Document

advertisement

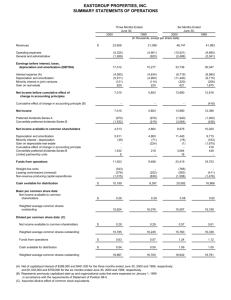

1ST Mock Exam 2012-2013 2. Ocean Limited owns the following non-current assets as at 1 January 2010: (i) (Depreciation) On 1 October 2010, an old motor vehicle costing $350,000 with a net book value of $100,000 as at 1 January 2010 was trade-in for a new one. A trade-in allowance of $9,000 was given. The list price of a new vehicle is $400,000 and a trade discount of 10% was allowed. Ocean Limited paid $2,400 for annual license fee, $10,000 for installing an air-conditioning system in the motor vehicle and $3,000 for freight charges. The scrap value of the new machine is $4,000. Ocean Limited had only credited sales account for $9,000. No other entries have been made. (ii) Ocean Limited adopts the following depreciation policies for its non-current assets: Motor vehicle – 20% on reducing balance method per annum REQUIRED: (a) Calculate the cost of new vehicle to be capitalized. (b) Prepare journal entries to correct the error above for the year ended 31 December 2010. (a) $ 360,000 10,000 3,000 373,000 Purchases price ($400,000 x 90%) Air-conditioning system Freight charges Cost of motor vehicle (b) Journal Sales Suspense Accumulated depreciation – Motor vehicle [$100,000 x 20% x 9/12 + ($350,000 $100,000)] Motor vehicle – trade-in allowance Profit and loss – Loss on disposal Motor vehicle Motor vehicle ($373,000 $9,000) License fee ($2,400 x 3/12) Prepayment ($2,400 $600) Bank Depreciation – Motor vehicle ($373,000 x 20% x 3/12) Accumulated depreciation – Motor vehicle Debit $ 9,000 Credit $ 9,000 265,000 9,000 76,000 350,000 364,000 600 1,800 366,400 18,650 18,650 Pre-Mock Exam 2012-2013 (Depreciation) 5. The following is the extract of the trial balance before the preparation of financial statements of Original Company as at 31 December 2010. Dr ($) Cr ($) Building 600,000 Machinery 480,000 Accumulated depreciation – Building ? – Machinery ? Accounts receivable 59,000 Bad debts 4,000 Allowance for doubtful debts 1,400 The following information is related to non-current assets and accounts receivable of Original Company: (i) The existing allowance for doubtful debts should be adjusted to 3% of accounts receivable. (ii) The company’s building was acquired on 1 January 2005. On 1 July 2010, the building was extended and the following expenditures were incurred. No entry has been made with regard to this extension. Construction materials used Labour cost Installation of lighting system Furniture: movable desks Total payment made by cheque (iii) $ 85,000 55,000 20,500 26,750 187,250 A new machine was bought on 1 March 2010 and the following costs were incurred. No entry has been made for this acquisition. List price Delivery expenses Repair expenses incurred due to an accident happened during delivery (iv) $ 100,000 20,000 5,000 Depreciation policy on machinery is reducing balance method of 20% and existing machinery was bought on 1 January 2007. Depreciation rate of building and the extension is 2% on cost. Depreciation is provided on a pro-rata basis. (v) It was discovered that a debtor balance of $1,000 has been omitted from the list of debtors and has not been included in accounts receivable in the trial balance. REQUIRED: (a) Compute the cost of the extension and the new machine to be capitalized. (2.5 marks) (b) Prepare the accumulated depreciation accounts of building and machinery for the year ended 31 December 2010. (7 marks) (c) Find the amount of allowance for doubtful debts and any expense or profit of this allowance incurred or earned against the profit for the year ended 31 December 2010. (2.5 marks) (d) Briefly explain the accounting concept applying to both providing allowance for doubtful debts and depreciation for non-current assets. (3 marks) (Total: 15 marks) (a) Cost of the extension Construction materials used Labour cost Installation of lighting system $ 85,000 55,000 20,500 160,500 Cost of the new machine List price Delivery expenses $ 100,000 20,000 120,000 (b) Balance c/d Accumulated depreciation - building $ 73,605 Balance b/d (600,000 x 2% x 5) Depreciation (W1) 73,605 $ 60,000 13,605 73,605 W1: 600,000 x 2% + 160,500 x 2% x 6/12 = 12,000 + 1,605 = 13,605 Balance c/d Accumulated depreciation - machinery $ 303,392 Balance b/d (W2) Depreciation (W3) 303,392 $ 234,240 69,152 303,392 W1: 480,000 x 20% + 480,000 x (1 – 20%) x 20% + 480,000 x (1 – 20%) x (1 – 20%) x 20% = 234,240 W2: (480,000 – 234,240) x 20% + 120,000 x 20% x 10/12 = 49,152 + 20,000 = 69,152 (c) Allowance for doubtful debts this year = (59,000 + 1,000 – 4,000) x 3% = 1,680 The expense incurred in increase in allowance for doubtful debts = 1,680 – 1,400 = 280 (d) — Under the matching concept, expenditure incurred should match with the revenue generated in the same accounting period. — The cost of non-current assets should match with the revenue generated. Depreciation is thus provided to allocate the cost of non-current assets over their estimated useful life. — Under the prudence concept, allowance for doubtful debts is to be made in the year to ensure that sales revenues are not overstated. HKDSE (2012, 2) The non-current assets of Moody Company as at 31 December 2010 were as follows: Cost Accumulated depreciation $ $ Machinery (all purchased in 2007) 3 600 000 3 455 000 Lorries (all purchased in 2008) 1 850 000 1 200 000 (Depreciation) The following were transactions relating to the non-current assets of the company during 2011: (i) On 1 March 2011, a piece of machinery was bought at a price of $2 400 000. On the same date, a component costing $60 000 was installed into the machinery to increase its productivity over the coming four years. (ii) On 1 January 2011, a lorry was bought at a price of $1 900 000. The price included an insurance premium of $36,000 covering the year ended 31 December 2011. It is the company’s policy to depreciate machinery at a rate of 25% per annum on cost, and lorries at a rate of 20% per annum using the reducing balance method. REQUIRED: (a) For Moody Company, (1) calculate the depreciation expenses of the machinery for the year ended 31 December 2011; and (2) prepare the accumulated depreciation account of lorries for the year ended 31 December 2011. (b) Different methods are used to depreciate the non-current assets of Moody Company. Explain whether such a difference in accounting treatments violates the consistency principle. Depreciation for old machine = 3 600 000 x 25% = 900 000 (a) (1) Depreciation expenses = ($3 600 000 $3 455 000) + ($2 400 000 + $60 000) x 0.25 x 10/12 NBV = 3 600 0003 455 000 = 145 000 = 145 000 + 512 500 = 657 500 (a) (2) Accumulated Depreciation – lorries 2011 Dec 31 Balance c/d $ 2011 1 702 800 Jan Dec 1 702 800 1 Balance b/d 31 Depreciation (W1) $ 1 200 000 502,800 1 702 800 W1: Depreciation for lorries = ($1 850 000 1 200 000) x 20% + ($1 900 000 $36,000) x 20% = $502 800 (b) It does not violate the consistency concept Reasons: — consumption pattern is different for different types of non-current assets — the company is consistently applying the same depreciation method for the same type of non-current assets. HKET Mock (4, 2011) (Depreciation) 4. A sole proprietor Ms. Ho owned a machine for production. Since the number of order has increased recently, that machine could not meet the required production volume. She decided to sell the machine and then buy a new suitable one. Here is the information related to the old machine: Purchase date Purchase cost Date of disposal Disposal value (in cash) Method for depreciation : : : : : 1 July 2007 $450,000 31 October 2011 $120,000 Reducing balance method 25% for each year *Depreciation is calculated on pro-rata by months if the period is less than one year. REQUIRED: Prepare the following accounts for Ms. Ho for the year 2011: (a) Machine Account (b) Accumulated Depreciation Account – Machine (c) Disposal Account – Machine (d) Income Statement (Extract) (a) Machine 2011 Jan 1 Balance b/d $ 2011 450,000 Oct 31 Disposal – Machine $ 450,000 (b) Accumulated Depreciation – Machine 2011 Oct Year 2007 2008 2009 2010 2011 31 Disposal – Machine $ 2011 318,494 Jan Oct 318,494 $ 283,887 34,607 318,494 1 Balance b/d 31 Depreciation Depreciation $56,250 $98,438 $73,828 $55,371 $34,607 $450,000 x 25% x 6/12 = ($450,000 $56,250) x 25% = ($450,000 $154,688) x 25% = ($450,000 $228,516) x 25% = ($450,000 $283,887) x 25% x 10/12 = Accumulated Depreciation $56,250 $154,688 $228,516 $283,887 $318,494 (c) Disposal – Machine 2011 Oct 31 Machine $ 2011 450,000 Oct Oct Oct 450,000 31 Accumulated Depreciation – Machine 31 Cash 31 Profit & Loss – Loss on disposal $ 318,494 120,000 11,506 450,000 (d) Ms. Ho Income Statement for the year ended 31 December 2011 (Extract) $ Expense : Depreciation Machine Loss in disposal of machine 34,607 11,506 HKDSE Sample 2 (2A, 3) (Depreciation) Subsequent checking of the records by the accountant of Easy Company revealed that no entries had been made for the following items: (i) Loan interest of $5050 incurred in 2011 remains unpaid as at 31 December 2011. (ii) A motor vehicle costing $80 000 with an accumulated depreciation of $40 000 as at 31 December 2011 was sold for $48 000 in cash on the same date. REQUIRED: (b) Prepare the journal entries to record the above transactions for the year ended 31 December 2011. (Narrations