230-Corporations_I-Childs-Erin_Frew

advertisement

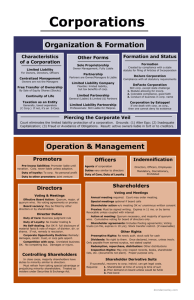

CORPORATIONS I (LAW 230A) Instructor – Childs (2008 T1) SUMMARY 1. PARTNERSHIP What is the nature of partnership? A partnership is a network of interlocking agency. Partnership was developed by the common law and codified in statute. Partnership is an arrangement with more than one equity investor. You do not need to intend to form a partnership. Partners are considered agents of each other (multilateral agency: actual or ostensible)—this is the source of unlimited liability. Partnerships have no legal separate identity. Partnership ends at the death or bankruptcy of one of the partners. Partners have unlimited liability for debts and obligations of the partnership. It is easy to form and dissolve a partnership—they are flexible. The Partnership Act sets out default provisions— you can opt out of specific rules. Statute: 2: definition: persons carrying on business in common with a view to a profit. 3: persons who are not a partnership 4: how to determine if partnership does or does not exist (esp 4(c)) 5: loans that look like investments—other creditors get paid first, but a weird middle ground. 81: you must register a partnership Case law: Cox & Wheatcroft v. Hickman (1960 HL): partners carry out trade together with an expectation in sharing profits. In this case they are not partners because they are just paying H until the debt is paid off. Grace v. Smith: sharing in profits raises a rebuttable presumption of a partnership Bovill’s Act: merely sharing in profits does not automatically make you a partner. This is roughly comparable to s. 4(c)(iv) of the PA Pooley v. Driver (1876 Ch. D): partnerships are determined by actions and intent, not what you call it. You cannot have the advantages of partnership without the liability of partnership. Here they were getting profits in excess of the lending debt. They are partners AE LePage Ltd. v. Kamex (1977 Ont. CA): the more tied up the property is the more likely it is to be a partnership. In this case it was merely co-ownership, and not a partnership. Intention of the parties played an important role. Volzke Construction v. Westlock Foods (1986 Alta. CA): management of the business is more than coownership of property. They are Partners. This is different from LePage: joint bank account, introductions as partners, rights, and mortgage together. Lansing Building Supply (Ontario) Ltd. v. Ierullo (1989 Ont. Dist. Ct.): the court tries to distinguish Kamex by what the group was doing, i.e. they were not carrying on business, and they were just co-owners. Even if this is not exactly what the court says. You cannot contract out of being partners. They are partners. This case is on the line. Backman v. Canada (2001 SCC): you don’t actually have to make profit, but you have to intend to at some point to be a partnership. This is not a partnership. Re Thorne and New Brunswick Workmen’s Compensation Board (1962), 33 DLR (2d) 167 (NBCA): you cannot be a partner and an employee—there is no separate legal identity Partnership Liability Third Parties partners are liable for torts and contacts of the partnership. You can sue a partnership by name. Partnerships can sue by name. the outcome of a suit is binding on all partners as plaintiffs or defendants. Partners have joint and several liabilities. There is liability in contract for purposes of the business. There is tort liability if you cause someone injury while in the process of carrying on business. Liability of trust, if one partner engages in a breach of trust the other partners are not liable. Page 1 Erin Frew CORPORATIONS I Statute: 7: liability of partners: partner as agent, unless no auth and the party had actual notice he had no authority or never believed him to be (the third party is obligated to make reasonable inquiry: LePage) 8: actual and ostensible authority both bind partnership by anyone. 9. if one partner pledges firm property for another business the partnership is not bound unless you appeared to have actual or apparent agency. Here the third party is entitled to reasonable reliance and the obligation rests on other parties to correct the apparent agency. 10: if partner’s power restricted and there was notice, act not binding 11: partners joint and several liablity for all debts and obligations of firm. If it is an estate than it is severally liable. 12: in tort, if partner acting in ordinary course of business or with authority, partnership liable 13: liability – misapplication (like trust funds) 14: liability is joint and severable for tort and misapplication claims. 15: you are not personally liable for missing trust funds unless you had notice 16: creditor liability: actual or ostensible authority binds firm. You are liable as a partner if this is why the creditor gave you money: Brown Economics 17: admission or representation of a partner concerning partnership affairs is evidence against the firm 18: if you give notice to one partner you give it to all partners 19: creditor liability: partners not liable for debts incurred before partnership, not relieved after retirement. You are only liable for de incurred while a partner 39: LOOK UP. Default governance sections – relationship between partners. Default provisions can be contracted out of. They are important if you find out you are in a partnership when you didn’t intend. It is premised on equality among partners and all partners owe each other a fiduciary duty. Fairness and good faith is the minimum standard. You must account for profits made using partnership assets or in competition with partners (ss. 32 and 33). Equal division of profit, equal apportionment of loss, partner indemnities, record keeping etc. (s. 27). Management by majority and no fundamental changes unless it is unanimous. Everyone can bind everyone else (presumption of equality). The relationship between partners and third parties is whatever is reasonable for the third party to rely on (ss. 7 and 8). Statute 21: can vary terms of statute through partnership agreement with the consent (express or inferred) of all partners 22: fid duty: partner has duty of fairness and good faith towards other partners and firm. 23: partnership property is held by the partners for the use of the partnership. 24: property bought with partnership $ deemed to be partnership property. 25: land that has become partnership property must be treated like it by the partners 26: a writ of execution cannot be made against a partnership unless it is for a judgment made against the firm 27: day-to-day running pf partnership 28: removal of partners only if power to do so has been expressly given & power in exercised in good faith 29: dissolution: any partner can end a partnership with notice to the other partners. 31: partners must give all info relating to partnership to other partners. 32: partner must account to firm for any benefit received from transaction concerning partnership. 33: partners must give to firm any profits made in competing business of same nature. 34: can assign partnership interests to another party, but new owner not “partner. 35: partnership is dissolved when it expires, at the termination of an adventure, or with notice. 36: partnership ends on death, bankruptcy, or dissolution of a partner. 37: dissolved when it is unlawful for the business to carry on 38: on application of a partner the court can dissolve a partnership Limited partnerships a limited partner’s exposure to risk is limited to the equity they put into the firm—a limitation of liability. LP’s must be registered. They must have at least one general partner. Limited partners have a restricted ability to deal in the management of the business. Also, they must not appear named with the general partner. They can not Page 2 Erin Frew CORPORATIONS I provide services. They get profits according to their contribution. This is a halfway between partnership and a corporation. Must register in Victoria: provide the identities of GPs and indicate LPs and their contributions to partnership assets; state terms of the agreement; and must use the words limited partnership in the name (s. 53). LPs cannot: pull money out if that would leave the partnership insolvent, or be involved in the management of the business Statute 51: must be express (registered) and state certain characteristics of LLP. 53: must have the words limited partnership in name, LPs cannot have their names in the title 55: limited partners can contribute money or property but not services 56: GP’s cannot carry out acts that make it impossible to carry out partnership business unless the LPs are consulted. 57: limited partners not liable for obligations of LLP except for value of capital contribution. 58: rights of limited partner (they can get information on the partnership and request that it be disolved 61: profits to be divided in proportion to respective amts of claims unless LP agt says otherwise. 