Unit 1 Finance and Accounting

advertisement

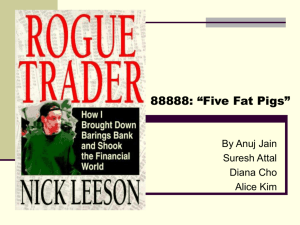

Unit 1 Finance and Accounting Text A Accounting: The Basis for Business Decision Accounting is the information system that measures business activities, processes that information into reports, and communicates the results to decision makers. Accounting is not the same as bookkeeping. Bookkeeping is a procedure in accounting, just as arithmetic is a procedure in mathematics. Accounting is often called “the language of business.” The better you understand this language, the better your business decisions will be, and the better you can manage the financial aspects of living. Personal financial planning, education expenses, loans, car payments, 1income taxes, and investments are based on the information system that we call accounting. Today people use computers to do detailed bookkeeping — in households, businesses, and organizations of all types. The process starts and ends with people making decisions. Virtually all businesses and most individuals keep accounting records to aid in making decisions. Individuals People such as you use accounting information to manage bank accounts, evaluate job prospects, make investments, and decide whether to rent or buy a house. Businesses Business managers use accounting information to set goals for their organizations, to evaluate progress toward those goals, and to take corrective action if necessary. Decisions based on accounting information may include which building to purchase, how much merchandise to keep on hand, and how much cash to borrow. Investors Investors provide the money a business needs to begin operations, To decide whether to invest in a company, potential investors evaluate what income they can expect from their investment. This means analyzing the financial statements of the business and keeping up with developments in the business press— for example, 2The Wall Street Journal and Business Week. Creditors Before making a loan, creditors (lenders) such as banks determine the borrower’s ability to meet 3scheduled payments. This evaluation includes a report on the borrower’s financial position and a prediction for future operations, both of which are based on accounting information. To borrow from a bank before striking it rich, 4Harold Nix probably had to document his income and financial position. Government 5Regulatory Agencies Most organizations face government regulation. For example, 6the Securities and Exchange Commission (SEC), a federal agency, requires businesses to disclose certain financial information to the investing public. Taxing Authorities Local, state, and federal governments levy taxes on individuals and businesses. Income tax is figured using accounting information. 7Businesses determine the sales tax they owe from accounting records that show how much they have sold. Nonprofit organizations Nonprofit organizations— such as churches, hospitals, government agencies, and colleges — use accounting information in much the same way that profit-oriented businesses do. Financial Accounting and Management Accounting Users of accounting information may be categorized as external users or internal users. This distinction allows us to classify accounting into two fields — financial accounting and management accounting. Financial accounting focuses on information for people outside the firm. Creditors and outside investors, for example, are not part of the day-to-day management of the company. Government agencies and the general public are external users of a firm’s accounting information. Management accounting focuses on information for internal decision makers, such as top executives, department heads, college deans, and hospital administrators. Text B Internal Control On February 26, 1995, one fresh-faced 28-year-old trader 1brought a venerable 233-year-old British bank to its knees. Nick Leeson, a trader for 2Barings Bank, had bought $27 billion worth of securities on Japan’s Nikkei stock market. When the Nikkei plunged, Barings lost $27 billion and collapsed. All fingers pointed to Leeson. How could a conservative bank allow this to happen? It soon became clear that nobody was supervising Leeson’s trades. Leeson worked in Barings’ Singapore office from 1992 to the time of the collapse. Barings fell because it lacked 3internal controls. Leeson was allowed to execute 4cross trades, transactions in which he acted as both buyer and seller. Leeson’s transactions were not 5at “arms’ length”, where the seller tries to get the highest price and the buyer tries to pay the lowest price. Without arms’ length trading, the amount of the transaction could be anything Leeson entered into the system. Amazingly, the bank did not require Leeson to give up his job as head of selling when he became head of buying. From the start, Leeson lost money in Singapore, but he hid the losses— $296 million in 1994 alone. What did Leeson’s bosses think of his performance that year? They thought he made a $46 million profit for the bank, and proposed paying him a bonus of $272,000. Months before the collapse, Barings knew of Leeson’s dual role. Internal auditors warned of “significant general risk” because Leeson controlled both the buying and the selling sides of transactions. But Baring’s higher-ups viewed Leeson as a golden boy, and they ignored the audit report — with disastrous consequences. The above case shows how important the internal control is. A key responsibility of managers is to control operations. Owners and top managers set a company’s goals, managers lead the way, and employees carry out the plan. Internal control is the organizational plan and all the related measures that an entity adopts to 1. Safeguard the assets the business uses in its operations, 2. Encourage adherence to company policies, 3. Promote operational efficiency (obtain the best outcome at the lowest cost), and 4. Ensure accurate and reliable accounting records. Internal controls are most effective when employees at all levels adopt the organization’s goals and ethical standards. Top managers need to communicate these goals and standards to workers. 