are not required.) (c) Explain the accounting treatment of item (i) using a relevant accounting concept. Answer: (b) Journal 2011 December (i) Loan interest Debit $ 5050 Accrued loan interest (ii) Accumulated depreciation – Motor vehicles Cash Motor vehicles Profit and loss – Profit on disposal of motor vehicles Credit $ 5050 40 000 48 000 80 000 8 000 (c) Accrual concept — Unpaid loan interest should be credited to accrued loan interest account to represent an increase in current liability in 2011. — The loan interest incurred should be debited in the profit and loss account as an increase in operating expenses of 2011. HKDSE Sample 1 (2A, 1) A company has incurred the following expenditures on a new machine purchased for business use: $ List price (allowance of 20% trade discount) 800,000 Legal fees related to the purchase 5,200 Machine installation and adaption 7,300 Maintenance fee 9,900 Testing 6,500 Initial training for operators 3,000 (Depreciation) The manager expects the efficiency of the machine to decline sharply over its useful life. He would like to adopt a depreciation method that will best meet the nature of the machine. REQUIRED: (a) Calculate the cost of the machine to be capitalized. (b) (i) Identify a depreciation method that is in line with the manager’s view. (ii) Explain one advantage of the depreciation method you identified in (i). (a) Purchase cost ($800,000 x 80%) = $640,000 Legal fees related to the purchase = $5,200 Machine installation and adaption = $7,300 Testing = $6,500 Cost of the machine = $640,000 + $5,200 + $7,300 + $6,500 = $659,000 (b) (i) Reducing balance method (ii) Advantage: even allocation of total fixed asset usage costs (depreciation and maintenance) appropriate matching of cost with benefits derived HKCEE (2009, 1) (Depreciation) The financial year for Victor Company ends on 31 December each year. The following fixed assets schedule was prepared on 31 December 2008: Fixed Asset Furniture A Office equipment X Furniture B Office equipment Y Furniture C Acquisition Date Cost Estimated Salvage Value Depreciation Method Estimated Useful Life/ Annual Depreciation Rate Depreciation Expenses 2007 2008 $ $ $ $ 1 Jan 2006 100,000 (1) Straight-line 4 years 22,000 (2) 1 Mar 2007 200,000 33,614 Reducingbalance 30% (3) (4) 15 July 2007 (5) 5,000 Straight-line 5 years (6) 8,000 20 Sept 2008 280,000 Reducingbalance (7) 56,000 1 Oct 2008 76,000 4,000 Straight-line 10 years (8) Additional information: (i) It is the company’s policy to charge a full year’s depreciation on fixed assets purchased in the first half of the financial year. For fixed asset purchased in the second half of the financial year, a half year’s depreciation is charged. (ii) On 1 November 2008, the company spent $5,000 to extend the useful life of Furniture C and $600 for the maintenance of this asset for the two years ended 31 December 2009. These amounts had been included in the cost of Furniture C at 31 December 2008. REQUIRED: Compute the correct amount/depreciation rate for items (1) to (8) in the schedule above. (1) $12,000 $100,000 $22,000 x 4 = $12,000 (2) $22,000 (3) $60,000 $200,000 x 30% = $60,000 (4) $42,000 ($200,000 $60,000) x 30% = $42,000 (5) $45,000 $8,000 x 5 + $5,000 = $45,000 (6) $4,000 $8,000 x 1/2 = $4,000 (7) 40% ($56,000 x 2) ÷ $280,000 = 40% (8) $3,570 ($76,000 $4,000 $600) ÷ 10 x 1/2 = $3,570 HKCEE (2008, 2) (Depreciation) (A) Mr Chan started his trading business on 1 January 2007. On that date, the company bought a computer for office use, costing $12,000. The computer was expected to be used for 3 years before it would be replaced by more advanced model. As at 31 December 2007, Mr Chan decided that the computer be carried at its original cost of $12,000 on the balance sheet, without providing for depreciation. REQUIRED: State the accounting principle or concept that has been violated and provide an explanation. (B) The financial year of Wingding Company ends on 31 December. In 2007, the company bought a machine at a cost $58,000 and paid a deposit of $8,000 on 1 April 2007. The machine was delivered and installed on 1 July 2007. An accident occurred on the same day and repair charges amounting to $2,000 were paid. The company settled the balance of the machine price on 1 October 2007. The machine was estimated to have a useful life of 4 years and a scrap value of $4,000. It is the company’s policy to depreciate its fixed assets on a straight line basis. The machine had a major breakdown in early 2008 and was disposed of on 30 April 2008 for $25,000. REQUIRED: Prepare the necessary journal entries to record the above. (Note: Narrations are not required.) (A) Matching concept