64: limited partner not liable for creditor debt unless takes part in mgmt of business. 66: LP cannot assign their interest without consent of all LP’s and GP’s. Case law: Haugton Graphic Ltd. v. Zivot (1986 Ont. HC): because of his actions and control in management of the company Z is a GP and not an LP Nordile Holdings Ltd. v. Breckenridge (1992 BCCA): contrast with Haugton: here they were not purporting to be managers of the partnership but rather as managers of the corporation that is the GP Limited Liability Partnership LLP legislation was developed in response to concerns of the scope of liability of large partnerships. You must file paperwork and follower procedural rules (e.g. produce a report). Partners are not directly responsible for actions of a partner unless they were directly supervising the activity that caused the loss. LLP is not a separate legal entity. Partners have the same obligations as corporate directors: you are liable for your own bad acts PART VI of the Act 5: registration of extra-provincial LLPs 96: must be express (registered) 104: partner in LLP not personally liable for ptp obligation, unless wrongful act or omission. 2. The CORPORATION What is the nature of corp.? Separate legal personality: corporation can enter into contracts and be liable for torts arising from its business and a corporation can own its own assets. It is a legal person. Limited liability: Unless a shareholder gives a personal guarantee they are only at risk of loosing their capital investment. There is no constraint on the ability of a shareholder to manage the corporation. Perpetual Existence: shareholder death or bankruptcy has no effect. May exist indefinitely. Different individuals involved Shareholders: these are equity investors. Shares are bundles of legal rights that investors can assert primarily against the corporation. Rights must include the right to share in a distribution of the profits of the corp. (dividends), the right to share in a distribution of the net proceeds of liquidation on the dissolution of the corporation, and the right to vote on important matters concerning the corporation. Shareholders may get benefits from increase in capital. Shareholder vote to elect the directors. Unless a shareholder gives a personal guarantee they are only at risk of loosing their capital investment. There is no constraint on the ability of a shareholder to manage the corporation. Directors: elected by the shareholders annually. They can be removed by ordinary resolution. They appoint officers and managing directors and sub committees of the corporation. They run the company and set policy. Page 3 Erin Frew CORPORATIONS I Directors can wear multiple hats. The corporation acts through its directors. There are technical rules on who can be a director: residency, etc Officers: CEO, COO, CFO, etc. These are senior management employees. They are agents of the company. They have some of the same fiduciary obligations as directors. They are hired by the directors. Others: directors may owe duties to more than just these people and the company: those affected by what the corp. does and its existence / demise. E.g. creditors, customers, employees, community around them, environment, and lease holders. Reasons for incorporation Limitation of liability for shareholders, gives the corporation a perpetual existence independent of its shareholders, ease of transfer of shares, shareholder cannot obligate the body corporate, shareholder can contract with or sue the body corporate, tax advantages may accrue, and provides a way of raising funds through selling shares Symbolic function of being a serious business Default Share Structure One class of voting shares with equal rights and no restrictions on alienability. Who can incorporate? (s. 5) 18 + Cannot be of unsound mind Cannot be bankrupt Can be a real person or a company Process for incorporation Must establish articles and other fundamental documents. The CBCA sets out requirements for articles. There are restrictions on names of corporations. Two modes: (1) letters patent: the CBCA (2) memorandum of articles: Old BC Companies Act Steps: 1. select a jurisdiction 2. do a name search through NUANS 3. File articles of incorporation (s. 6(1)) (you want to keep these simple because they are hard to change) a. Shares must set out: classes of share, max number of shares, rights and privileges attaching to shares, authority to be given to directors to establish rights and privileges, any restrictions on the issue, transfer or ownership of shares. b. Number of directors (s. 6(1)(e)) c. Restrictions on the business of the company 4. file notice of registered office of the company 5. file notice of directors: must provide addresses of directors. This is important because directors have significant powers and anyone dealing with the company has to be able to see who has the authority. 6. pay prescribed fee (250 / 50) Statute incorporation, general business of corp, articles and bylaws 5: incorporators must be 18 yrs, not of unsound mind, not bankrupt. 6: what must be in the articles, incl share structure (can put restrictions too). 7: articles must be sent to Director. 9: corp comes into existence on date shown on cert of incorp 10(5): corp will use its name in all K’s, instruments made on behalf of corp. 15(1): corp has the rights of a natural person. Also substantially abolished ultra vires rule. 16(2): corp’s business and powers can be restricted in articles. 103(1): create bylaws (post-incorp) 105: qualifications of directors. 106: notice of directors must be sent to Director at time of incorporation. Page 4 Erin Frew CORPORATIONS I Case Law: Salomon v. Salomon & Co. Ltd.; Salomon & Co. Ltd. v. Salomon (1897 HL): a corporation’s legal personality is separate and independent from its shareholders. It is not an abuse of creditor / debenture process. As long as you comply with the legal obligations the company is a separate legal person, not an agent or the trustee. It is a separate person. Lee v. Lee’s Air Farming Ltd. (1961 JCPC) (NZ): affirms Salomon. A company is its own legal entity and not the identity of its directors / controlling shareholders. Mrs. Lee is entitled to WCB for Mr. Lee’s death. A one person corporation even though you are the sole employee you are still the employee of the company because of its separate legal identity. You can be employed by your own company. Macaura v. Northern Assurance Co. Ltd. and others, (1925 Eng. HL): there is no insurable interest as a shareholder. Kosmopoulos v. Constitution Insurance Co., (1987 SCC) (Wilson J.): the sole shareholder of a corporation has an insurable interest in the corporation’s assets, but the sole shareholder does not own the assets of the company. This modifies insurance law, not corporate law. The business owns the assets but the shareholder has an insurable interest in the assets of the company. 3. PIERCING THE CORPORATE VEIL They all turn on individual facts, but cts will not pierce the corporate veil unless there are exceptional circumstances such as fraud or the need to protect innocent third parties, but in respect of contracts they tend to keep legal separate identity. Simple unfairness is not enough to pierce the corporate veil. Categories: allegations of fraud, where the company is an undercapitalized shell, where there is a tort claim against the company, where it is done for tax purposes, where there is a network of parent and subsidiaries operating as a whole entity (enterprise liability / alter ego doctrine), where equity or interests of justice are better served. The court is more willing to pierce the veil where it is tort damages and not contract damages. This has to do with voluntariness of contracting. You should know whether or not the corporation has sufficient assets (a caveat emptor sort of thing). Purely economic loss v. loss from injury. Case Law: Clarkson Co. Ltd. v. Zhelka (1967 Ont. HC): equity will not allow an individual to use a company as a shield for improper conduct or fraud. This maze of corporations was intended to frustrate creditors. VEIL LIFTED Big Bend Hotel Ltd. v. Security Mutual Casualty Co. (1980 BCSC): where the director makes a misrepresentation or omits to disclose it was deemed to be part of the information that the new company ought to have disclosed. Veil will be lifted where there is an attempt to use a corporation for improper conduct. VEIL LIFTED. Rockwell Developments Ltd. v. Newtonbrook Plaza Ltd., (1972 Ont. CA): bad record keeping isn’t enough to get the corporate veil lifted. The shareholders are not liable even though they used their own banks etc. VEIL NOT LIFTED. 