Figuring Out Where To Live

advertisement

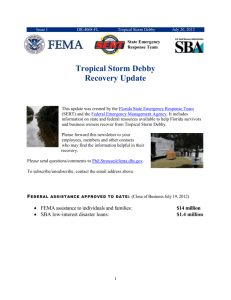

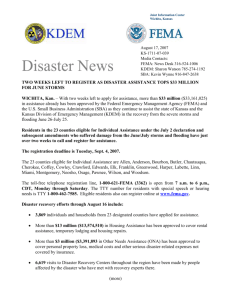

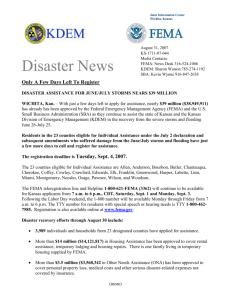

Figuring Out Where To Live Finding a place to live is a big challenge for those who cannot live in their home due to a disaster. Some actions will be different depending on whether you own your home or rent. Below is chart and series of housing considerations to work through after a disaster. Question 1: Where will you live? If you rent, first contact your property manager/landlord Find out when your home will be livable Immediately Decide what to do, if anything, to make your home safe, sanitary, and secure In the near future Never or too long Contact a disaster case manager, American Red Cross, or other agency for possible temporary housing assistance Arrange for temporary housing until you can find affordable, long-term rental housing or until your home is ready Find alternative affordable housing option Determine how much money or resources you still need to get back into your home Proceed to Question 2 If you rent, request return of security deposit Question 2: What type of insurance do you have? Homeowners or Renters No Yes Auto Disaster-specific (flood, etc.) Yes Contact insurance agent to determine coverage for home/housing, personal property; and temporary housing No Yes No Contact your insurance agent to determine coverage Document your damage/loss using the tips for documenting loss from the MU Extension Right Away: A Few Tools for Financial Recovery Determine the current amount of uncovered loss and unmet needs after or without insurance coverage Consider whether you can claim the property loss as a deduction on your income taxes by contacting the IRS to receive a Disaster Loss Kit (see the MU Extension Right Away: A Few Tools for Financial Recovery) Proceed to Questions 3 and 4 Question 3: Is the disaster federally declared, with FEMA1 individual Household Assistance Programs and SBA2 low interest loans available? Yes No Apply for a FEMA and/or SBA loan FEMA grant and/or SBA loan denied; you may appeal FEMA grant and/or SBA loan received Determine the current amount of loss and unmet need, subtracting any FEMA and SBA assistance Proceed to Question 4 1 FEMA stands for the Federal Emergency Management Agency, which is the primary agency that helps families and individuals in disaster recovery. Individuals and households can apply for FEMA’s Individual and Household Assistance Program (IHP). For more information contact FEMA at (800) 621-FEMA or www.FEMA.gov. 2 SBA stands for the Small Business Administration, which in addition to helping businesses in disaster recovery, also provides low-interest loan assistance to eligible homeowners, renters, and eligible non-profit organizations. Contact the SBA at 800-659-2955 or www.sba.gov. Question 4: Is the disaster state declared, with SBA low interest loans or state-initiated loans and grants available? Yes No Apply for a SBA loan and/or state loan/grant SBA loan and/or state loan/grant denied SBA loan and/or state loan/grant received Determine the current amount of loss and unmet need, subtracting any FEMA and SBA assistance If you are a flooded homeowner, investigate if there will be a property acquisition “buy out” program (note that this process may take 9-24 months to complete). See what other types of assistance and resources may be available to you by talking with disaster case managers, community agencies, community long-term disaster recovery committees and churches or other charitable organizations. Do not forget friends, family, and personal networks. Post-Disaster Housing Commitments When a natural disaster occurs, your home may be unlivable for a short period. A business you owned or worked for may also have damages, leaving you without income. If you own your home, you may have to make mortgage payments in addition to paying rent. Be sure you understand the status of your financial commitments and obligations. If you own your home Check the rules outlined in your mortgage agreement about late, missed, or reduced payments. Your mortgage agreement probably outlines your options when you are not able to make mortgage payments. If you have troubles paying your mortgage, explore a workout agreement with your lender. A workout agreement can be a temporary or permanent change to your mortgage agreement. Try to get a workout plan that your lender will accept, you can fulfill and that still meets your needs. Workout options will vary based on the type of mortgage you have, your lender, and your financial situation. For more information about workout options, visit www.hud.gov/offices/hsg.sfh/econ/loandworkoutsolutions.cfm. If you are at risk for foreclosure, get help immediately Foreclosure is a legal process for the lender to seize your home. You may need an attorney with expertise on the foreclosure process in your state. A foreclosure prevention counselor can help you look at the pros and cons of loan workout options and help you explore assistance programs to prevent foreclosure. To find a trained foreclosure prevention counselor in your state, contact the U. S. Housing and Urban Development office at 800-569-4287 or www.hud.gov. Other organizations that may be able to help include: National Foundation for Credit Counseling (800-388-2227 or www.nfcc.org) Homeownership Preservation Foundation (888-995-HOPE or www.995hope.org) NeighborWorks America (888-995-4673 www.nw.org) If you are a renter Missouri law requires your property owner to release you from your lease if your rental unit is unlivable. Notify the property owner in writing and ask for the return of your deposit. If you are struggling to pay rent, contact the National Foundation for Credit Counseling (800-388-2227 or www.nfcc.org) to find a legitimate credit counselor. Adapted from Recovery After Disaster: The Family Financial Toolkit (University of Minnesota Extension, North Dakota State University Extension Service, and Lutheran Social Service of Minnesota) by Brenda Procter, M.S., State Specialist & Instructor, and Graham McCaulley, M.A., Extension Graduate Assistant, Personal Financial Planning, College of Human Environmental Sciences, University of Missouri Extension equal opportunity/ADA institutions