Q2 2013

Oxford Communiqué Investor Report:

Why the World’s Most Profitable

Energy Stock is About to Triple

By The Oxford Club Research Team

NOTE: The Oxford Club is not a broker, dealer or licensed investment advisor. No person listed here should be

considered as permitted to engage in rendering personalized investment, legal or other professional advice as an

agent of The Oxford Club. The Oxford Club does not receive any compensation for these services. Additionally, any

individual services rendered to The Oxford Club members by those mentioned are considered completely separate

from and outside the scope of services offered by The Oxford Club. Therefore if you choose to contact anyone listed

here, such contact, as well as, any resulting relationship, is strictly between you and the Pillar One service.

105 West Monument Street | Baltimore, Maryland | 21201 | 410.864.1751

Oxford Communiqué Investor Report: Why the World’s Most Profitable...

A certain energy company – one we estimate not one in 20,000 Americans can even name – is

about to make a major announcement that we believe will triple its stock price.

The company is nearly 12 times more profitable than Toyota… three times more profitable than

Wal-Mart… four times more profitable than ConocoPhillips. It’s more profitable than Royal

Dutch Shell, Exxon Mobil, BP and Chevron. And we’re talking bottom line profits here, not

growth rate.

Furthermore, this company manages to make more money than all these industry giants, on just

a fraction of the revenues.

And when you look at its business, it’s easy to see why…

The Czar of Russian Energy

That company is Gazprom (OTC: OGZPY) (LSE: 81JK.L), which owns 60% of Russia’s gas

reserves. Based in Moscow in the Russian Federation, the company was founded in 1993. Along

with its subsidiaries, Gazprom is in the exploration, transportation, production, storage and sale

of oil and gas. It is the biggest company in Russia and one of the largest in the world…

It operates more than 6,988 wells producing natural gas, with reserves worth an astonishing $299

billion. It runs 6,151 oil-producing wells and owns the largest gas transportation network in the

world. And its installed and operates 81 power facilities generating 37 GigaWatts of power. That

is enough power to service around 37 million homes.

Currently Gazprom generates 17% of Russia’s power. It exports more natural gas to Europe than

any other company… And it owns nearly a fifth of all worldwide supplies of natural gas.

On top of that, it just rewarded shareholders with by far the biggest dividend increase in

company history. In 2012, it increased its dividend 110% compared to what it paid out to

shareholders in 2011. And its three-year dividend growth rate clocks in at over 207%.

But here’s the interesting part…

For one specific and very unusual reason, Gazprom currently trades at one third of the valuation

of its competitors. Despite making more money than all of them, its P/E is currently 2.85 while

the industry average is well over 9.

Plus, Gazprom is a virtual baby in the energy business. Its founding was just 20 years ago. By

comparison, Exxon Mobil’s origins go back nearly 150 years.

But while Exxon Mobil, Royal Dutch Shell, BP, and others enjoy the benefit of a major head

start, things have changed dramatically over the last few years. In 2012, Gazprom’s oil exploration

2

Oxford Communiqué Investor Report: Why the World’s Most Profitable...

budget alone jumped to $6.1 billion. And it will increase to $23 billion over the next three years.

It operates gas and oil exploration projects in the United Kingdom, Vietnam, Bolivia, Russia,

Algeria, Kuwait and more.

As a result, it’s set record highs for increases in gas reserves. Currently Gazprom controls 18% of

the global natural gas supply. That’s approximately 35.6 trillion cubic meters, valued at around

$300 billion. Its largest plant has produced ten million tons of LNG (liquid natural gas) in each

of the last two years.

And there is a huge market for the fuels it’s producing…

The company holds major sales contracts to deliver LNG to Japan, India, Germany, Thailand,

the UAE, China, Taiwan, Italy, Korea and France. It shipped over two million tons to Japan and

Korea alone. And it operates the world’s largest gas transportation system with over 164,000 km

of pipeline and shipping operations spanning the globe.

But even this is just a small sampling of everything this company has lined up for future

expansion…

It’s already activated more than 80 power stations producing 37 GW of power throughout

Europe. It’s got a blockbuster deal in the works with China. It’s currently co-developing 17

trillion cubic feet of gas in Israel’s massive Leviathon gas field.

In other words, it is well on its way to achieving its ultimate goal as stated by the company

Chairman:

“To become the strongest company in the world’s energy sector.”

Best of all, with profit margins that blow the doors off its competitors, its stock is set to soar in

the months ahead.