The matching concept links revenue with its relevant expenses or costs. The use of the office equipment contributes to the generation of revenue of the business. The cost of the office equipment should therefore be allocated over its useful life on a systematic basis. e.g. straight line basis. The cost of using the office equipment during the year (the depreciation) should be recorded as an expense (in the profit and loss account) for the year ended 31 December 2007. (B) Journal Date 2007 Apr Jul “ Oct Dec Details 1 Deposit – machine Bank 1 Machinery Creditors Deposit – machine 1 Repair expenses Bank 1 Creditors Bank 31 Depreciation expense [($58,000 – $4,000) ÷4 x 6/12] Accumulated Depreciation – machinery 2008 Apr 30 “ 30 Depreciation expense [($58,000 – $4,000) ÷4 x 4/12] Accumulated Depreciation – machinery Accumulated Depreciation – machinery ($6,750 + $4,500) Bank Profit and loss (Loss on disposal of machinery) Machinery Dr $ 8,000 Cr $ 8,000 58,000 50,000 8,000 2,000 2,000 50,000 50,000 6,750 6,750 4,500 4,500 11,250 25,000 2,1750 58,000 HKCEE (2007, 2) (Depreciation) (A) Nelson Company traded-in a used machine for an advanced model in April 2007. The old machine had a net book value of $12,000 and a trade-in value of $10,000. Nelson Company paid the following expenditures for the new machine during April 2007: (i) Cash of $55,000 for the exchange. (ii) $5,000 for a training course for workers on the operation of the new machine. (iii) $4,000 for the delivery of the new machine. (iv) $1,000 for insurance during transportation of the new machine. (v) $8,000 for a specially made steel case to house the new machine. (vi) $2,000 for the installation of the new machine. (vii) Repair cost of $3,800 for accidental damage during installation. (viii) $1,200 for the lubricants to be used with the machine during its first year of operation. You are required to: Prepare for Nelson Company a statement to calculate the cost of the new machine. (A) Cost of the new machine Acquisition cost ($10,000 + $55,000) Delivery charges Insurance Steel case Installation cost $ 65,000 4,000 1,000 8,000 2,000 80,000 (B) After preparing its final accounts for the year ended 31 March 2007, Babel Company found that the following transactions had been omitted from the books. For each of the omissions, state the change (increase / decrease / no change) in the net profit for the year and the working capital as at the year end after the omission has been corrected. Net profit for the year ended 31 March 2007 Working capital as at 31 March 2007 No change Increase Example: After expenses at 31 March 2006 were paid by the proprietor from his own bank account (a) A motor vehicle was sold on credit at a profit ? ? (b) A short-term bank loan, together with the accrued interest on the loan, was repaid. ? ? (c) Goods were purchased by cash for resale. These goods were sold on credit at a loss. ? ? (d) A customer settled his account. The amount received was used to pay a creditor and the electricity expenses of the proprietor’s residence. ? ? (B) (a) (b) (c) (d) Net profit for the year ended 31 March 2007 Increase No change Decrease No change Working capital as at 31 March 2007 Increase No change Decrease Decrease HKCEE (2006, 2) (A) State the major characteristics of fixed assets. (Depreciation) (B) Valor Company acquired a machine on 1 January 2002. The machine has an estimated useful life of 5 years. The depreciation charge for the first three years was calculated for this machine using two different depreciation methods as follows: Straight-line method (5 years) Year 2002 2003 2004 Reducing-balance method (50% per annum) $12,400 12,400 12,400 $32,000 16,000 8,000 You are required to: (a) State three causes of depreciation. (b) Calculate the cost of the machine and its estimated residual value. (c) Prepare journal entries to record the disposal of the machine based on the straight-line method, assuming that the machine was sold on 30 September 2005 for $36,000 on credit. (Narrations are not required) (A) Major characteristics: they are long-term in nature and can benefit the business for more than one year. they are material in amount. they have physical substance. they are acquired for use in the operations of the business and not for resale. (B) (a) Causes: physical wear and tear. obsolescence. inadequacy. passage of time. (b) Cost of the machine: $32,000 ÷ 2 = $64,000 Estimated residual value of the machine: $64,000 $12,400 x 5 = $2,000 (c) Journal Debit $ Debtors 36,000 Provision for depreciation – machinery ($12,400 x 3 + $12,400 x 9/12) 46,500 Credit $ Machinery 64,000 Profit and loss (Profit on disposal of machinery) 18,500