642947 Ont. Ltd. v. Fleischer (2001 Ont. CA): when a company is seriously undercapitalized and the parties that set it up intentionally do this the courts will go behind the veil. Especially when you try to fuck around the courts by giving a fraudulent undertaking. VEIL LIFTED. De Salaberry Realties Ltd. v. Minister of National Revenue (1974 Fed. TD) aff’d on appeal: courts may sometimes treat more than one legal corporation as a single legal entity where one has a controlling interest in the others and has integrated their respective affairs. Complicated tax driven structure is a no-go. Company is only an instrument of the parent and grand-parent companies. Income not capital gains. VEIL LIFTED. TEST FROM Smith Stone and Knight Ltd. v. Birmingham Corp. (1939 UK): Suggests exceptions to Salomon arise where corporation is simply an agent of SH. Six part test: - Were profits treated as profits of the parent corporation? - Were people conducting business appointed by parent co? - Was parent corporation head and brain of trading venture? Page 5 Erin Frew CORPORATIONS I - Did Parent Corporation govern the adventure and decide what should be done and what capital should be committed to the venture? - Did Parent Corporation make profits by its skill and direction? - Was parent corporation in effectual and constant control? Alberta Gas Ethylene Co. v. Minister of National Revenue (1989 Fed. TD): Walkovszky v. Carlton, (1966 NYCA): though the shareholder has set up several separate corporations in order to avoid tort liability, this is not illegal, as there is no evidence of these individual corporations acting as an agent of a larger corporation. VEIL NOT LIFTED. Wolfe v. Moir (1969 Alta. SC): if you don’t meet the formalities of incorporation you cannot claim the benefits. VEIL LIFTED. ADGA Systems International Ltd. v. Valcom Ltd. (1999 Ont. CA): Protection is available in some cases to those acting in the best interest of a corporation with parties. In this case however the defendants’ actions were intentional and the only relationship between the corporate parties was as competitors. They are liable because they are intentional tortious actions. Limiting Butt to breach of k cases. VEIL NOT LIFTED. Said v. Butt (1920 KB): an employee is generally not liable for wrongful acts done at the behest of the company if you are acting in good faith. 4. PRE-INCORPORATION CONTRACTS Corporations come into existence on the date and time on the certificate of incorporation from Victoria or Ottawa. This is when it begins its life. But before it is incorporated the directors must appoint officers, issue shares / share certificates, appoint auditors, open bank accounts etc. How do you solve the problem of people entering into contracts with non existent person or someone acting on behalf of a nonexistent person? The problem arises where people want out of the contract or are claiming that the other party has breached it. If the corporation ratifies / adopts contracts entered into before its existence than it assumes responsibility. It can choose not to. Promoters are liable if it was intended that they be parties to the contract. Third party will not be able to enforce the contract personally against the promoters if it was found that they contracted with the corporation rather than the promoter. Can always sue the promoter for the tort of breach of warranty and get damages based on losses suffered. Statute 14: pre-incorporation contract liability: the promoter is personally bound unless the written contract provides otherwise. (2) Corporations may ratify by any action that signals an intention to be bound (4) can expressly exclude personal liability and personal benefits Case Law: Kelner v. Baxter (1866 Common Pleas): where the company doesn’t exist and the company doesn’t take over the contract then you may be bound personally. It turns on the signature line. Here it was signed by the promoter and indicates an intention to be bound. Newborne v. Sensolid (Great Britain) Ltd. (1953 Eng. CA): contrasting position to Kelner. There was never a contract as the non-existent company signed via its agent. The contract was unenforceable despite the intention to be bound by both parties. Black et al. v. Smallwood & Cooper (1966 Aust. HC): the contract was not enforceable against any party personally. The intention of the parties was clear. There was no intention to be personally bound. Suit for specific performance must fail. Wickberg v. Shatsky (1969 BCSC): It was intended that he be employed by the company, nto the individuals that signed the contract. He did have a claim for breach of warranty, but the damages were from the loss and not the breach of warranty so damages for $10. Page 6 Erin Frew CORPORATIONS I Sherwood Design Services Inc. v. 872935 Ont. Ltd. (1998 Ont. CA): Illustrates how even reputable, capable, competent law firms get things wrong in a bad way. A cautionary tale. The letter from the lawyer was unequivocal expression of intent to adopt the pre-incorporation contract. MT using a shell company to carry out a deal that fell through. The other client that inherited the shell company was saddled with liability because of the letter written by the solicitor that ratified the pre-incorporation contract. 5. SHARES AND DEBT SECURITIES Shares and debt securities What is the difference between equity and debt: shares are entitlements to share in profits / dividends and entitlement at wind up (variable return) whereas debts are an entitlement to a fixed amount that has priority over shareholders. Debtors get paid out before shareholders but don’t get to influence the management of the company. Shareholders may lose money or gain money—more risk and more control over the company What is a dividend? They are portions of the profits. The board of directors declares the amount of the dividend then the corporation distributes the dividend. Can be allocated by unanimous shareholder agreement. There is no duty to declare dividends, but the directors have a fiduciary duty to do so. Must exercise powers with a view to the best interest of the corp. Types: cash, in specie (ppt other than cash), and stock Solvency test: sets out two tests (must be met both when the dividend is declared and when it is paid out): 1) liquidity test: whether the corporation will have enough assets convertible to cash to continue to meet its liabilities as they come due; 2) whether the corporation could pay all its liabilities and return all capital contributed by shareholders if the corporation were liquidated (this is based on the realizable value of the corporation’s assets) Statute 42: corp can’t declare dividend if corp would be insolvent or if liabilities would exceed assets (2 part test) 43(1): corp can declare a dividend – cash or more stock. 115(3)(d): restricts decision to declare to directors 122(1)(a): must exercise in the best interest of the corporation in a way that is not oppressive to shareholders or unfairly disregards th interests Page 7 Erin Frew CORPORATIONS I 118(2)(c): directors are personally liable for violating the rules regarding solvency. What is a share? Dfn: a common, divided, participation interest in corporations’ business connected in someway to an investment of money. It is a complex form of personal property. United Fuel Investments Ltd. v. Union Gas Company of Canada (OCA): not an entitlement to specific assets, only a proportionate distribution of the value of those assets Sparling v. Quebec (1988 SCC): A share is a bundle of interrelated rights and liabilities. Including: 1. ***the right to vote for directors of the company 2. the right to look at audit statements 3. the right to vote on fundamental changes in the assets of the company 4. ***the right to dividends: they never have to declare it, but someone has to have the potential to get it (procedural, not substantive) 5. ***the right to receive share of assets on the winding up of the corp (***The three rights must be given to at least one share class) Stokes v. Continental Trust Co. (1906 NYCA) Re Bowater Canadian Ltd. v. R.L. Crain Inc. (1987 Ont. CA) Atco v. Calgary Power Ltd. (1982 SCC) Classes of shares Common v. preferred: generally speaking preferred shares have better rights to dividends or assets on dissolution but do not have voting rights (anything that isn’t a regular old share). Preferred shares are sometimes referred to as senior securities. They may also get super-rights e.g. 10 votes per share or less rights, e.g. nonvoting shares. All the rights of preferred stock must be set out in the corporate charter. It is possible to have more than one class of common shares with different voting rights. Most small corps don’t have different classes of shares. You can create different classes for tax purposes or to attract equity. Issued capital: how many shares are there? Authorized capital: a corp can have a restriction on the maximum number of shares they can have, but they don’t have to. This can deal with the potential for dilution. Directors can issue shares form the authorized capital after incorporation (s. 25). They must set a price per share. They can only issue shares in return for money, property, or past services to a corporation. This ensures fair value / equal price of shares. S. 25(3) allows for compensation for the risk incorporators / promoters take when incorporating Single class structure: s. 24(3). All shares must have the same rights. Rateable distribution: (2. 