Oracle Confidential

For use by Oracle employees and authorized partner only. Do not distribute to third parties.

SAP All-In-One Competitive Profile

Harald Freudendahl

January 30, 2006

SAP AG All-In-One Corporate Statement

All-In-One is SAP’s midmarket solution offering of to companies or divisions of larger corporations with revenue

between $200 Million and $ 1 Billion. All-In-One is currently based on the SAP R/3 4.6 version. SAP has announced

an update for 2006 that is based on mySAP ERP.

The All-In-One business suite offers the typical ERP-functionality of Financials, Cost Mgmt., Sales and Distribution,

MRP II based manufacturing and Reporting. vSAP offers pre-configured vertical and pre-configured country versions to

accelerate the implementations and reduce costs. The All-In-One solutions are sold via VAR channels as well as directly

via SAP midmarket sales reps in the higher end of the market.

This document covers the following:

Overview

Corporate History & Statistics

Senior Management

Financial Viability

Business & Strategy

Target Markets

Strategies

Positioning

Customers

Partners

Strengths & Limitations

Technology

Product Families

Architecture

Platforms

Scalability

3rd Party Interoperability

Other

Analyst Reports

(C) 2005, Oracle. All rights reserved. This document is provided for information purposes only, and the contents

hereof are subject to change without notice. This document is not warranted to be error-free, nor is it subject to any

other warranties or conditions, whether expressed orally or implied in law, including implied warranties and

conditions of merchantability or fitness for a particular purpose. We specifically disclaim any liability with respect

to this document, and no contractual obligations are formed either directly or indirectly by this document.

Page 1 of 7

Oracle Confidential

For use by Oracle employees and authorized partner only. Do not distribute to third parties.

Overview

URL

Corporate

Statistics &

History

http://www.sap.com/solutions/sme/allinone/index.epx

All-In-One is SAP’s product offering aimed at the middle of the SMB market. The low-end of

the SMB market – below $200M revenue – is covered by BusinessOne; the high end from $ 1.0

Billion to $ 1.5 Billion revenue companies is covered by mySAP ERP. Because SAP AG serves

primarily large Enterprise customers, only a fraction of its business is SMB. Click here for the

general corporate overview.

Corporate SMB facts:

Senior

Management

Organizational

SMB Structure

10.4 Billion US$ revenue with 30% SMB (< 1 Billion revenue segment)

35,000 employees – number of dedicated H/C to SMB not published

50 country versions of All-In-One as of 10/2005

730 VAR partners for All-In-One as of 10/2005

7,100 All-In-One customers as of 10/2005

SAP announced for 2006 a mySAP ERP based version on Netweaver2004

SAP launched many unsuccessful SMB initiatives over the last 14 years

Leo Apotheker heads-up worldwide sales, field marketing and professional services. The

senior management for the SMB division and all country GM’s report into Leo.

Donna Troy, SVP SMB Channels, joined the team in Q1-2004 to beef-up SAP’s floundering

SMB initiative. Putting her SMB channel expertise to work, she re-designed the VAR program

into PartnerEdge and hired her management team. Troy runs an overlay organization and the

Field Sales organization reports to the country GM’s.

Rodney Seligman is the SVP at SAP America for what they call the Territory Sales

Organization. It combines all SMB-sales, not just the Business One VAR-channel. This new

structure was created in July 2005.

Andreas Naunin leads the German distribution channel and reports to the German GM

Hoechbauer (ex PSFT GM Germany). Naunin succeeds M.Schmitt as of 01.01.2006 due to

mediocre results. The German distribution channel and partner solution offering will be

expanded to better address the SMB space and to increase market coverage.

For other non-SMB related players see the SAP AG OrgChart here

Financial

Viability and

M&A activity

The four Enterprise software heavyweights are Oracle, IBM, Microsoft and SAP. SAP

is the only non US-based company and is financially stable and profitable.

It is unlikely that SAP will be acquired, although, SAP and MSFT conducted a

comprehensive M&A exercise in Q4-2003. Following those discussions SAP decided to

stay independent and the two companies will collaborate more.

In the past SAP has not acquired software companies to “buy marketshare” or to buy

channel expertise. SAP believes in building from inside the organization. However,

SAP does acquire smaller companies/boutique software companies to round out it’s

business solution offering.

For the latest Financial Facts & Figures click here.

Page 2 of 7

Oracle Confidential

For use by Oracle employees and authorized partner only. Do not distribute to third parties.

Target Markets

All-In-One

Business & Strategy

Customer size:

SAP keeps changing the SMB-target definitions over the last three years in order to

increase the “SMB revenue” they show. Previously their SMB-space covered <50

Million to 700 Million. Now they expand it to up to $ 1.5 Billion sized customers. The

Route-to-Market slide published in 11/2005 to financial analysts does not capture all

details.

