Central Counterparty for Equities Guidance Note Dec 2000, 04/00

advertisement

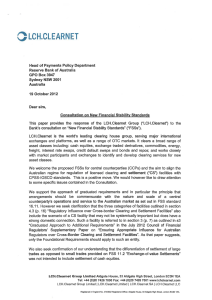

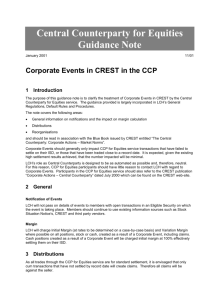

Central Counterparty for Equities Guidance Note December 2000 04/00 Balance sheet reporting 1 Background Although the principal-to-principal structure of the central counterparty model was established in the early stages of the project, some prospective General Clearing Members (GCMs) have only recently appreciated that the structure has implications for their balance sheet accounting and credit risk information systems. This is an issue both for GCMs in relation to their business with NCMs; and for GCMs and ICMs in relation to business with clients which is currently labelled ‘agency’ business. The issues were raised bilaterally with LCH by three firms and discussed in a broader forum with LIBA’s Settlement Working Party. LCH was asked, and agreed, to re-examine the principal-to-principal structure built into the proposed LCH-GCM-NCM agreement and its Regulations to see whether it could make changes that would obviate the need for the balance sheet reporting. It was suggested that a structure in which the GCM gave an irrevocable commitment to assume the NCM/client’s settlement obligations in the event of the latter’s non-performance would relieve the need for reporting. 2 Conclusion of re-examination LCH has reviewed the contractual-legal structure with its advisers and concluded that it cannot make the suggested change to a hybrid agency-principal structure. The basis of the conclusion is that such a structure would be ambiguous and would fall outside the statutory insolvency protection offered to LCH under Part VII of the Companies Act 1989. The effectiveness of that protection is of fundamental importance to the security of LCH’s central counterparty arrangements, and at the same time to the clearing members who of course provide the default backing of the company. The effect of the removal of Part VII protection would be to introduce uncertainty as to LCH’s right to apply the initial margin of a defaulting member to offset default losses. The Default Fund contributions of non-defaulting members would therefore be more at risk. The contractual structure will thus remain as shown in the diagram below: LCH l in pr a cip GCM - AAA pr in cip al ICM - CCC gin ori e ad l tr a principal NCM - BBB Client Client 3 Accounting treatment Contact with prospective GCMs has revealed a range of views on what needs to be reflected on their balance sheet: It is not necessary to reflect the NCM/client business on balance sheet Mark-to-market value should be shown Total trade consideration should be shown Individual trade values should be shown. LCH has spoken to accountants and been told that contract values should be shown (FRS5 debtor-creditor entries) and that knowledge of client exposures will also be required under FSA/SFA reporting and credit risk requirements. But the situation is complex, particularly in the case of multi-national firms, and firms should of course seek their own advice in the light of their own group and legal structures. 4 Regulatory capital requirements The FSA has advised that whether or not client-related exposures are on- or off-balance sheet is not a factor in the applicable regulatory requirements. The SFA Rules and FSA Guide to Bank Supervision, although detailed, seem relatively clear on this issue, but firms should of course seek advice from their relevant Supervision Team or Complex Groups Division, Policy at the FSA if they are uncertain. 5 Calculation of balance sheet positions GCMs may require net receivables/payables by NCMs, by trade date, in order to meet balance sheet reporting requirements. The information can be derived from LCH’s PC margin calculation tool, PC ERA. In addition to PC-ERA’s existing reports, LCH could, if members wish, develop a new report to provide details of variation margin and consideration by trade date for balance sheet reporting purposes. Whilst PC ERA has been specifically developed for use in a testing environment, LCH will , if there is member demand, provide additional support for the PC tool in an interim period for members whose systems will not provide this functionality by 26 February 2001. 2 Questions pertaining to this guidance note should be directed to: Name Number E-mail Christopher Jones +44 20 7426 7103 mailto: jonesc@lch.co.uk Andrew Lamb +44 20 7426 7055 mailto: lamba@lch.co.uk List of guidance notes The project has published a number of guidance notes. The others published to date, or in production, are listed below, please contact the project for any later guidance notes. 01/00 Disclosure of shareholdings 02/00 UK Stamp Duty Reserve Tax 03/00 Agency and riskless principal trading 04/00 Balance sheet reporting 05/00 Impact of late settlement (to be published) 06/00 Irish Stamp Duty (to be published) Contact points The CCP for Equities project can be contacted on 020 7849 0510 or via email at ccp@crestco.co.uk. Members of the Exchange, LCH or CRESTCo can also make use of their usual contacts in these organisations. Information about the service is also available on the following websites: www.crestco.co.uk www.lch.co.uk www.londonstockexchange.com This guidance note has been prepared by the London Stock Exchange, LCH and CRESTCo to assist participants in their planning for the CCP for Equities project. The London Stock Exchange, LCH and CRESTCo do not represent or warrant the completeness or accuracy of the information contained in this guidance note. Recipients should not rely on this guidance, which is not a substitute for specific legal advice, and should consult their own legal advisers. © December 2000 CRESTCo Limited, registered in England and Wales No 2878738, London Stock Exchange plc, registered in England and Wales No 2075721, and The London Clearing House Limited, registered in England and Wales No 25932. The CREST logo is a trademark of CRESTCo Limited. SETS, SEAQ, SEATS Plus and the London Stock Exchange crest and logo are trademarks of London Stock Exchange plc. The London Clearing House logo is a trademark of The London Clearing House Limited. 3