Unprecedented Profit Margins… So Why the Dirt Cheap Valuation?

By dominating its markets, quickly expanding across the globe, and consistently developing new

resources, Gazprom has created a heavy-duty profit machine.

And that is not an exaggeration…

According to the latest annual report audited by PricewaterhouseCoopers, the company set new records

in sales revenue, currency earnings and net profit. Earnings per share leapt 141%. Net profits

jumped 141%. And dividends per share were up an astonishing 110%.

3

Oxford Communiqué Investor Report: Why the World’s Most Profitable...

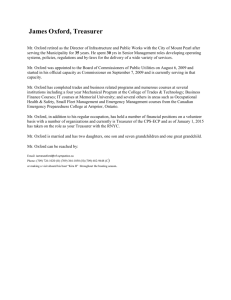

600

400

771.2

800

1,183.0

Net Profit in Russian Rubles

1,000.9

1,000

634.1

200

2012

2011

0

2010

Royal Dutch Shell was ranked

#1 in the globe in terms of total

revenues. It brought in $470 billion.

Gazprom, on the other hand, made

more money on far less revenue: just

$158 billion.

1,200

2009

But here’s where it gets interesting…

Gazprom’s Profits are the Best in the Energy Business

Profits (in Billions)

Bottom line profits were nearly

US$45 billion. By comparison,

Royal Dutch Shell had $31 billion

in profits.

In other words, the profit margins for Gazprom are off the charts. Its current profit margins of

27.21% are more than four times Royal Dutch Shell’s 5.52%.

As the company chairman recently stated in a presentation to shareholders, “Gazprom is on top

of the world in terms of net profit among not only oil and gas companies, but also all other

companies in the world!”

And as we mentioned above, Royal Dutch Shell, Exxon Mobil, Chevron and even Brazil’s

Petrobras trade at around 9 times earnings, while Gazprom trades at a ridiculous 2.85 times

earnings. That means in just three years, it is likely to make more money in profits than the

company’s entire current value.

Forbes has called it a “company investors cannot ignore.” Adding, “What makes Gazprom a buy

is its position in the natural gas market, its massive reserves, and regional demand for the only

clean burning fossil fuel around.”

So why haven’t Americans heard about Gazprom? And why is it trading at such a dirt cheap

valuation?

You Don’t Own This Stock Because You Weren’t Allowed To…

It’s amazing to think that a company as big, profitable and primed for future expansion as

Gazprom could be flying under-the-radar. But there’s one very good reason why it still trades so

cheaply…

Because for many years, almost nobody in America (or outside of Russia for that matter) was

allowed to buy it.

4

Oxford Communiqué Investor Report: Why the World’s Most Profitable...

As we said, amongst energy companies, Gazprom is extremely young. It only started trading in

the 1990’s. It is also a very tightly held company. Even just a few years ago, there were major

restrictions on who could own shares.

According to company guidelines, shares “were issued in line with 144 A Rules and Regulation S,

meaning that US institutional investors with a portfolio of over $100 million… had the rights to

ownership of the Company’s receipts.”

Translation: the individual investor was left out. Trading was essentially limited to investment banks,

money management firms and hedge funds. And explains why most of us remained unaware of this

energy giant.

Because of this unique restriction, there was no reason for Gazprom to get any attention

in the financial media. The institutions with $100 million or more were happy to grab up

ultra-cheap shares. And they did exactly that…

Newgate Capital Management, Ameriprise Financial, the Renaissance Group, RMB Capital

Management, Aberdeen Asset Management and a handful of other big investment firms bought

hundreds-of-thousands of shares.

But they had no incentive to tell any of their clients or to try and get the mainstream media to

talk about Gazprom, because regular small-time investors weren’t allowed a seat at the table. The

company was never made available on the NYSE, Nasdaq or even the American Exchange. And

so for years, American investors had no idea it even existed.

A few years ago, to remedy the situation and bring the stock up to where it rightfully belongs,

Gazprom executives decided to make the stock available to a wider audience. As a result,

Gazprom expanded its stock listings to include the London Stock Exchange and the Berlin and

Frankfurt exchanges in Germany.

It also began offering ADR (American Depository Receipts) shares on the US over-the-counter

(OTC) stock market.

From a corporate perspective, Gazprom executives have already achieved their goal of becoming

“the strongest company in the world’s energy sector.” However, from a personal wealth

perspective, company executives (including the Russian government which owns slightly

more than 50%) haven’t realized the financial windfall they expected for themselves and other

shareholders.

