ACCOUNTING TERMS

advertisement

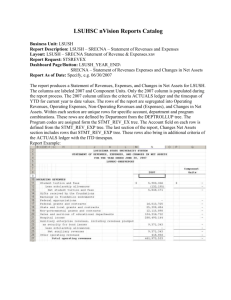

ACCOUNTING TERMS 1. Food Cost Calculation : Opening Stock + Purchases – Closing Stock 2. Individual Menu Item Cost (variable %): Portion Cost/Priced Menu Item x 100 3. Food Cost Budget: Food Cost/Sales Budget x 100 4. Setting the selling price: Portion Cost/Food Cost target % x 100 5. Variance Report: Highlights deviations from budget 6. Receivable Report: Monies owed by customers/suppliers to business 7. Merchant Summaries: Monies the credit card companies (merchant cards) we the business for a given period 8. Source document: Record of occurrence of any business transaction e.g. Purchase orders, Invoices, Credit notes, Restaurant Dockets, guest room accounts 9. Transaction reports: Listing of all transactions within a general ledger code or group of codes 10. Transaction Exemption Report: Done by banks when an amount of 10k or more is deposited by business – report sent to Transaction Reports and Analysis centre 11. Bank Reconciliation statement (BRS) Reconciles the businesses cash and bank balances to that of your bank 12. T Account: Revenues on one side and expenses on the other 13. Running Balance Account: Daily tracking of invoices and sales – used by small businesses 14. Double Entry Book Keeping: Each transaction has two sides – Dr (debit) and a Cr (credit) – E.g. Sale to a customer on 30 days credit will be CrSales Revenue and Dr – Accounts Receivable 15. Credit Card Statements: Lists all transactions for a credit card 16. Account Summary/Balance: Summary of a particular account e.g. Bank, merchant etc 17. Invoice: Docket/Payment details that are due to be paid by business or to the business – details? 18. Business Activity Statement (BAS): Business GST (Goods and Services Tax) tax collection summary and tax paid summary – done monthly or quarterly. Most businesses have GST computation included in transactions that automatically calculate it. 19. PAYG: Pay As You Go – tax the business is expected to owe from the profits at end of financial year. 20. Cashflow Report: Cash movement report – in and out of business/bank – critical part of business as this determines actual cash available to pay the obligations – updated weekly or sometimes daily in businesses, 21. Sales Report: Produced by each revenue earning department within the business. E.g. Restaurant, Golf, Rooms etc – used to compare actual to budget. 22. Stock Report: Shows closing stock levels at end of period. The intention is keep inventory as low as possible using JIT/Par levels etc 23. Wastage Report: Shows how much stock is wasted each period e.g. wines, juices, food etc – critical for business work in conjunction with Stock Report – manage yield – 50ltr Keg 24. Purchase Summary Report: Summary of all purchases over a period – helps procurement to set bulk purchasing deals. 25. Labour /Wages report: Labour or wages spent in each department – salary vs. wages – compared to budget and to industry bench marks 26. Expenditure Reports: Labour (On costs) and non labour (administrative expensesstationary, selling expenses - advertising, finance expenses- interest paid 27. Budget Reports: Compares entire budget to actual MTD and YTD and compared to MTDLY and YTDLY 28. Supporting Reports: Covers report (productivity, hour per guest – benchmarking info) Occupancy Rates: compared to last year, compared to competition, Comp Set Unit Sold reports – product analysis – identifies group sales such as cocktails, beer and is used by management to make strategic decisions. 27. Accrual Accounting: Recognizes revenues when earned and expenses when incurred to make these revenues. 28. Cash Accounting: Revenues are had when cash is received and expenses when cash is paid 29. Forecasts A periodical estimate of revenues for the next period of accounting – realistic based on economic climate, bookings held etc – Revenue/Sales Strategy Meetings 30. Indirect expenses: Are expenses that are not directly related to revenue producing activities e.g. Administrative, General, marketing, maintenance, energy costs(undistributed operating expense). Fixed Indirect expenses are management fees, franchise fees, guest entertainment etc. Bank Reconciliations: To check that the bank general ledger code shows the same as your business code Bank and business should have the same closing balance Bank reconciliations are done monthly – large businesses do it daily Each ledger code entry is checked – any discrepancy is adjusted using a journal entry E.g. – Bank fees, direct deposits will not appear in your general ledger. E.g. – cheques presented but not cleared will appear in business general ledger but not in bank(unpresented cheques) Cheques not presented will inflate your ledger cash balance and your cheques may BOUNCE Accounting Cycle 1. Transaction Analysis - A transaction occurs Source document created or checked 2. Journalise - Details of transaction entered in journal 3. General Ledger - Journal entry is transferred to General Ledger 4. Trial Balance (unadjusted) created - Closing balance of (Dr or Cr) of each General Ledger is recorded in Trial Balance 5. Work Sheet (Optional – see attachment) 6. Ledger accounts adjusted as necessary. 7. Closing Trial Balance prepared. 