6Lee Iacocca, former president of 7Chrysler Corporation, instilled goals in Chrysler employees by spending time with assembly-line workers. (Japanese firms pioneered this style of 8participative management.) The result? Defects decreased, and Chrysler products became more competitive. An Effective Internal Control System Whether the business is 9First Fidelity, Target Corporation, or a local department store, and effective system of internal controls has the following characteristics. Competent, Reliable, and Ethical Personnel Employees should be competent, reliable and ethical. Paying top salaries to attract top-quality employees, training them to do their job well, and supervising their work all help a company build a competent staff. 10Within this organization, the controller may be responsible for approving invoices (bills) for payment, and the treasurer may actually sign the checks. Working under the controller, one accountant may be responsible for payroll, another accountant for 11depreciation. All duties should be clearly defined and assigned to individuals who bear responsibility for carrying them out. Assignment of Responsibilities In a business with a good internal control system, no important duty is overlooked. Each employee is assigned certain responsibilities. For example, in a certain company, there is a vice president of finance and accounting. Two other officers, the treasurer and the controller report to that vice president. The treasurer is responsible for cash management. The controller is the chief accounting officer. Text C Effective Accounting Information Systems Every organization needs an accounting system. Decision makers need information. The more important the decision, the greater the need for information. An accounting information system is the combination of personnel, records, and procedures that a business uses to provide financial data. It consists of two basic components: a general journal and a general ledger. Every accounting system has these components, but this simple system can efficiently handle lonely a few transactions per period. Businesses cope with heavy transaction loads in two ways: computerization and specialization. We computerize to do the accounting faster and more reliable. 1Specialization comes within the similar transactions to speed the process. Computerized accounting systems have replaced manual systems in many organizations — even in small businesses such as your neighborhood pharmacy. 2Inputs represent data from source documents, such as sales receipts, bank deposit slips, fax orders and other telecommunications inputs are usually grouped by type. For example, a firm would enter cash-sale transactions separately from 3credit sales and purchase transactions. Outputs are the reports used for decision making, including the financial statements (income statement, 4balance sheet). Business owners are making better decisions— and prospering — because of the reports produced by their accounting system. Good personnel are critical to the success of any operation. Employees must be both competent and honest. And several design features can make the accounting system run more efficiently. A good system— whether computerized or manual — includes control, compatibility, flexibility, and a favorable cost/benefit relationship. Managers need control over operations. Internal controls are the methods and procedures used to authorize transactions and safeguard assets. For example, in companies such as Coca-Cola, 4America Online, and 5Kinko’s, managers control cash disbursements to avoid theft through unauthorized payments. 6Visa, Mastercard, and Discover keep records of their accounts receivable to ensure that they receive collections on time. A compatible system is one that works smoothly with the business’s operations, personnel, and organizational structure. An example is Bank of America, which is organized as a network of branch offices. Bank of America’s top managers want to know revenues in each region where the bank does business. They also want to analyze loans in different geographic regions. If revenues in California are lagging, managers can concentrate their efforts in that state. They may relocate some branch offices or hire new personnel. Organizations evolve. They develop new products, sell off unprofitable operations and acquire new ones, and adjust employee pay scales. Changes in the business often call for changes in the accounting system. A well-designed system is flexible if it accommodates changes without a complete overhaul. Achieving control, compatibility, and flexibility costs money. Managers strive for a system that offers maximum benefits at a minimum cost — that is, a favorable cost/benefit relationship. Most small companies use off-the shelf computerized accounting packages, and the very smallest businesses might not computerize at all. But large companies, such as the brokerage firm Edward Jones, have specialized needs for information. For them, custom programming is a must. The benefits — in terms of information tailored to the company’s needs — far outweigh the costs. The result? Better decisions.