Chapter 16: Accounting for Tax Losses

advertisement

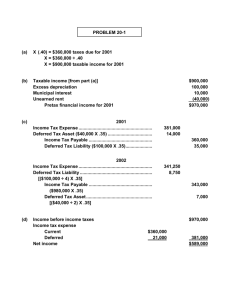

Chapter 16: Accounting for Tax Losses Assignment 16-9 Requirement 1 Taxable income: Accounting income Permanent difference: Golf club dues Accounting income subject to tax Temporary difference: Depreciation CCA Taxable income Tax rate Income tax payable 20x3 $ 10,000 20x4 $ 15,000 20x5 ($40,000) 20x6 $ 10,000 3,000 4,000 3,000 4,000 13,000 19,000 (37,000) 14,000 6,000 (3,000) 16,000 × 20% $ 3,200 6,000 (6,000) 19,000 × 20% $ 3,800 6,000 (12,000) (43,000) × 30% n/a* 6,000 (10,000) 10,000 × 35% $ 3,500 * Part of loss is carried back at rate of 20%; current year rate is not applicable. See Requirement 2 Requirement 2 Taxable Amounts Tax loss ............................................................................ $(43,000) Carryback ($16,000 + $19,000) ....................................... 35,000 Carryforward .................................................................... $ (8,000) Benefit $7,000 (20%) The $8,000 loss carryforward would be recorded at a rate of 30% ($2,400) if recorded in 20x5. This is the enacted tax rate in 20x5. The 20x6 rate cannot be used until enacted. This data is used further in Assignment 16-10. Assignment 16-10 Note: Students should have completed Assignment 16-9 prior to this assignment. Income tax receivable (1)............................................................. Deferred income tax asset – LCF (2) ........................................... Deferred income tax – long term (3)...................................... Income tax expense (4) .......................................................... 7,000 2,400 1,500 7,900 (1) Taxable income, 20x3 & 20x4: (see solution to Assignment 16–9) $16,000 + $19,000 = $35,000. Amount paid, $3,200 + $3,800 = $7,000 (2) Taxable loss in 20x5 (see solution to Assignment 16-9) ............................ $43,000 Loss carryback to 20x3 and 20x4 ($16,000 + $19,000) ............................. (35,000) Tax loss carryforward ................................................................................. 8,000 Benefit of tax loss carryforward (@ 30%) .................................................. $ 2,400 (3) (in 000’s) Tax Basis Accountin g Basis Temporary Difference DIT Liability $(3) @ 30% $(.9) 20x5 Capital assets (a) (b) (c) (4) $54 (a) $57 (b) Opening Balance $.6 (c) Adjustment ($1.5) $75,000 – ($3,000 + $6,000 + $12,000) $75,000 – ($6,000 × 3) [($75,000 – $9,000) – ($75,000 – $12,000)] × .20 $7,000 + $2,400 – $1,500 In order to record the benefit of the tax loss carryforward in 20x5, the company must be able to establish that its realization during the carryforward period is more likely than not. This is defined as a probability of more than 50%. Assignment 16-20 Schedule of Accounting and Taxable Income (amounts in thousands) 20x5 Accounting income (loss) Less: non-taxable dividends Temporary differences: Warranty expense Warranty claims paid Depreciation expense CCA Taxable income $ 20x6 0 0 0 60 (60) 600 (600) $ 0 20x7 $ (980) (20) (1,000) $ 0 (20) (20) 120 (80) 600 0 $ (360) 160 (200) 600 (500) $ 40 20x8 20x9 $2,000 0 2,000 $4,000 0 4,000 200 (90) 600 (450) $2,260 300 (75) 600 (400) $4,425 Schedule of Temporary Differences (amounts in thousands) Tax basis 20x5–40% Capital assets Warranty 20x6–40% Capital assets Warranty 20x7–40% Capital assets Warranty 20x8–45% Capital assets Warranty 20x9–45% Capital assets Warranty $5,600 0 Accounting basis $7,600 0 Temporary difference Deferred income tax Opening balance $(2,000) 0 $(800) 0 $(800) 0 $0 0 Adjustment 5,600 0 7,000 (40) (1,400) 40 (560) 16 (800) 0 240 16 5,100 0 6,400 0 (1,300) 0 (520) 0 (560) 16 40 (16) 4,650 0 5,800 (110) (1,150) 110 (517.5) 49.5 (520) 0 4,250 0 5,200 (335) (950) 335 (427.5) 150.75 (517.5) 49.5 2.5 49.5 90 101.25 Journal Entries (amounts in thousands): 20x6 Entry Deferred income tax—capital assets ....................................... 240,000 Deferred income tax—warranty ............................................. 16,000 Deferred income tax asset—LCF ($360 x .40) ....................... 144,000 Income tax expense (recovery) ......................................... 400,000 20x7 Entries Deferred income tax—capital assets ....................................... 40,000 Deferred income tax—warranty ....................................... 16,000 Income tax payable ($40 x .4)........................................... 16,000 Income tax expense (recovery) ......................................... 8,000 Income tax payable ................................................................. 16,000 Deferred income tax asset—LCF...................................... 16,000 Gross LCF now $360,000 – $40,000 = $320,000; recorded at 40%, or $128,000 20x8 Entries Income tax expense ................................................................. 965,000 Deferred income tax —capital assets ...................................... 2,500 Deferred income tax —warranty ............................................ 49,500 Income tax payable ($2,260 × .45) ................................... 1,017,000 Income tax payable ($320 × .45) ............................................ 144,000 Deferred income tax asset—LCF ($144 – $16) ................ 128,000 Income tax expense ($320 × (.45 – .40)) .......................... 16,000 20x9 Entry Income tax expense ................................................................. 1,800,000 Deferred income tax—warranty ............................................. 101,250 Deferred income tax—capital assets ....................................... 90,000 Income tax payable ($4,425 × .45) ................................... 1,991,250 Assignment 16-27 Carryback Of the $220,000 tax loss, $120,000 can be carried back to the preceding three years. The carryback will result in CTC’s realizing a full refund of taxes paid in 20x1, 20x2, and 20x3. The total refund will be $45,600. Carryforward The remaining $100,000 of the 20x4 tax loss can be carried forward and applied against taxable income in the next 20 years. Since management believes that the probability of realizing the future tax benefits is greater than 50%, the deferred income tax benefit should be recognized in the year of the loss, 20x4. The 20x5 enacted rate of 36% can be used. A deferred income tax asset of $36,000 will be recognized. Temporary differences 20x3 – 40% Capital assets Pensions Temporary Difference $95,000* 55,000* deferred deferred Ending Balance $38,000* 22,000* $60,000 cr. cr. cr. $30,600 30,600 $61,200 cr. cr. cr. 20x4 – 36% Capital assets Pensions $85,000** deferred 85,000** deferred * given ** ($95,000 – $10,000); ($55,000 – $30,000 + $60,000) Journal entry to record income tax: Income tax receivable ............................................................ Deferred income tax—LCF ................................................... Income tax expense .......................................................... Deferred income tax—long term ($61,200 – $60,000).... 45,600 36,000 80,400 1,200 Lower portion of income statement Income (loss) from operations before income tax ........................................ Income tax (recovery) .................................................................................... Net income (loss) ........................................................................................... ($200,000) 80,400 ($119,600)