Productivity and Innovation Credit (PIC) Scheme

advertisement

Scheme")

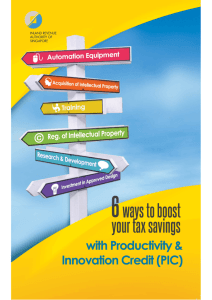

Productivity and Innovation Credit (PIC) Scheme PRESENTATION BY INLAND REVENUE AUTHORITY OF SINGAPORE 22 NOVEMBER 2011 Agenda Productivity and Innovation Credit (PIC) Scheme Overview Tax Benefits How to Claim for PIC Details on What Qualifies for PIC Training of Employees PIC Automation Equipment Assistance and Service Channels Q&A 2 Overview of PIC Scheme Introduced in Budget 2010 and enhanced in Budget 2011 Encourage businesses to invest in productivity and innovation All businesses benefit, especially SMEs - Either get a cash payout or claim tax deduction 3 Overview of PIC Scheme 6 activities covered under scheme: Training of Employees Purchase/Lease of PIC Automation Equipment Acquisition of Intellectual Property Registration of Intellectual Property Research & Development Approved Design Project 4 Tax Benefits under PIC 400% tax deduction/allowances on expenditure on each of the 6 activities (YAs 2011 to 2015) Opt for cash payout in place of tax deduction/allowances (YAs 2011 to 2013) 5 Tax Deduction / Allowances 400% tax deduction/allowances on up to $400,000 expenditure per year in each of the 6 activities To allow max PIC benefits, the spending cap across YAs for each activity is as shown below: Years of Assessment Expenditure Tax Deduction cap per activity per activity 2011 and 2012 (Combined) $800,000 $3,200,000 (400% x $800,000) 2013 to 2015 (Combined) $1,200,000 $4,800,000 (400% x 1,200,000) For newly incorporated/registered businesses whose 1st YA is YA 2012, the expenditure cap per activity is $400,000 Expenditure is net of grant or subsidy Expenditure exceeding the cap can still enjoy deduction based on 6 existing rules Tax Deduction / Allowances Potential Maximum Benefits for YAs 2011 & 2012 combined Deduct up to $19.2m (400% x $800,000 x 6 activities) R&D Training IP Acquisition 400% deduction/allowances on up to $800K expenditure Automation IP Registration Design 7 Tax Deduction / Allowances Example (YA 2011) Expenditure on staff training = $900,000 Total tax deduction = $3,300,000 $100,000 $100,000 (remain 100% deduction) $800,000 $3,200,000 (400% x $800,000) 8 Cash Payout Option Option to convert expenditure of up to $100,000 in all 6 activities per YA At 30% conversion rate Expenditure converted is not tax deductible $100,000 $30,000 Expenditure Cash Payout Cash payout is non-taxable 9 Cash Payout Option Year(s) of Assessment Expenditure cap for all 6 activities Maximum cash payout 2011 and 2012 (Combined) $200,000 $60,000 (30% x $200,000) 2013 $100,000 $30,000 (30% x $100,000) For newly incorporated/registered businesses whose 1st YA is YA 2012, the expenditure cap for all 6 activities is $100,000 10 Cash Payout Option Conditions for cash conversion Employed at least 3 local employees (Singapore Citizens or PRs with CPF contributions) in the last month of accounting period Carrying on business operations in Singapore Note: Employees exclude sole-proprietors, partners under contract for service, shareholders who are also directors of companies 11 How to Claim PIC 400% tax deduction Cash payout Applicable YA YAs 2011 to 2015 YAs 2011 to 2013 How Claim tax deduction/allowances in income tax return Submit PIC cash payout application form (available on IRAS’ website) When For company, submit income tax return by the filing due date: 30 Nov Anytime after accounting year-end but not later than the income tax For sole-proprietor/partnership, submit filing due date income tax return and PIC declaration form by the filing due date: 15 Apr 12 Most SMEs would have some spending on: - Staff Training - Purchase of Automation Equipment 13 Training of Employees 14 Training of Employees External training All external training qualify Qualifying Expenditure Includes Qualifying Expenditure Excludes Course fees to any external training Accommodation, travelling and transport expenses of employees attending the training service provider E.g. registration or enrolment fees, examination fees, tuition fees and aptitude test fees Overheads like imputed rental and utilities Rental of external training premises Meals and refreshments provided during the courses Training materials and stationery 15 Training of Employees In-house training Qualifying training programmes: (a) Workforce Skills Qualification (WSQ) training courses accredited by the Singapore Workforce Development Agency and conducted by a WSQ in-house training provider; (b) courses approved by the Institute of Technical Education (ITE) under the ITE Approved Training Centre scheme; and (c) on-the-job training by an on-the-job training centre certified by ITE 16 Training of Employees In-house training Qualifying Expenditure Includes Qualifying Expenditure Excludes Salaries and other remuneration Salaries and other remuneration (excluding director fees) paid to inpaid to in-house trainers for other house trainers for course delivery duties including preparation of training material Rental of external training premises Salaries and other remuneration Meals and refreshments provided paid to employees providing during the courses administrative support Training materials and stationery Absentee payroll Accommodation, travelling transport expenses and Overheads like imputed rental and utilities 17 PIC Automation Equipment 18 Purchase/Lease of PIC Automation