The three tiered customer sizes SAP has drawn in the SMB-space positions All-In-One

in the middle of their SMB solution offering. See the chart below for the Route-toMarkets (RTM). As a result, All-In-One targets companies with $200 Million to $1.0

Billion annual revenue and similarly sized branches and divisions of global and national

enterprises where other SAP products are installed (RTM3 – green shaded area).

Industries:

SAP requires VAR-partners to develop and distribute at least one software-add-on. By forcing

VAR-partners to comply, SAP claims to offer 550 micro-vertical and country-versions – virtually

covering all niches. In January of ’06, SAP announced an additional 39 partner solutions for AllIn-One.

Geographies:

All-In-One is marketed worldwide with special focus on emerging markets in India and China.

SAP’s midmarket presence in EMEA is sizable. The VAR-channel and implementation partnernetwork in North America is lacking bandwidth and will be expanded on 2006 to increase

geographic coverage.

Strategies

SAP’s stated SMB goals as stated by Leo Apothekar are as follows:

1. To grow its SMB business faster than the industry average.

2. To double it’s installed base of SMB/Midmarket customers (SAP aims for 20,000

midmarket customers in 2006).

3. To build the infrastructure and programs to become the most partner-friendly software

vendor in the industry.

There are two strategic questions that are key to achieving these goals: How to reach and expand

the SMB market and How to expand the product solution set with limited direct SAP R&D

investment.

SAP’s so-called Route-To-Market is shown in this graph, which tries to solve the channel

conflicts between direct and indirect sales channels and territory or competency assignments of

multiple VAR and software partners for the same space.

Page 3 of 7

Oracle Confidential

For use by Oracle employees and authorized partner only. Do not distribute to third parties.

Target companies are between $10 Million and $1.5 B in SAP America and EMEA. In emerging

markets SAP has a lower target. The SAP SMB-market solutions consist of 3 different solution

sets and a hybrid “direct vs. indirect” model to reach the different market segments.

Product Strategy expansion

Since early 2002, SAP has required every VAR-partner in the partner-contract to develop, expand

and maintain strong micro-vertical solution sets. By 2006 SAP will refocus on the quality of the

software solutions and will weed out weaker offerings. Those solutions that survive the quality

assessment will gain access to the marketing and sales channel of all VAR’s. Currently SAP is

undergoing a major revamp of the 550 add-on solutions offered and intends to increase the

quality of the solutions, not the quantity.

PartnerEdge Channel Partner program

SAP relaunched its VAR SMB prorgam to better reward the commitment of smaller partners.

SAP does not only reward the large VARs which drive sales volume and revenue, but also VAR

who invest into staff education, referenceable customer implementations and quality best

business practices. By collecting credits the VAR gets increasing benefits and is promoted from

Associate level to silver and gold level.

Marketing

messages AllIn-One

Positioning

SAP uses a series of consistent messages to promote the benefits of All-In-One:

“The power to drive value and to increase revenue for SMB enterprises”

“Pre-configured solution sets, pre-packaged industry versions “

“Leverages over 30 years of best practices expertise – enhanced for SMB”.

“Cost-effective turnkey implementation.”

“Affordable: Defined Scope. Defined Price. Defined Timeframe.”

The value play is now also at work in SAP’s marketing messaging in the SMB-space. The

widespread concern of costly, timely implementations is countered with the messages above

and culminates in the marketing message: Accelerating the implementation process saves time

and money while minimizing risk and disruption to business.

Page 4 of 7

Oracle Confidential

For use by Oracle employees and authorized partner only. Do not distribute to third parties.

Customers

Watch for these

companies to be

references

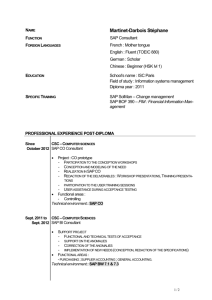

SAP claims ~ 7,100 All-In-One customers as of 10/2005. SAP claims a run rate of adding 20

customers per day worldwide in the SMB-space. The following customers are known references.

Their selection appears to be random by geography, industry and company-size. Additional

customer success stories can be viewed on SAP’s web site.

Partial Customer List:

Anthro Corp.

Brezelbckerei Ditsch

Bookham Technology

Chordus

Cosmtique Active

Crestron electronics

Dairy Industries

Daryl Industries

DITAN Distribution

Eclipse Aviation

ECompany Store

Edrington Group

Endo Pharmaceuticals

Engelhard Arzniemittel

Fastbolt Distributors

FHECOR Ingenieros Consultores

Fredericks Dairies

Greenheck

Hand Held Products Inc.

Hawaiian Tropic

Holhl & Co.

Indigo Lighthouse

Macaw Soft Drinks

Microcast

Mitsui Chemicals

Muntons

Nieder-Ramstdter Diakonie

Oxford Chemicals

Schloss Raggendorf Sekt & Weinhandel

Schumacher Elevator

Southern Pump & Tank Co.

