salary sacrifice - National Union of Teachers

advertisement

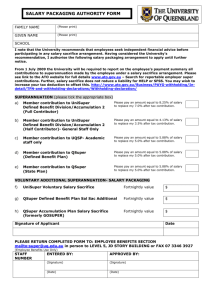

SALARY SACRIFICE SCHEMES NUT GUIDANCE From 1 June 2006, all teachers will be able to take part in “salary sacrifice” schemes offered by their employers. These schemes allow employees to obtain certain kinds of benefit - in particular childcare vouchers - on a tax-free basis in return for surrendering part of their pay. This briefing note explains how “salary sacrifice” schemes operate and advises on the implications for NUT members considering whether to take part. WHAT ARE “SALARY SACRIFICE” SCHEMES? 1. Salary sacrifice schemes allow employees to take advantage of tax exemptions for the costs of certain kinds of non-cash benefits provided by their employers. 2. The employer enters into an individual contractual agreement with each employee taking part in the scheme. The employees agree to give up part of their gross pay and the employer agrees to provide in return non-cash benefits to the same value. The employees then receive these non-cash benefits free from income tax and National Insurance contributions which they would otherwise have paid on those amounts of gross pay. 3. From April 2006, the exemption from income tax and National Insurance (NI) contributions applies to schemes providing Childcare Vouchers or other childcare benefits, schemes providing cycles or cyclists’ safety equipment for travel to and from work and schemes permitting the purchase of mobile phones from employers. The exemption for home computers purchased from employers was ended by the 2006 Budget. 4. The exemption from income tax and NI contributions currently applies to the first £55 in value per week of the benefits. The exemptions significantly reduce the cost of such benefits to employees in comparison to the cost of buying such benefits from take-home pay after tax. Employees could, for example, obtain £55 in childcare vouchers in return for giving up £55 in gross pay which might otherwise have amounted to only some £35-40 in take-home pay after income tax and NI contributions. 5. The exemptions apply to benefits provided by employers in addition to pay, for example as recruitment or retention incentives for teachers. They apply also to benefits provided in place of pay under salary sacrifice arrangements. 6. At www.hmrc.gov.uk/specialist/salary_sacrifice.pdf you can find detailed Inland Revenue on salary sacrifice schemes. Advice should also be available from any employers operating salary sacrifice arrangements for their employees. 2 TEACHERS AND SALARY SACRIFICE 7. From 1 June 2006, all NUT members will be able to take part in salary sacrifice schemes and take advantage of the income tax and NI exemption. 8. Teachers employed in local authority maintained schools will become entitled to take part in salary sacrifice schemes run by local authorities with effect from 1 June 2006. Previously, many authorities had excluded such teachers from their schemes on the basis of DfES advice that employers were statutorily required to pay such teachers their full pay entitlements irrespective of any salary sacrifice agreement. The NUT made representations to DfES Ministers in summer 2005 and again in autumn 2005 asking for the law to be changed to allow such teachers to take part in local authorities’ salary sacrifice schemes. The NUT is pleased to report that its representations were successful and that the necessary amendments to the teachers’ pay structure have been made to allow this. 9. Other NUT members have previously been entitled to take part in salary sacrifice arrangements offered by their employers. They include: 10. NUT members employed on Soulbury terms and conditions; supply teachers working in local authority maintained schools who are employed via supply agencies; teachers in local authority maintained residential social services establishments employed on JNCTRE terms and conditions - but not teachers in local authority maintained residential special schools; teachers in sixth form colleges. teachers in Academies ,including those paid in line with the STPCD; and teachers in CTCs and independent schools. Employers must agree to set up salary sacrifice schemes before their employees can take part. If your employer does not currently operate a salary sacrifice scheme, contact your local NUT division or association for advice and assistance. IMPLICATIONS FOR PENSIONS AND BENEFITS 11. The NUT has persuaded the DfES to change the rules of the Teachers’ Pensions Scheme (TPS) to ensure that salary sacrifice arrangements do not affect TPS members’ pension entitlements. Other NUT members considering taking part in salary sacrifice arrangements should, however, be aware of the possible implications for their pensions. 12. Most pension schemes provide that the rate of pay used to calculate contributions and pension entitlements excludes pay surrendered under salary sacrifice schemes. The pay rate used to calculate pension entitlements in such cases is the pay rate net of the salary sacrifice element. Salary sacrifice arrangements could, therefore, affect employees’ pension entitlements in such cases if they retired, including retirement on ill-health grounds, or died in service within three years of the ending of any such arrangements. 3 13. The DfES has announced its intention to amend the rules of the TPS later in 2006 in order to make clear that where salary is sacrificed, the sacrificed portion of pay will count as pensionable. 14. NUT members who are members of other pension schemes such as the Local Government Pension Scheme should seek advice on this issue from their employers or pension scheme administrators. 15. NUT members should also be aware of possible implications for entitlement to other benefits including contributory or earnings related benefits such as: 16. statutory sick pay, statutory maternity pay, maternity allowance and incapacity benefit; and tax credits such as Working Tax Credit and Child Tax Credit. It is unlikely that any NUT members would be affected by these implications for other benefits, unless they were working on a part time basis for a rate of pay close to the NI Lower Earnings Limit. NUT members should nevertheless seek appropriate advice from the employer or other expert source. REGISTERING AN INTEREST IN SALARY SACRIFICE 17. The DfES has provided brief guidance on this area, including a model form for teachers to register an interest in taking part in salary sacrifice schemes, via the Teachernet website at www.teachernet.gov.uk/docbank/index.cfm?id=9792 18. As noted earlier, NUT members employed in LEA maintained schools should contact their NUT division or association with regard to the availability of salary sacrifice schemes in their area. NUT Salaries Dept May 2006