27(2) if you cannot pay the total dividend entitlement of all the shares in a class, than the shares of all a series share the amount ratably. This heads off discretionary distribution of dividends, and protects what you thought you were investing in. Subscription agreement: contract in which a corporation undertakes to issue shares to subscribers. This is a protective device in corporate law that says you are not bound until the share is fully paid. Stated capital account: once a share is issued the consideration revieced for the share must be entered into the SCA Sparling v. Quebec (Caisse de depot et placement du Quebec), (1988 SCC): shares are a bundle of rights an commensurate obligations. You cannot pick which of these you get to have. Par value shares: used to be more common. It is when shares have a stated face value Discounted Stock: you cannot sell stock for less than FMV as other shareholders and creditors are affected by the dilution of shareholdings by exchange for inadequate capital. Ooregum gold Mining Co. v. Roper, (1892 HL): illustrates the problem of issuing discounted stock. The capital is fixed and certain and every creditor of the company is entitled to look at that capital as his security. The shareholders that bought at discount had to pay the difference into the company. North- West Electric Co. v. Walsh (1898 SCC): adopted the decision in Oooregum into Canada Handley v. Stutz (USA 1891): allows issuance of discount stock Page 8 Erin Frew CORPORATIONS I Response: corporation could issue “no par value” shares or issue shares for non-monetary consideration Watered Stock Watered Stock: arises whenever “no par value” shares are issued for inadequate consideration, whether monetary or non monetary. It amounts to a misrepresentation to future creditors and shareholders as they may be led to overvalue the corp. This also lets one shareholder get proportionally more than they ought to based on their contribution. Hospes v. Northwestern Mfg. & Car Co. USA 1892: The capital of a corporation is the basis of its credit Unacceptable consideration: Some types of consideration are prohibited by statute: promissory notes or promises to pay, non-property assets, and future services (s. 25(3)) S. 118(1) imposes liability on directors that vote for an issue of shares that contravenes s. 25(3) See v. Heppenheimer, (NJ Ct. of Ch. 1905): prospective profits are not property. The test is whether they would be willing to pay that amount in cash for the property. Remedy: corporation can sue directors, shareholder can sue (derivative action on behalf of the company), creditors might be able to sue, but hard to prove quantum of loss. Rights on Liquidation International Power Co. v. McMaster University (1946 SCC): Preferred shareholders are entitled to similar benefit to assets as are common shareholders. Rights of all shareholders are on the basis of equality unless otherwise stipulate in bylaws. Priorities listed in bylaw are in addition to already existing common law rights and do not wholly demarcate the rights of the shares. The right to dividends is distinct from the rights to assets. Default was that common and preferred were the same except where differences explicitly set out. Convertible Securities Rights and Warrants conversion: exchanging securities of one class for securities of a different class. The privilege of conversion is inextricably associated with the share and a transfer of the latter includes the transfer of the former. The holder of a conversion privilege has none of the rights of a stockholder until and unless he complies with the terms and conditions of the contract. A warrant is similar to a convertible security, except the warrant is exercised by a payment of cash. options to acquire shares for a cash consideration. If the warrants are issued with a debt security and “attached”, then they cannot be sold separately. However, detachable ones also exist. There are conversion rights that can be executed by holders of certain types of securities—security-holder is not a shareholder until conversion. rights: options to purchase shares that a re usually offered to existing shareholders at current market value on a pro rata basis (382) Closely held corps. and distributing corps Closely held corporations have fewer shareholders. For these corporations there may be governance mechanisms that are not practical for larger corporations. It is common to have restrictions on shareholders. The articles may have restrictions like transfers must be approved. You know what the directors are doing because you are one. The courts are generally reluctant to interfere with shareholders in closely held corps. They are not worried about the public being defrauded. Five types of share restrictions: 1. absolute restrictions: SH can’t sell (rarely used) 2. consent restrictions: SH can sell on approval of corp’s board. 3. first option restrictions: most common – must offer to remaining SH first. 4. buy-sell agts: a triggering transaction (death, deadlock) would activate provision that corp or other SH must purchase shares. 5. buyback rights: corp given right to repurchase shares on triggering event even if SH does not want to sell. Page 9 Erin Frew CORPORATIONS I Differences in governance: you don’t have to give formal notice of meetings if all the shareholders attend. You don’t have to have shareholder meetings if you sign written resolutions. You don’t need an auditor. You don’t have to have publically funded financial statements if you are closely held Re Barsh and Feldman (1986 Ont. HC): illustration of the courts reluctance to intervene. The court will not order a meeting where it is a certainty that one shareholder will be outvoted. Ringuet v. Bergeron (1960 SCC): the power of the directors to manage is subject to any provisions in a unanimous shareholders agreement. Can expressly transfer responsibility in response to this case. Where there is a unanimous shareholder agreement, just buying the shares doesn’t bind you to the agreement. BUT such an agreement between shareholders owning or proposing to own majority of issued shares to unite upon a course or policy is not illegal or contrary to public policy. Agreement is enforceable. S. 102 CBCA permits directors discretion to be transferred to the shareholders S. 137 BCBA says that directors duties may be transferred via the articles / bylaws corporate finance 6: what must be in the articles, incl share structure (can put restrictions too). 24: shares, rights attached to shares (ie voting), consideration, prohibits par value shares. 25: issue of shares - director’s resolution 25(3) can’t be for less than $ value if property, eg. (watered stock) – remedy 118(1). 27: articles may authorize issue of any class of shares. 27(3): no priority of dividend payment for new classes over old series of shares in same class. 28: if articles provide, shareholders of class of new issue have pre-emptive right to buy offered shares 189(1): Directors can borrow on credit of corp without SH authorization. 189(2): Directors can delegate this borrowing power to officers. shareholders 103(2): ratify changes to bylaws. 106(3): elect directors by ordinary resolution at each annual meeting. 109: may remove directors by ordinary resolution at a special meeting, and may fill that vacancy. 137: can submit proposal notice of a matter the SH wants to raise at mtg (resolution). 137(4): can submit proposal to nominate directors if signed by 5% of voting SH. 140: unless otherwise stated, each SH must have one vote. 143: 5% of SH may requisition SH meeting for stated purpose, dir must comply (3). 146(1): unanimous SH agt can take over powers from directors. 146(3): purchaser of shares subject to unanim SH agt deemed to be party to agt. 146(5): if SH elect to manage co, they have same liabilities as directors would have. 148: may appoint another person to represent the SH at meeting and vote their shares. 150(1) right to send a dissident proxy circular. 153: duties of intermediary. 162: approve auditor 173(1): changing articles must be approved by special SH resolution. 189(3): sale, lease or exchange of substantially all assets require SH approval (special res). 190: right to dissent, appraisal and payment for shares by corp, procedure to do this. 206: in a takeover, if 90% of non-majority SH have agreed to sell, majority SH can compel acquisition of rest. 211(7)(d): shareholders only get stuff after all secured and unsecured obligations met. meetings 144: court can order SH meeting close corps 49(8): restrictions on shares not effective against transferees unless actual notice or notice on cert. 136: shareholder may waive notice of meeting of SH in any manner 139(4): if corp has only one SH, that is quorum (in person or by proxy). 