So, despite Gazprom executives efforts to expand the availability and trading volume of their

shares… it has not resulted in the hoped for increase in share price.

The stock has simply not realized its full potential...

5

Oxford Communiqué Investor Report: Why the World’s Most Profitable...

Gazprom’s stock trades for far cheaper than any of the other big players. Based on a price-toearnings basis, Gazprom is trading at a third of the value of its leading competitors, which

includes Royal Dutch Shell, ExxonMobil, Chevron, etc.

This puts Gazprom in an unusual situation; the world’s most profitable energy company is both

overlooked and highly undervalued. But this is the exact reason why the company offers such

immense profit potential in the days ahead.

Here’s why…

The Major Announcement… And Why It Could Triple Your Money

Gazprom has dominated almost every major market it’s gone after. Europe, Japan, India,

China… You name it. But now, it’s about to go after another market…

For the first time in company history, it’s decided to enter the North American and Latin American markets.

Russian media outlets indicate it will target “a number of countries there, including, primarily, the United

States.”

Soon enough Americans could start seeing Gazprom’s name on billboards, TV ads, and trucking

gas and oil down the highways. And you might wake up one morning to see its name on the

front page of The Wall Street Journal.

Here’s what we think is going to happen…

In preparation for Gazprom’s big move into North America, we believe there is a high chance

it will soon make the unexpected announcement that its shares will be listing on the New York

Stock Exchange (NYSE), the world’s deepest and most liquid market.

When this announcement hits the mainstream media, the stock will go roaring up the charts.

The financial media will be screaming with press coverage. And individual investors across the

country will likely begin buying up millions of shares. Likewise, pension funds, endowments and

mutual funds that couldn’t own Gazprom’s stock before will begin snatching up shares on a grand

scale.

Currently only a small percentage of institutional investors own shares of Gazprom – relative to

the much higher percentages of its competitors and other companies of similar market cap.

This is due to self-imposed rules set by the mutual fund companies, investment banks and

pension funds that restrict the purchase of over-the-counter (OTC) stocks (in favor of bigger,

safer stocks on the NYSE & AMEX). Instead, they generally only purchase shares trading on

major stock exchanges.

6

Oxford Communiqué Investor Report: Why the World’s Most Profitable...

But if Gazprom gets itself listed on the NYSE, interest will pour in from almost every fund

category. From value investors to growth stock buyers to international funds and energy

sector players: all will find things they like about Gazprom.

Simply put, institutional investors will send shares flying. But for those investors who already

own the stock… they can just sit back and enjoy the ride. That’s why we created this report.

There may only be a very short window left in which Gazprom remains overlooked and

extraordinarily cheap.

And if shares never get listed on the NYSE, that is fine with us. You can still buy the over-thecounter shares today. With all the publicity and profit potential surrounding the company’s move

into North American and Latin American markets… this alone should help to move the shares

steadily higher.

Don’t misunderstand this… there is nothing wrong with an OTC stock listing. It’s true that

many companies that trade OTC do so because they’re financially weak or too small to meet

major exchange requirements.

But with a market cap over $100 billion, size is not a concern for Gazprom.

Neither is it financially weak, with some of the most solid fundamentals in the industry (audited

by PricewaterhouseCoopers, the world’s largest accounting firm).

Its return-on-assets of 11.04% and operating margins of 22.59% both beat the industry averages

that come in at 8.15% and 14.51%. Its return-on-equity is 15.85%, right in line with the

industry. And its debt load is more than 13 points below its competitor’s average.

Another important factor is liquidity. For stocks, a general rule of thumb is (at least) an average

volume of 50,000 shares a day. Gazprom’s OTC average daily volume over the past 12 months

clocks in at 938,721… We can comfortably say there is adequate volume here.

And let’s not forget Gazprom trades at a ridiculously cheap price. The stock currently sells at less

than three times earnings. That’s lower than just about every stock on the NYSE, and it’s more

profitable than all of them.

If the stock merely trades up to the same earnings multiple of its nearest competitor, Exxon,

it would more than triple in value. In order to reflect its true profitability, it would have to go

even higher. This is perhaps the best buying opportunity we’ve seen for many years in the energy

market.

Action to Take: Buy Gazprom (OTC: OGZPY) at market. And use a 25% trailing stop to

protect your position and your profits.

7

Oxford Communiqué Investor Report: Why the World’s Most Profitable...

