Environmental Disclosure: Evidence from Newsweek's

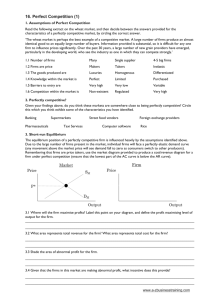

advertisement