142: resolution can be made if unanimous amongst SH in writing instead of at meeting 146(1): unanimous SH agt can take over powers from director. Page 10 Erin Frew CORPORATIONS I 146(2): if only one SH, makes written declaration restricting powers of directors, deemed to be unan. 146(3): purchaser of shares subject to unanim SH agt deemed to be party to agt. 149(2): dir not required to send proxy form if not public or has <50 SH. 163: corps not public don’t need auditor (unanimous SH resolution required). 6. DIRECTORS’ DUTIES AND SHAREHOLDER REMEDIES Ultra Vires Doctrine A rule that a corporation has no legal capacity to act in any fashion not specifically authorized by the incorporating documents. IF the company does something beyond the scope of its powers the act is a nullity. To avoid this, add an objects clause that is sort of an et cetera bin. Ashbury Ry. Carriage & Iron Co. v. Riche (1875), LR 7 HL 65 HL): construction of a railway was outside the objects of the corporation. The activity was ultra vires, the company may not pursue it and the contract is unenforceable. Abolished: s. 15, they can do anything they want … Unless: s. 16 unless it is restricted by its articles Director Management: The Indoor Management Rule / Ostensible Authority Generally speaking we don’t expect third parties to carry out detailed investigation into authority of directors acting in the ordinary course of business. S 18 is a codification of the indoor management rules. Sherwood Design: didn’t matter if you didn’t pass the resolution the indoor management rule applies. Does not protect those with constructive knowledge. You can put restrictions into the articles (s. 6(1)(f)): restrict activities of management, protect your investment, protect creditors’ interests. Royal British Bank v. Turquand (1856 Ex.): when an outsider dealing with a corporation satisfies himself that the transaction is valid on its face to bind the corporation, he need not inquire as to whether all of the preconditions to validity that the corporation’s internal law might call for have in fact been satisfied Sherwood Design Services Inc. v. 872935 Ont. Ltd. (1998 Ont.CA): the indoor management rule combined with adoption of pre-incorporation contract. Innocent third parties are entitled to rely on appearance of authority. Directors’ duties and liabilities: Directors call annual meetings and special meetings. The shareholders (5%+) can ask that meetings be held and the court can step in if the directors don’t comply with the request. Directors can also apply for court ordered meetings. Practically the directors will probably be shareholders and can rely on that status. Types of Votes / Meetings s. 173 requires approval for fundamental changes of the articles s. 176 when special class votes or series votes are required (when a resolution affects one class of shareholders) s. 183: special resolution to approve an amalgamation with another corporation s. 144 the court can order a meeting where the shareholders apply, no minimum. The courts will decline where the meeting would not be properly held or in closely held corporations where the communications between shareholders are really bad. Special resolutions and shareholder ratification: certain corporate transactions require ratification by the shareholders as a condition of their validity. A special resolution requires a majority of not less than 2/3 of the votes cast by the shareholders that voted in respect of that resolution. Required for: amendment to articles (s.173); creating and amending bylaws (s. 103); amalgamations (s. 183(3)); continuing in another jurisdiction(s. 188); liquidation or dissolution (211); and sales of substantially all the assets (s. 189(6)) ordinary resolutions: are passed by a simple majority of the votes cast Page 11 Erin Frew CORPORATIONS I Re Marshall (1981 Ont. HC): the role of a chair conducting the meeting. The issues that arise with who is responsible for voting to determine who is entitled to vote. Here there is a conflict of interest between the interest of the chair and the running of the meeting. Unanimous SH agt (USA) can override the directors’ power to manage corp (CBCA 102(1)) and give it to the SH (s. 146). more common in closely held corps (would be too difficult to get unanimity in lg corps) Conduct of Meetings: Blair v. Consolidated Enfield Corp. (1993 Ont. CA): looking at proxies and the role of the chair in determining the validity of the proxies in a conflict of interest. Legal advice is one factor to be taken into account. There are limits as to how far the chair has to go. He doesn’t have to go behind the register. He just has to make sure that only registered shareholders are voting and that proxies are done properly. The rights of the chairs to deal with disputed matters of proceedings Re Canadian Javelin Ltd. (1976 Que SC): circumstances where a court ordered meeting is the only way out of the mess. Charlebois v. Bienvenu (1968 Ont. CA): what else can they do at a court ordered meeting. Court ordered meetings are about the process of the meeting not the powers of the shareholders at the meeting. You can not get around limitations on shareholder power by getting the court to hold a meeting. Shareholder Voting Rights: Automatic Self-Cleansing Filter Syndicate Co. v. Cunninghame (1906 Eng. CA): directors are responsible for managing the company (102) and if the shareholders want change they need to do things through special resolution, not try to manage the corporation through ordinary resolutions. Jacobsen v. United Canso Oil & Gas Ltd. (1980 Alta. QB): s. 6(3) allows articles to set a higher requirement for votes than the statute. BUT s. 24(3) says that where a corporation only has one class of shares all the holders rights are equal. And s. 140 says that unless the articles provide otherwise each shareholder is entitled to a vote/ share. The Bylaw cap contravenes the CBCA The Queen v. McClurg (1990 SCC) Corporate Governance and Corporate Social Responsibility corporate governance: the structure by which corporate decisions are made so that capital can be raised casteffectively, assets are used in the efficient generation of wealth and with a view to sustainability of the corporation, and corporate decision-makers are held accountable to those who have direct investments in the firm “Directors and officers have an obligation, in exercising their duties, to act honestly and in good faith with a view to the best interests of the corporation, and to exercise the care, diligence, and skill and a reasonably prudent person would exercise in verbal circumstances.” shareholder apathy is rational where there is a large and dispersed group of shareholders because their individual small stakes in the Corporation make the gains from monitoring relatively small to the costs (48) whose interests directors and senior management should have in mind when they‘re acting in the best interest of the corp. It depends on all the circumstances. Sometimes some interests are more pressing than others. It is more than just the interests of the shareholders. The shareholders’ interests are not the same as the companies’ interests. Dodge v. Ford Motor Company (1919 Mich): Suggests that directors were operating improperly if the decision on pricing was made in the public interest and not the shareholder interests. Courts of equity will not interfere in the management of the directors unless they are guilty of fraud or misappropriation of corporate funds, or refuse to declare a dividend when such refusal would amount to an abuse of discretion as would constitute a fraud, or a breach of good faith towards the stock holders. The directors must justify their decision not to declare a dividend. The corporation works for the shareholders not for the primary purpse of benefiting others. peoples v. wise: it may be legit for the directors to consider not just the interest of shareholders but depending on the circumstances the interests of employees suppliers ,creditors, consumers, government, environment Revlon : duties of directors in takeover. When in Revlon mode there is a narrower focus. When it is clear there is an auction you can still take into account other constituencies’ but more of a focus on shareholders and the interest of others should be rationally connected to those of the shareholders. Different in the US because they have a different regulatory approach to takeover bids. More of a focus on maximizing the returns to shareholders. Not inconsistent with Peoples v. Wise because it varies with the circumstances Unical: duties of directors in takeover Page 12 Erin Frew CORPORATIONS I Shareholder remedies S. 102: directors have power to manage the company subject to any unanimous shareholder agreement…what do these involve Director’s Duties Two distinct duties to be disturbed by directors and officers per s.122(1): - fiduciary duty (to act honestly and in good faith with a view to the best interests of the corporation); - duty