variance (step 4) Expected Fixed O/H Absorption by Capacity (step 3) (Budgeted Cost x Actual Capacity / Budgeted Capacity) Efficiency Variance (step 4) Volume Variance (step 4) Total Fixed O/H Variance (step 4) Fixed O/H Absorbed by Volume (step 2) (Budgeted Cost x Actual Volume / Budgeted Volume) - The three columns show three separate possible answers, depending on what information is available or wanted. Figures which are not applicable are indicated with a dash. In column A, the calculations for Expenditure, Capacity & Efficiency variances are shown. In column B, the calculations for Expenditure & Volume variances are shown. In column C, the calculation for the Total Fixed O/H variance is shown. With these calculations, it is always essential to correctly identify the output volume (quantity) of the product or service, and the resource capacity which is used to create the product or service if this is also given. Sometimes questions use confusing ways of measuring these, but the proposed method should be reliable provided that Actual & Budgeted Volume are measured in the same units, and Actual & Budgeted Capacity are measured in units that are appropriate to Capacity. Note: The Standard Costing Absorption Rate is Budgeted Cost / Budgeted Volume if needed for other calculations. Note: The order of the reconciliation is reversed in the Osborne Unit 8/9 book, requiring favourable variances to be negative and unfavourable variances to be positive there.