8. Financial Statements prepared – Income Statement, Profit & Loss Statement, Balance Sheet INCOME STATEMENT Departmentalised statement of revenues and expenditures in hotel Varies from one establishment to another Has revenues on top of statement – e.g. Food Revenue, Beverage, Room Hire, Other, Gaming, Entertainment, management fees, franchise, investment etc Revenues are reported when earned and not received(accrual accounting)- Matching principle of accounting - Owners Equity will increase if revenues exceed expenses and will decrease otherwise Expenses are reported at the bottom of the income statement – R-E methodology applies i.e. Food is purchased is recorded as asset; however cost of sale for a food preparation is not recognised until it has been determined how much food inventory was sold Departmental Contributory Income is Income before Tax – Departmental revenues less Departmental managers control their departments with total autonomy and responsibility Typical questions an Income Statement answers a) Sales in month – compared to budget, LYMTD, Last Month,YTD, LYYTD b) Cost of goods sold - Food, Beverage, Other compared to budget – compared to industry benchmarks c) Profitability of department d) What we can do to minimise costs, increase profits, increase revenues without incremental costs? e) – Profit or Cost centre – incentivised. f) Productivity and wage cost % - compared to budget, industry benchmarks? g) How did we go compared to forecasts Each department manager critiques their department. Employee costs are computed based on FTE equivalent or other relevant method of referral. Net Food cost => cost of food after all adjustments such as staff meals, entertainment costs are taken off. Employee meal costs are recoded to employee benefits as expense. Indirect expenses are expenses that are not directly related to revenue producing activities. Controllable costs but not directly controlled by department managers(normally GM of property – Note - wages for people responsible for controlling these costs are part of this cost as well) Income before fixed charge is a critical line in Income statement – measures overall efficiency. Fixed charges relate to property taxes, insurance, interest, depreciation etc. Income tax is applied to this final income to calculate Net Income of department. Net Income is transferred to balance sheet as Earnings. COST OF SALES: Cost of Sales = Opening Stock + Purchases – Closing Stock Perpetual Inventory Control – daily/continuous updating of receipt and sale of each inventory item. Cost of sales adjustments – interdepartmental transfers, employee meals, promotional expense Inventory Valuation Methods 1. Specific Item Cost – individually costed 2. First In First Out – stock rotation 3. Last In, First Out – not good during inflationary pressure periods as margins will suffer. 4. Weighted Average BALANCE SHEET Assets: Current Assets – that can be converted into cash in a short period, less than a year. 1. Cash on hand 2. Cash in Bank 3. Marketable securities – e.g. Bonds, Short term investments, term deposits(foot note to indicate present or market value) 4. Credit Card Receivables (merchant summary). 5. Accounts receivables – Bad Debts? 6. Inventories – predominantly Food, Beverage, supplies in hotels. 7. Prepaid Expense –e.g. insurance, rates, taxes, license fees Fixed Assets – long life, permanent in nature, not intended to be sold 1. Land, Building, Furniture and Equipment 2. Accumulated Depreciation – due to wear & tear, decline or increase in value due to economic factors etc. 3. China, Glassware, Silverware(still new and in storage Other Assets: which does not fit into either fixed or current assets 1. Deposits – refundable in the future – e.g. public utility company deposit 2. Investments – Long term 3. Leasehold Costs or Leasehold Improvements – leased land – cost of this is spread over the lease period or in other words AMORTIZED. Amortization applies to intangible assets such as Goodwill or deferred expenses 4. Deferred Expenses - similar to prepaid expense however long term e.g. prepaid mortgage expense to claim additional discount in long term cost – is normally amortized(spread) over the life of mortgage. LIABILITIES Current Liabilities – that must and can be paid in a short period, less than a year. 1. Accounts Payable – Trade – suppliers 2. Accrued Expenses – Unpaid wages, Unpaid salaries, payroll tax or similar costs 3. Income Tax Payable 4. Deposits and Credit balances – Unearned Income – Prepaid deposits etc 5. Current Portion of long term mortgage(debts due within a year) 6. Dividends Payable – if declared and unpaid Long Term Liabilities – that are due beyond one after balance sheet date. 1. 2. Stock Holders Equity – Owners interest in enterprise – Capital Stock and Earnings Capital Stock – Authorized number of sharesPar or Stated Value (par times number of shares actually issued up to the authorised qty is the value of Capital Stock). Other stock types are preferred stock and common stock. Common Stock - Units of ownership in a public Company for which the holders can typically vote on matters Pertaining to the company and receive dividends from the Company’s growth. Common stockholders are the last to receive Assets if the company liquidates. Preferred Stock - stock whose holders are guaranteed priority in the payment of dividends but whose holders have no voting rights 3. Paid in Capital – Excess of Par- additional monies received when stocks were sold more than its par value 4. Retained Earnings – All net income or losses of an incorporated business. Can be used to offset dividends, extraordinary losses, prior period adjustments or for capital growth of company. 5. Proprietorship and partnership – Sole owner Vs more than one owner. 6. Statement of Capital = Beginning Capital + Net Income/Loss – Owners Withdrawals = Ending Capital Balance Sheet Detail – Representation varies and is dependant 1. on information desired, 2. Type of business – Partnership/Proprietorship or Inc 3. Can be very simple and easy to read with additional foot notes and addendums for specific details. 4. It depicts the real picture of the business – liquidity of business, earnings of owners, breakdown of assets, business liabilities 5. Limitations are a. True value of assets may not be real as the figures were true when the transactions were recorded. Does not show market value b. Goodwill built up is not reflected on balance sheet. c. Balance sheet does not show any value or investment that business has spent on its employees. d. Some values are estimates or judgemental figures e.g. depreciation and method used. e. Balance sheet is the true value of business at the time the figures for its making was entered COST/PROFIT CENTRES IN HOTEL Outlet Cost Kitchen Bar Restaurant Gaming Spa Marketing Car Parking Front Office Human Resources Profit Responsibility