The “Over-the-counter,” or OTC market, is a term loosely applied to securities that aren’t listed

on an organized exchange – such as the New York Stock Exchange (NYSE) or American Stock

Exchange (AMEX). Market participants trade over an electronic network, the telephone or

facsimile instead of on a physical trading floor. There is no central exchange or meeting place for

this market.

OTC stocks are traded through numerous “market makers” who maintain bids and offers for the

securities they trade. The Financial Industry Regulatory Authority (FINRA) regulates brokerdealers that operate in the over-the-counter (OTC) market.

Many large, non-U.S. companies trade on the OTC market; including Nestle, Deutsche

Telecom, Roche, BASF and Adidas. In fact, the combination of large foreign corporate listings

with the explosion of initial public offerings and subsequent OTC listings make it the biggest

market in the world. So when it comes to Gazprom, don’t worry about buying it on the OTC.

If the company does decide to list its shares on the NYSE, your OTC shares will automatically

convert over.

Alternative Action to Take: Investors can also consider purchasing the stock on the London Stock

Exchange. It is listed as Gazprom (LSE: 81JK.L).

The volume and fundamental ratios are very similar to the OTC shares. Just be sure and check that

the commission charges are comparible to buying it on the OTC. But for any non-U.S. residents or

anyone interested in purchasing this stock in a currency other than the dollar, the LSE may be the

easiest and most economical way to go about it.

Pillar One Advisor Jeff Winn with International Assets Advisory can help you with equity trades

on international markets. His contact information is listed below.

International Assets Advisory, LLC

Jeff Winn, Wealth Protection Director

300 South Orange Ave. Ste. 1100 • Orlando, FL 32801

Ph: (800) 432-4402 or (407) 254-1522 • Fx: (407) 254-1540

Web: www.iaac.com • Email: jwinn@iaac.com

8

From time to time, The Oxford Club will discuss investment ideas that will not be included in the Club’s various portfolios. There are certain situations

where we feel a company may be an extraordinary value but may not necessarily fit within the selection guidelines of these existing portfolios. In these

cases, the recommendations are to be considered speculative and should not be considered part of any of the Club’s portfolios.

Also, by the time you receive this report, there is a chance that we may have exited a recommendation previously included in one of our portfolios.

Occasionally, this happens because we use a disciplined “trailing stop” philosophy with our investments, meaning that any time a company’s share

price falls 25% from its high, we sell the stock.

If you have any questions about your Oxford Club subscription, or, would like to change your email settings,

please contact us at 800.992.0205 Monday – Friday between 9:00 AM and 5:00 PM Eastern Time. Or if calling

internationally please call 443.353.4056.

© 2013-present The Oxford Club, LLC All Rights Reserved

The ww | 105 West Monument Street | Baltimore, MD 21201

North America: 800.992.0205; Fax: 1 410.246.2297

International: 443.353.4056; Fax: 1 410.246.2297

Email: customerservice@oxfordclubinfo.com

The Oxford Club is a financial publisher that does not act as a personal investment advisor for any specific individual. Nor do we advocate the

purchase or sale of any security or investment for any specific individual. Club Members should be aware that although our track record is highly

rated by an independent analysis, and has been legally reviewed, investment markets have inherent risks and there can be no guarantee of

future profits. Likewise, our past performance does not assure the same future results. All of the recommendations communicated to members

during the life of this service may not be reflected here. The stated returns may also include option trades. We will send all our members regular

communications with specific, timely strategies and updated recommendations; however, you should not consider any of the communications by

our company and employees to you as personalized investment advice. Note that the proprietary recommendations and analysis we present to

members is for the exclusive use of our membership.

We expressly forbid our writers from having a financial interest in any security recommended to our readers. All of our employees and

agents must wait 24 hours after on-line publication or 72 hours after the mailing of printed-only publication prior to following an initial

recommendation. Any investments recommended in this letter should be made only after consulting with your investment advisor and only after

reviewing the prospectus or financial statements of the company.

Protected by copyright laws of the United States and international treaties. This newsletter may only be used pursuant to the subscription

agreement and any reproduction, copying, or redistribution (electronic or otherwise, including on the worldwide web), in whole or in part, is

strictly prohibited without the express written permission of The Oxford Club, LLC. 105 W. Monument Street, Baltimore MD 21201.

The Oxford Club

105 West Monument Street | Baltimore, Maryland | 21201 | 443.353.4056

COMMIR0613-16

300R013063