of care (521) Fiduciary duty to act honestly with a view to the best interest of the co and to avoid conflict of interests Peoples Department Stores Ltd. Inc. (Trustee of) v. Wise (2004 SCC): breaches require more than just being negligent. It is about honesty and dishonesty. The fiduciary duty is owed to the corporation and not specifically to the shareholders, creditors, or any other group. Content of the duty: - respect the corporation’s trust and confidence in managing assets; - avoid conflicts of interest with the Corporation; - avoid abusing their position for personal benefit; - maintain confidentiality of information (521) Standard is the reasonably prudent person in comparable circumstances. Business judgment rule: meeting the requirements of this duty of care as long as you select from a range of reasonable options Nielsen Estate v. Epton (2006 Alta. QB) aff’d by Alta CA: directors owe a duty of care. To the corporation and to the employees of the corporation. Corporate directors have a personal duty of care in the following circumstances: (1) Director has or ought to have personal factual awareness of a serious and avoidable or reducible danger to which employees are exposed in relation to corporation-related activities; (2) it is within the authority of the director to envision, establish and enforce corporate policies which could reasonably avoid or reduce such serious danger; and, (3) it is within the reasonable capacity of the director to envision, establish and enforce the actions necessary to carry out such policies and to reasonably avoid or reduce such serious danger (530) Defence: Directors also have an obligation to dissent where they do not agree with board decisions; and recording of such dissent may act as a liability shield for the director in a personal capacity in some circumstances Bushell v. Faith (1970 HL): The mischief Parliament was attempting to avoid was the practice that a director should be irremovable or only removable by an extraordinary resolution. Parliament never sought to fetter the right of the company to issue a share with such rights or restrictions it desires. There is no indication that Parliament sought that every share that is entitled to vote should be deprived of its special rights under the articles. Business Judgment Rule: When the court is assessing how the directors operate they keep in mind the “business judgment rule” that says that directors and officers are entitled to choose from a range of reasonable options. Judges are cognizant of the fact that they are not experts in the business and so give deference to the directors. Also the courts recognize that there is rarely just one option to choose…the courts acknowledge that directors do not have to be perfect. They don’t have to choose the successful action--they pay price in other ways. They can’t do anything they want, i.e. they cannot chose an unreasonable option Peoples Department Stores Inc. (Trustee of) v. Wise (2004 SCC): the definitive statement on the BJR. meeting the requirements of this duty of care as long as you select from a range of reasonable option. Bad Director, Bad! Shirking: if the directors don’t take their duties seriously. The common law standard is low and is the test from Re Brazilian Rubber: The directors of the company regarded it as pleasant employment without responsibility. The directors issued a prospectus with some big errors. There is no special requirement to be a director. We will only expect what is reasonable gibven your education and background. The Dickerson report recommended this standard be raised. The duty is now higher than common law. You don’t have to be perfect but must be a Page 13 Erin Frew CORPORATIONS I reasonably prudent person in the present circumstances. Shirking may manifest itself in a failure to know what’s going on. You must go to meetings. You must give stuff adequate consideration and thought. Barnes v. Andrews (1924 USDC SDNY): It wasn’t a failure to not attend the meetings, but he was responsible for some of the problems of the company because he had failed in his general duty to stay advised of the general goings on of the company. He had a duty to keep himself informed—just talking to the president wasn’t enough because he should have actually looked for some detailed information—he should have known that the friend was just giving a superficial account of how things were going. He was in breach of his duties, but then the court goes on to say that there was no loss shown by the plaintiff Peoples Department Stores Inc. (Trustee of) v. Wise (2004 SCC): trustee was suing the directors saying that they failed in their duty. The court considered in whether the directors have met the standard of care the courts will apply the business judgment rule. If they acted prudently and on a reasonably informed basis then they are fine. Peoples Department Stores Inc. (Trustee of) v. Wise (2004 SCC): The court concluded that there was a whole range of factors that led to the bankruptcy not everything could be linked to the joint inventory thing. The court finds that where you cannot point to the loss being attributable to the failure of the directors then there is an issue. They were not entitled to rely on the unaccredited professional’s advice. Defences to Shirking: reliance on senior officers, reliance on professional advisor, the reliance is reasonable (it is not enough to rely on someone that merely knows more than you do) UPM-Kymmene Corp v. UPM-Kymmene Miramichi Inc. (2002 Ont. SCJ): Illustrates that it’s not just the status of the advisor, but also the directors have to be mindful of the circumstances in which the opinion was rendered. The board tried to rely on the business judgment rule. The court would have let them had they actually used their judgment. There was a total failure to consider the facts. Smith v. Van Gorkom (1985 Del. SC): a US case looking at the extent to which directors can rely on the business judgment rule in approving a merger proposal. You cannot rely on the business judgment rule where you are grossly negligent. They made a hasty ill-informed decision. Couldn’t say they relied in good faith on the officers because the officers had not been directed to carry out the proper investigation by the board. Globus v. Law Research Service Inc.: the director has to be indemnified where the director was acting in another capacity and if there are no personal guarantees. Indemnification is popular for medium firms. Looting: extracting wealth from the company. Taking assets or opportunities that are the companies and taking them as your own. Concerned about conflicts of interest. Aberdeen Ry. Co. v. Blaikie Brothers (1854 HL) North-West Transportation co. v. Beatty (1887 JCPC): which shareholders get to elect the director. There just needed to be a simple majority because it would be to disregard the majority and allow the minority shareholders to have the say…against regular corporation organization. It isn’t practical to have to go through all the shareholders and decide which ones are allowed to vote and which ones can’t Safe Harbour for Interested Contracts S. 120: if you make written disclosure of your interest, the contract is approved by disinterested majority, and the contract was reasonable in fair you can have your conflicty contract UPM-Kymmene Corp v. UPM-Kymmene Miramichi Inc.: Gray v. New Augarita Porcupine Mines Ltd: If it is material to their judgment that they should know not merely that he has an interest, but what it is and how far it goes, then he must see to it that they are informed. It is no answer to the duty to disclose to say the directors could have discovered this for themselves. The duty to disclose is an absolute one, because, without full disclosure, any investigation into whether the beneficiary would have acted in the same manner is impossible Regal (Hastings) Ltd. v. Gulliver (1942 HL): it doesn’t matter how honest your actions are if the opportunity came to you as a result of the role as director, you cannot take it. Test: Fiduciary relationship + advantage by way of the relationship = breach! Peso Silver Mines Ltd. v. Cropper (1966 SCC): illustrates an attempt to apply the principle in Regal and make a similar claim in the Canadian mining context. Here the company had rejected the offer and the issue had already passed out of his mind, when the offer was made to him. He chose to take the risk personally and he should be entitled to the reward. Are you profiting as a result of the fiduciary relationship / by reason of being a director and in execution of your office OR on your own. Page 14 Erin Frew CORPORATIONS I Canadian Aero Service Ltd. v. O’Malley (1974 SCC): it still applies to senior management even where you resign before taking the offer. Here this was direct competition for the opportunity. General principle is to avoid conflict but there is no exhaustive check list to avoiding breaches of fiduciary duty. Broadens