Sparkice

SRB Group

Tallard Technologies

TriVirix Int’nat’l

Wictor SpA

Note: ca. 40 customer names from 04/2005

Sales

Channels &

Partners

SAP sells All-In-One through channel partners and direct in the higher-end of the SMB-space.

There are currently ~730 Business One partners worldwide in 50 countries. India was launched

in 01/2006. Some are traditional SAP implementation partners with an All-In-One practice, and

others are VAR’s in the SMB space who are adding All-In-One to their portfolio of JD Edwards

and Microsoft Dynamics/ MBS offerings.

Issue: Existing loyal R/3 clients complain to SAP AG that the license price per user for the AllIn-One suite is only 25% of the licenses they were charged in the 1993 – 2002 timeframe and that

their annual maintenance fees are still based on these high prices. (Source: DSAG German user

group 10/2005 survey and interview with Chairman).

For a look at the complete SAP All-In-One directory click here. Please choose the country and

the category you want to locate an All-In-One partner for.

Other Partners

SAP has enlisted software partners to address the different micro-vertical and country specific

requirements. As of 10/2005 there are 550 software add-on solutions.

Strengths

The All-In-One solution has several key competitive strengths:

Mature business application suite built on the old and proven SAP R/3 4.6 release

By investing in pre-configured solution sets and a so-called building block structure,

SAP may indeed achieve more efficient implementations

SAP achieves coverage of geographies by adding the VAR channel to its existing highend enterprise sales presence

The All-In-One solution benefits from SAP’s R&D investment into 50 country versions

The micro-verticals are covered by 550 partner add-on solutions

SAP offers a wide implementation partner network and expands its reach with the

benefits of the PartnerEdge Channel program

Page 5 of 7

Oracle Confidential

For use by Oracle employees and authorized partner only. Do not distribute to third parties.

Limitations and

Weaknesses

Product

Families

There are several inherent weaknesses with the All-In-One offering:

SAP’s track record in the low-end SMB space is poor

The market perception that SAP solutions are complex, costly and time-consuming to

implement hurts SAP

SAP does not know how to do business down-market and, according to disenchanted

VAR-partners, is in true ramp-up mode.

Until the sales volume can sustain the infrastructure costs, the low-end market is

economically challenging for SAP

SAP faces challenges from it’s old R/3 customers who complain about the four-times

higher license costs they paid between 1993 and 2002 vs. the All-In-One price points

today. Their annual 17 % maintenance fees are also still based on these four times

higher net-software values.

The All-In-One product is based on proprietary SAP-technology (e.g. ABAP

programming language) and customers who implement today are forced into the 12 year

old client/server baggage of the multinational enterprise functionality that is buried

under the covers

The major burden for cost effective turnkey implementations is on the SAP

implementation partners. Only time will tell if they are able to succeed where SAP

failed in the past.

Technology

SAP AG offers Business One as the entry-level solution for SMB. This is a standalone solution

based on MSFT platform technology. SAP so far does not offer any upgrade to their other SMB

solution, All-In-One. For so-called high-end SMB they offer the All-In-One solution which as a

pre-configured R/3 edition. This runs on the SAP Netweaver platform. The announced plan for

2006 is a version of All-In-One, which better integrates with Netweaver.

In the Enterprise Business SAP offers mySAP ERP 2004/2005, the mySAP BusinessSuite and

for existing customers R/3 Enterprise. Please refer to the extensive coverage of the SAP

coverage on the CI-website.

Architecture

3-tier client-server architecture from 1992

All major operating system and database combinations are supported

Low requirements for scalability due to low-end of Business applications market-space

Runs on inexpensive commodity hardware

Platforms

Operating systems: Microsoft 2000, XP, Server2003 and the like

Databases: Microsoft SQL

Scalability

SAP addresses the scalability more in terms of site support:

Ability to support multi-plant

Ability to support larger enterprises (more importantly for SMB, what size org. can the

software support)

3rd Party

Interoperability

All-In-One integrates with all R/3 based partner add-on solutions via the SAP-proprietary BAPIinterfaces. Complexity inclusive.

Other

Analyst

Reports

Gartner: SAP Capable of challenging SMB market leaders? ID COM-20-1751 June 2003

Gartner: SAP partners with HP to target SMB in EMEA ID M-18-5719

IDC: SAP launches PartnerEdge blueprint Doc.No. #33454 May 2005

IDC: SAP SMB partner update – Gaining critical mass Doc.No. #SN52M June 2005

Number: E-22-3973

Number: E-22-3973

Page 6 of 7

Oracle Confidential

For use by Oracle employees and authorized partner only. Do not distribute to third parties.

Contact Harald Freudendahl if you have any questions regarding SAP in SMB or contact Charles Homs as the

SAP Lead on the Competitive Intelligence team.

Page 7 of 7