Chp 1 Notes

advertisement

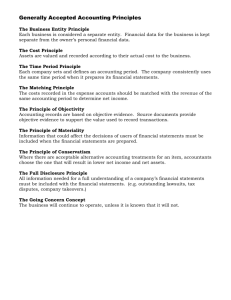

Chapter 1 Year 12 Accounting – Unit 3 Chapter 1 Study/Summary Notes Accounting should be seen as an overall management strategy. Financial Information helps a business owner answer such things as Is profit improving/declining? (Profitablilty) Is the owner earning sufficient return on the investment in the business? Could he earn a better return elsewhere, eg on the sharemarket? (Return on Investment) How much cash can the owner withdraw from the business? (Drawings) Has the business enough liquid funds to continue trading? (Liquidity) Can the business meet its debt repayments? (Liabilities) Is the business financially stable? (Stability) Are credit customers paying on time? (Debtor Control) What is the cost of the business’s assets and how are they financed? (Balance Sheet) Q: What is the major reason why small businesses collapse? A: Lack of available, meaningful financial information. Well informed business=better chance of success. Information is powerful. The Accounting Process Data Collected Data Sorted Data Classified Data Reported Data Analysed Users of Financial Information Accounting must meet the needs of the individual user and must be flexible enough to satisfy a variety of purposes. The main users are: 1) Owner/Manager – interested in profit, liquidity, stability, sales, growth, budgets, stock management, debtors, creditors, rates of return Chapter 1 2) Prospective Owners – Interested in budgets, future earnings, predicted returns, stability, prospects of growth 3) Banks/Lenders – Interested in liquidity, stability, prospects of growth 4) Suppliers of goods or materials – Interested in credit rating, reliability, stability 5) Government Departments – taxation department, Australian Bureau of Statistics, Small Businesses of Victoria 6) Employers/Unions – Interested in stability of employment, profits, the likelihood of wage increases 7) Customers – Interested in pricing, credit facilities, future trading opportunities Role of Accountants Computer technology has resulted in more streamlined processes therefore accountants have more input into the interpretation of financial results as part of a management team. Types of Accountants 1. Public Accountants – work in business for themselves. They serve the public by providing expert advice on financial matters. Have areas of expertise e.g taxation, finance, computerized accounting Usually members of a professional accounting body (ICAA or CPA Aust) A valuable resource because many small business owners have little/no training 2. Private Accountants – employed by one particular business as a private employee Usually work for large scale organizations Specialize in various areas Choose to work for one employer rather than in a public practice 3. Government Accountants – employed by Government departments and authorities on federal, state and local levels. Deal with government receipts, payments and budgets 4. Academic Accountants – employed in tertiary education or in research Educate future accountants Develop accounting standards Accounting Standards Definition: Accounting Standards are enforceable by law and set out the generally accepted accounting principles, which all members of the professional bodies are obliged to follow. Aim: to ensure that reports are prepared in an acceptable form using approved accounting techniques. Statement of Accounting Concepts (SACS) Definition: Statements designed to complement accounting standards and to provide interpretation of accounting standards Aim: to achieve consistent methods in accounting applications across the whole accounting profession Chapter 1 SAC 1: Definition of a Reporting Entity SAC 2 : Objective of General Purpose Financial Reporting (GPFR) – Identifies users of GPFR, needs of users of GPFR and the information GPFR should provide e.g balance sheets and P/L Statements Objective: To provide relevant and reliable information to users of general purpose financial reports to allow them to make financial decisions. SAC 2 specifies that accounting information must have the following qualities; (C.U.R.R) Qualitative Characteristics of General Purpose Financial Reporting Comparability: 1) Users of reports must be able to compare results from different periods in order to report on changes in a firm’s performance over consecutive reporting periods. Accounting methods must be applied consistently from one period to the next. 2) Users of accounting must be able to make comparisons between the performances of different business. Understandability: Reports must be prepared in such a way that general users are able to comprehend their meaning. Eg. Use descriptive heading and explanatory notes Relevance: Accounting information must be based on information that is relevant to the entity. This supports the entity principal that states personal transactions are omitted. The test of relevance is know as materiality. Information is of material importance if its omission could influence the decision of the user of accounting. Eg reporting cents is not material therefore it is not relevant. Reliability: Information must be reliable (trustworthy) because it is used to make many financial decisions. Information is reliable if it can be verified against business documents. Information must not be subject to personal opinion or bias. SAC 2 contains the definitions of several key elements of accounting such as Assets - resources controlled by the entity as a result of past events and from which future economic benefits are expected to flow to the entity. Liablilites – are present obligations of the entity arising from past events of which there is an expected outflow of resources from the entity involving economic benefits. Owners Equity – is the residual interest in the assets of the entity after deduction of its liabilities Chapter 1 Assets = Liabilites + Owners Equity Owners Equity= Assets – Liabilites Revenues – Are increases in economic benefits during the reporting period in the form of inflows or improvement of assets or decreases in liability that result in increases in equity. Expenses – are decreases in economic benefits during the reporting period in the form of outflows or depletions of assets or incurrences of liabilities that result in decreases in equity. Accounting Principles Entity Principle – personal transactions of the business should be kept separate from those of the owner. The business is always viewed as a separate entity. Refers to SAC 2 Qualitative Characteristic of GPFR – Relevance. Historical Cost Principle – all transactions are recorded at their original cost price and therefore this method relies on evidence of documents such as invoices and receipts. Refers to SAC 2 Qualitative Characteristic of GPFR – Reliability Going Concern Principle – assumes that a business will go on forever for an indefinite period. Accountants can report long term assets in the balance sheet otherwise they would have to be written off as expenses in their first year of purchase. Reporting Period Principle – the continuous life of a business is divided into equal periods of time for the purpose of calculating profit and loss and enabling comparison of results. Refers to SAC 2 Qualitative Characteristic – Comparability Monetary Principle – the measurement unit used in reports is the currency of the country where the report is being prepared. Events must be able to be stated in monetary terms for it to be included in an accounting report Conservatism Principle – Reports should be prepared cautiously and accountants should err on the side of safety. Expected losses would be allowed however gains would only be recognised if certain to occur. Consistency Principle – Accounting methods must be applied consistently from one period to the next to enable comparisons of performance over time. This supports the SAC 2 Qualitative Characteristic Of Comparability. In Brief Relevance is supported by the accounting Entity Principle and the Reporting Period Principle Comparability is supported by the Consistency Principle Chapter 1