the Peso test. Johnston v. Greene (1956 Del SC): the opportunity belongs to him as it was his opportunities not the companies. If he had a duty to pass along the opportunity which one of the many corporations he was director on would he pass it to? Ratification and Derivative Actions: Ratification: a process by which the contracts entered into where a director has an interest may be approved by the shareholders has a basis in the rights of individuals to bring derivative actions against the company Derivative action allows a shareholder to sue in respect of a wrong done to the company. They bring the action on behalf of the company even if they are a minority stakeholder. There are four types of derivative actions: - Ultra vires transactions - Actions which require a special majority - Actions which contravene the personal rights of shareholders - Fraud on the minority Statutory Derivative Action The statute expands it from Foss v. Harbottle (shareholders against directors- fraud on the minority). The CBCA allows it to be brought by more people (part XX: registered or beneficial holder or past shareholder or affiliate, former or current directors and officers, directors, any other person the ct deems appropriate) but requires leave of the court. The court must consider (s. 239(2): notice of directors of intention to bring, complainants are acting in good faith, it is to the advantage of the corp or a subsidiary. Primex Investments Ltd. v. Northwest Sports Enterprises Ltd. (1995 BCSC): the directors refused to bring an action without giving reasons. If an action is in the best interest of a corp the directors should pursue it. The decision was not impartial. Shareholder ratification may not be determinative of what is the best interest of the company. Re Northwest Forrest Products Ltd. (1975 BCSC): shareholder ratification will not be overly persuasive because the misdeed was carried out at the behest of the majority shareholder. Auerbach v. Bennett: the role of the board in derivative actions. The company created a special litigation committee. This was good procedure. The decision is protected by the BJR. The ultimate decision to litigate is within the scope of the Rule. The court will supervise the process, but not the result Zapata Corp. v. Maldonado: another case in which the corp makes a decision that they are not going to pursue an action but have it dismissed. Allegation that the directors had manipulated the exercise date of some options so that the value would be affected to provide favourable tax benefits to them at the expense of the company. Two step test: inquire as to independence and then apply cts own judgment. Even if the company acts in good faith it is still up to the court to say if the litigation is within the best interest of the company. Personal Actions Sometimes there is a personal wrong to an individual shareholder. The biggest reason to try to bring a personal action is you don’t require leave of the court Jones v. H.F. Ahmanson & Co.: discusses the distinction between personal and derivative. Can bring where the act was not a wrong to the corp but to you. It doesn’t matter that a lot of other shareholders had personal claims too. There can also be a wrong to the company too, a personal action doesn’t preclude it. Corporate Actions Abbey Glen Property Corp. v. Stumborg: deals with a claim for unjust enrichment. Where the wrong is done to the company the remedy is compensation to the corporation itself not the shareholders. duty of care isn’t in law to those shareholders it was an obligation to the company and the company has an existence beyond the shareholders Oppression Remedies Page 15 Erin Frew CORPORATIONS I Oppression remedy: courts have ability to step in for shareholders in the interest of the corporation. It is a Canadian thing. The complainant is the same test for derivative actions OR is set out in s. 241. It is about claiming your interest as a shareholder have been unfairly disregarded and the conduct has been unfairly prejudicial. You must show more than just suffering some loss, but some oppressive or unfair conduct. Key questions: Application of business judgment rule: Were the directors acting in a range of reasonable options? AND Reasonable expectations of the individual: What were your reasonable expectations? If you are trying to seek some befit, protection, status that is unreasonable the ct will not assist you? Clitheroe v. Hydro One Inc. (2002 Ont. SCJ): The oppression must relate to your status. You can’t use it as a way of bringing a wrongful dismissal case. Not every grievance you have as a shareholder is subject to an oppression remedy. must show you suffered disadvantage because you are a shareholder. First Edmonton Place Ltd. v. 315888 Alberta Ltd. (1988 Alta QB): proper person. Bad lawyers. The law doesn’t stop the company from doing things that prejudice their interests it just stops the company if they are unfairly prejudiced. They were not creditors at the time of the wrongful act. A creditor is not someone with a claim to unliquidated damages Downtown Eatery (1993) Ltd. v. Ontario (2001 Ont. CA): Oppression remedy for a creditor. They effectively killed the defendant through a corporate reorganization. Because the company went out of business and all its assets were transferred…the result was the same that he was unfairly prejudiced West v. Edson Packaging Machinery Ltd. (1993 Ont. Gen. Div): Practically it was all part of the same package. It was a connected claim because they were supposed to buy these shares to show support. it wasn’t just a wrongful dismissal claim there was some expectations to do with the fact they are shareholders, not just in relation to their status as employees. Scottish Co-operative Wholesale Society Ltd. v. Meyer (1959 HL): Illustrates a claim based on a breach of fiduciary obligation by the directors of the company. Inaction can constitute oppression. Linked to the idea of reasonable expectations. The company has been damaged by the acts of the directors. since the nominee directors failed to protect the better remedy is to have the majority shareholder buy them out at the price before the oppressive conduct occurred Re Ferguson and Imax Systems Corp (1983 Ont CA): Expectations and obligations may be tied up with matters that are personal rather than just corporate Naneff v. Con-Crete Holdings Ltd. (1993 Ont. Gen. Div.): Family Business with undesirable woman. You can’t ignore your corporate obligations just because he’s your son. Where family expectations aren’t overlooked is in determining the remedy. You can’t all work together, so you buy the company Naneff v. Con-Crete Holdings Ltd. (1994 Ont CA): alters the remedy. He knew right from the start dad was in charge. Buy out the son. It is a family business and your expectations are not appropriate. Directors’ Defence S. 123: RElinace on professionals: Peoples v. Wise: it doesn’t count if you are relying on an unaccredited professional. Liabiliyt Insurance. S. 124: Indemnity of directrors: director must be acting honestly in good faith with a view to the best interest of the company Blair and Consolidated Enfield: can the director be indemnified in deciding proxies Blair: It was okay to make the wrong decision because he was acting in good faith and relying on legal advice. Not a question of getting it right but acting in good faith or bad faith Statute directors duties and powers 102(1): directors shall manage or supervise management of business of corp. (incl pwr to declare dividends) 122(1)(a): fiduciary duty/ duty of loyalty, with view to best interests of the corp 122(1)(b): standard of care, care diligence and skill of reas prudent person in comparable circumstance 122(2): directors must comply with these duties. 122(3): and cannot be relieved of the duties. 25: directors can issue shares 43: directors can declare dividend 103: create and amend bylaws Page 16 Erin Frew CORPORATIONS I 105: qualifications of directors (incl residency concerns). 106(8): directors may appoint director to fill vacancy until the next AGM. 108: director ceases to hold office. 111(1) can fill vacancies on board if interim vacancy 115: directors can delegate to committee director powers except certain core duties. 116: even if defect in election, act of director or officer valid. (there is a distinction between no appointment and a defective appoi Morris v. Kanssen 1946) 120(1): must disclose to corp any interests in material K or transactions to which they are a party. 120(7): interested director K not void if disclosure requirements complied with. 120(5) director in most circumstances should not vot on an interested K. 121: directors can appoint officers. 133: can call special meetings of SH. 135: must call an AGM and send notice to SH. 149: must send proxy forms when giving notice for SH meeting (+ 50 SH) 189(1): Directors can borrow on credit of corp without SH authorization. 189(2): Directors can delegate this borrowing power to officers. 