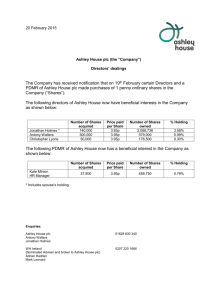

Annual Report 2011

advertisement