Equipment Automation equipment that qualify for PIC with effect from YA 2011 are prescribed in the “PIC Automation Equipment List” PIC Automation Equipment List • Includes existing Section 19A(2) prescribed automation equipment; and • Expanded scope and new additions Both purchase and leasing (only for own use) of automation equipment qualify for PIC One expenditure cap applies for both purchase cost and lease payments: • $800,000 for YAs 2011 and 2012 combined; and • $1,200,000 for YAs 2013 to 2015 combined 19 PIC Automation Equipment Existing Section 19A(2) prescribed* automation equipment includes: Facsimile Optical character reader Laser printer Mainframe/Computers Milling machines Office system software Automatic storage and retrieval system of warehouses Injection mould machines Automotive navigation systems Automated kitchen equipment for the purpose of food processing Interactive shopping carts Automated housekeeping equipment Automated seating systems for convention or exhibition centre Self-climbing scaffold system Concrete pumps * Refer to Income Tax (Automation Equipment) - Rules 2004; and - Amendment Rules 2010 (effective from 15 Dec 2010) 20 PIC Automation Equipment (Expanded Scope) Item Prescribed Automation Equipment [S19A(2)] PIC Automation Equipment 7 Computer controlled machine for cutting and removal operations with automatic tool change capabilities, including CNC lathes, milling machines, EDM wirecut, machining centers, grinders, presses and laser equipment. Computer controlled machine for joining (new), cutting or removal operations, including CNC welding machine (new), CNC lathes, milling machines, EDM wirecut, machining centers, grinders, presses and laser equipment. 14 Injection mould machines used for making plastic, ceramic or metal components in factory production. Injection mould machines used for making plastic, ceramic, metal or silicone rubber (new) components in factory production. 21 PIC Automation Equipment (New Additions) Item PIC Automation Equipment 30 Automated sorting system, automatic inserting system with high speed cutting, collating, folding and inserting of documents into envelopes, and automatic packaging system for packaging or repackaging of products into plastic films or plastic wraps. (new) 31 Hydraulic bucking unit which includes high automatic function for quick make-up or break-out. (new) 32 Automated machine used in laundry processes, including automatic linen feeder, automatic linen folder and stacker, laundry conveyor system and automatic garments managing system, but excludes washing or drying machine. (new) 33 Automated sludge treatment machine. (new) 34 Automatic machine used in vegetable farming processes, including auto-seeding machine for seed plugs and auto-seed plug transplanting machine, and automatic machine used in vegetable packaging 22 processes. (new) Flowchart on PIC Automation Equipment Automation Equipment In PIC Automation Equipment List No Yes Qualify for Prescribed Automation List*[S19A(2)] Yes Capital Allowance: 1 Year E.g. computers, laptops, printers Case–by-case approval, subject to meeting criteria Approved cases No Capital Allowance: 3 Years E.g. CNC welding machine, automated machine used in laundry processes * Refer to Income Tax (Automation Equipment) - Rules 2004; and - Amendment Rules 2010 (effective from 15 Dec 2010) 23 PIC Automation Equipment Case-by-case approval Businesses that invest in specialised equipment not in the PIC Automation Equipment List, to automate their processes and to enhance productivity may apply to IRAS to have their equipment approved for PIC on a case-by-case basis 24 PIC Automation Equipment Cash conversion option Election is on “per equipment” basis (can’t claim tax deduction and cash payout on the same equipment) Expenditure in excess of conversion cap forfeited Hire purchase equipment with repayment covering 2 or > basis periods not eligible for cash conversion 25 PIC Automation Equipment Minimum ownership period Minimum 1-year holding for purchased equipment Claw-back of allowances or cash payout may apply if equipment disposed of or leased out within 1 year from date of purchase Waiver of claw-back provisions Automatic waiver: If in the basis period when the equipment was acquired, the cost of qualifying equipment acquired (excluding the cost of equipment disposed of) is more than or equal to the expenditure cap applicable to that basis period Case-by-case basis: If IRAS is satisfied with the commercial reason(s) that led to the disposal 26 PIC Automation Equipment Example - Automatic waiver Acquired $1,000,000 worth of qualifying equipment in Jun 2010 (Enhanced allowances claimed in YA 2011 - $800,000) Holding period less than one year Jan 2010 Dec 2010 Dec 2011 Disposed of equipment costing $100,000 in Jan 2011 Claw-back provisions automatically waived as cost of remaining qualifying equipment of $900,000 ($1 mil - $100K) is higher than expenditure cap of $800,000 27 Assistance and Service Channels Website http://www.iras.gov.sg <Businesses><For Companies (including Productivity and Innovation Credit scheme)> Email - ctmail@iras.gov.sg for general tax matters - ctpayment@iras.gov.sg for payment matters - picredit@iras.gov.sg for Productivity and Innovation Credit Helpline - For companies: 1800-356-8622 - For self-employed/partnership: (+65) 6351 3534 - 8.30am to 5.00pm from Mondays to Fridays 28