189(3): sale, lease or exchange of substantially all assets does require SH approval (sp res). directors liability 42: directors can’t declare dividen if it would make it go insolvent. 116: even if defect in election, act of director or officer valid. 118(1) and (2): liability of directors for mischief re: issuing shares without receiving full payment for them /dividends 118(6): defence to 118(1) and (2): if director did not and could not reasonably have known 119: liability of directors for unpaid wages if corp can’t pay. Position, not fault, based provision. Six months of unpaid wages. Prov there is also liability for unpaid compensation to staff by directors. 123: director is deemed to have consented to resolution unless formally dissents (absolves liability) 123(4): reasonable diligence defence: director not liable under 118 or 119 and has complied with 122(2) if exercised reasonable care and skill and relied in good faith on (a) or (b). 123(5): good faith defence: director complied with 122(1) duties if relied in good faith on (a) or (b). 124: indemnification of directors, advance of costs, insurance 124(3): limits to indemnification (must have acted in good faith, though conduct lawful). 125: can set their own renumeration. third parties 17: parties not deemed to have notice or knowledge of docs just bec filed with Director. 18(1) Indoor management rule. Takes burden off third parties to establish a party has authority. 42: creditor interests come before SH claim on dividends. 116: act of director or officer valid despite irregularity in election or appointment. 211(7): creditors will get notice upon intent to dissolve. remedies 118(4) and (5): court may order remedies re: improper share/dividend issues. 120(8): interested K – court can set aside and order accounting for profits. 144: court can order SH meeting 190: dissent and appraisal rights 214: court may order dissolution if, for one, USA not complied with. 239: derivative action. 241: oppression remedy. 247: court may make restraining or compliance order if Act, articles, bylaws, USA not complied with. 17: No Constructive Notice: no person is affected by or is deemed to have notice or knowledge of the contents of a document concerning a corporation by reason only that the document has been field by the Director. Page 17 Erin Frew CORPORATIONS I 18: authorities of directors, officers and agents: (d) indoor management rule: a person held out by a corporation as a director, an officer or an agent of the corp has not been duly appointed or has no authority to exercise the powers and perform the duties that are customary in the business of the corporation or usual for a director, officer or agent. 116: validity of directors 7. MERGERS & ACQUISITIONS Sales of all or substantially all of the assets of the co 189(3): requires 2/3 votes. Prevents abuse of minority shareholders. Something that so fundamentally changes what they are doing that it is as serious as winding up a company. If it is a publically owned company certain information must be sent out and the meeting must be conducted in a specific way. Cogeco Cable Inc. v. CFCF Inc. (1996 Que CA): qualitative (75%- can measure using book value, contribution to gross revenue, or effect on net income) and quantitative test (list on p 971). The issue is whether it strikes at the heart of the corporate business. There is no automatic rule Amalgamation Arranging two companies to combine to form one new company which legally continues to have the assets and liabilities of both subsumed corps. Short form: if they are both wholly owned by the same person. Doesn’t require votes or paperwork Long form(?): if they are not part of the same family already. Both sets of shareholders must pass special resolutions approving the amalgamation. There will be securities issues if it is publically traded. The effect is the same as the short form. R. v. Black and Decker Mfg. Co.: like a river formed by the confluence of two streams. There may be reasons to do this: tax, business licence transfer, charitable status, assets that cannot be transferred or the transfer has consequences. Even criminal liability survives amalgamation. “and sins if sinners they be” Plan of Arrangement Under s 122, can get a court approved plan to do it. Will be complex with lots of court monitoring The Appraisal Remedy s. 190 for certain kinds of fundamental transactions where some shareholders do not vote. There is an exit strategy to have their shares bought out at FMV. Process: Send demand of payment, return shares, and 30 days to accept an offer Valuing shares: four methods: market value, asset value, earning value, some combo. Courts sometimes give a premium on the shares for the forcible taking. Buyouts and Going Private s. 206: requires 90% shareholder approval to get rid of the other ones going from widely held to closely held Neonex International Ltd. v. Kolasa (1978 BCSC): The judge takes a cautious view of how the CBCA made it easier for majority shareholders to get rid of minority shareholders: allowed for amalgamation even thought the dissenters could have stopped it. Allows the majority to get around the 90% requirement by going through the amalgamation provisions instead. The CBCA made it easier to remove dissenting shareholders so the court will tend to be sympathetic to the dissenters because they are having their property expropriated against their will. it is up to the company to establish the fair value Takeover Bids Two ways: proxy battle and takeover bid. Takeover rules under securities law apply when transaction will result in one shareholder with more than 20 % of the copr as this gives effective control. Process is that you start the takeover bid by mailing an offer to all the shareholders of a class with a circular that sets out the information. It is required to stay open for 35d. If some offer than they must be taken pro rata. Page 18 Erin Frew CORPORATIONS I Defensive tactics Teck Corp. v. Millar (1972 BCSC): The corporations interest are not synonymous with the majority shareholders and it is okay for the directors to prefer one bid to another as long as they are acting with the best interest of the corporation must have a reasonable ground for believing it to be in the best interests. The leading case on takeovers, has been widely followed. Defensive Share Repurchase: Unocal Corp. v. Mesa Petroleum Co. (1985 Del. SC): Directors are entitled to the protection of the business judgment rule in a takeover situation. it was legitimate to regard this as a threat and they were entitled to resist it. Protecting the shareholders by defeating the inadequate offer or preventing the ones who are stuck with shares from having to accept junk bonds. You couldn’t carry out the valid purpose without excluding M. An exception to the rule that you have to treat shareholders in the same class the same. The selective response is generally to the greenmailers, but this one is to defeat the greenmailers. Given the nature of the threat posed the response is not unlawful or unreasonable. Test: must show there is a threat, show use of independent committee, show proportionality. Due Care Requirement: Revlon Inc. v. MacAndrews & Forbes Holdings Inc. (1986 Del SC): They have a duty to get the best price It might be okay where there are two bidders to prefer one over the other. Why was it not okay to prefer F to P? Because the bids were essentially the same (not like Teck v. Placer where one had a better reputation). The lock up was based on something more than maximization of shareholder profit so it was wrong to adopt measures that ended the auction. Once it is clear the company is going to be sold try to get the highest price. Maple Leaf Foods Inc. v. Schneider Corp. (1998 Ont. CA): Directors duty where there is a hostile takeover bid and preference by majority shareholders to deal with someone else. The recommendation of the special committee was not subject to challenge. S didn’t want to sell because of their personal interests; they preferred the bid of Greenfield as they wanted to keep long-term employees etc. This was a legit concern to take into account. The board didn’t have to auction even though it was in Revlon mode. Just Say NO! Paramount Communications Inc. v. Time Inc. (1989 Del. Ch): agreed in result and didn’t think it was wise to focus on timescale as an issue, but is more of a responsibility of the board of directors. if not in Revlon mode they are in no obligation to maximize short term share price, rather the timeframe is theirs to determine. This picks up on a notion of corporate culture. Poison Pill in Canada: 347883 Alberta Ltd. v. Producers Pipelines Inc. (1991 Sask. CA): They were acting beyond their powers and the plaintiff was entitled to the oppression remedy so he set aside the pp and the numbered co could make a takeover bid and the shareholders could make a choice between the two bids ~EXEUNT OMNES~ Page 19 Erin Frew