Lessons to be drawn for lenders and directors from the Bell Group

advertisement

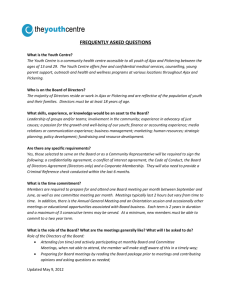

Allens Report: Lessons to be drawn for lenders and directors from the Bell Group appeal decision Partner Diccon Loxton looks at the recent appeal decision of the Western Australian Court of Appeal in the Bell Group litigation1, a saga concerning work-outs, which suggests that company directors and banks can be subject to increasing judicial scrutiny, and that courts are overcoming their reluctance to second-guess directors’ decisions in determining whether there is sufficient ‘corporate benefit’. What does it mean for future practice? How does it affect you? • • • • • 1 The judgment has some significant things to say about directors’ duties under general law (which continue in addition to their statutory duties) and the possible liability of lenders and others as constructive trustees. Lenders may want to take a more cautious approach in work-outs in taking security and guarantees, particularly when they are not providing new funds. They cannot assume that they will be no worse off if the transaction is set aside – they risk losing more than they stand to gain. This may make work-outs more difficult to achieve. Lenders may want to take more care in their procedures for taking guarantees generally from companies in corporate groups, and pay greater attention to the position of individual companies in assessing corporate benefit. Directors may also need to take a more cautious approach more generally. In particular, directors in a work-out have one more reason to obtain independent legal advice. Lenders dealing with corporate groups should take some care to make sure they are not structurally subordinated to other financial creditors, and that subordinated creditors are truly subordinated in the structure. The Bell Group saga in a nutshell On 17 August 2012, the Western Australia Court of Appeal handed down its 1024-page appeal judgment. The appeal was from the 2643-page judgment of Justice Owen handed down in October 2008. The case concerned an attempted work-out in January 1990. In that work-out, banks took guarantees and security from a large number of companies in the Bell Group, and control over all proceeds of sale of their assets, in exchange for the banks postponing the maturity of their previously unsecured loans. The companies also subordinated their intercompany debt, but the banks gave no new funding. More than a year later, the companies went into liquidation and the banks enforced the security and recovered $283 million. The companies and their liquidators sued. Among other things, they claimed that the guarantees and security, and the subordination, had been given in breach of directors’ duties (in very broad terms, that there was insufficient corporate benefit). In part this was because the companies were insolvent and it prejudiced other creditors. They said the banks had the requisite knowledge of that breach and were liable as constructive trustees. Two of the three appellate judges agreed. All three judges agreed the transactions should be set aside under bankruptcy legislation. The trial judge had said the companies were insolvent, and this was not appealed. Westpac Banking Corporation v The Bell Group Limited and others [No 3] 2012 WASCA 157. ©2012 Allens 2 If the judgment stands, the banks between them must pay an amount estimated to be between $2 and $3 billion – the amount received from the security plus monthly compound interest at an overdraft rate plus 1% pa. Much of that amount will ultimately be returned to the banks as creditors in the winding up, but a significant portion will end in the hands of holders of subordinated bonds issued by a special purpose finance subsidiary, which on-lent the issue proceeds to Bell Group companies. The Court of Appeal (2:1) found that the on-loans were not subordinated, overruling the first instance judge. The result is that the bondholders are not effectively subordinated to the banks. From the banks’ point of view, there will be substantial ‘leakage’ to the bondholders. Statute law has significantly changed since the events examined in the case. Nevertheless, it is a significant case study of a work-out, and most of the issues arose from general law duties, not corporations legislation. Many of the underlying principles remain relevant and there are lessons to be drawn. Banks Loans Subordinated Bond Holders d ate rdin tee o b Su uaran G Guarantee Original Committed Bell Companies On-loan Other Bell Companies Subordinated Bonds BGNV On-loan The lessons learnt: practical tips and precautions The lessons for directors and lenders involved in work-outs or when lenders take guarantees and security include the following. They arise from either or both of the first instance and appeal decision. Section 187 Corporations Act 2001 (Cth) But first, one useful precaution whenever wholly-owned subsidiaries are involved and there may be questions of corporate benefit is to have a provision in the subsidiaries’ constitutions allowing their directors to act in the best interests of the holding company, as contemplated by s187. That was not available at the time of the Bell Group transactions but, in any event, would not have helped (the companies were insolvent, and the court may have said the transaction was not in the best interests of the holding company). When companies in a solvent group are giving a guarantee of a new financing Directors: (i) in the case of a wholly-owned subsidiary, prefer that it has a provision in its constitution contemplated by s187; (ii) where you can’t rely on it separately, examine the position of each company in determining corporate benefit, and minute it; (iii) ensure that the minutes of any meeting are accurate and a meeting is actually held for each company; ©2012 Allens 3 (iv) if you are at all unsure whether there is sufficient corporate benefit, and you need to rely on s187 or, as a last resort, shareholder ratification, satisfy yourselves as to the solvency of the company both before and after giving the guarantee; and (v) if you need a shareholder ratification, because there is insufficient corporate benefit and s187 isn’t available, ensure the ratification is fully informed and recognises expressly that the transaction may not be in the best interests of the company. (viii)at least if you rely on ratification by the company’s shareholders or s187, satisfy yourself as to solvency. Lenders: Directors: (i) ask for your standard requirements, unless you have good reason not to, and be careful in giving them up; in other words, avoid being in a position where you can be accused of wilfully or recklessly shutting your eyes, or having suspicions; (ii) where relevant, ensure each company has a s187 provision in its constitution; (iii) in relation to each company, where you can’t rely on s187, unless the corporate benefit is readily apparent, get defensible, reasonable statements (preferably extracts of resolutions, not full minutes) which set out the reasons why the directors are entering the transaction and the corporate benefit (not simply a statement that there is corporate benefit); (iv) be cautious about you or your lawyers drafting those statements; (v) be very wary of accepting evidence of directors’ resolutions which are implausible (that is, they set out formalities that may not be followed); (vi) be cautious about proforma resolutions set for every single company; (vii)if you rely on ratification, ensure it follows the requirements set out above; and • When companies in a group are asked for security or guarantees while in financial difficulties or seeking a workout Follow the recommendations listed above with more caution, and, in addition, do the following. • • get separate legal advice (this has already become the practice in large work-outs, motivated particularly by concerns about liability for insolvent trading, and, for listed companies, liability under disclosure laws); obtain and critically examine forwardlooking cashflows showing a prospect of paying, continuing or refinancing existing debt; and for each company, be cautious as to creating security in favour of one group of creditors to the exclusion of others, unless there is new funding, or a plan or a reasonable prospect of a plan for the company to continue to pay creditors, or other real benefits. Lenders: • • • obtain and critically examine cash flows showing a prospect of paying, continuing or refinancing existing debt; be aware of the potential issues and requirements for directors (see above); it may well be better for you if directors are independently advised; ask for your standard requirements in relation to information, certificates and ©2012 Allens 4 • • the like, and do not give up the request without significant caution; in other words, avoid being in a position where you can be accused of wilfully or recklessly shutting your eyes, or having suspicions; it is considerably easier to establish corporate benefit if the lender provides some new funding, and, in any event, there should be some capacity within the work-out to pay other creditors as they fall due; and treat with caution any proposed guarantee from a company that has not previously given a guarantee of the debt. own difficulties. The Bell Group companies depended on asset sales proceeds to pay their debts as they fell due and to service interest on the bank loans and subordinated bonds and the associated on-loans. Apart from a web of intercompany debts between the companies, the only other creditor of any significance (and then only in respect of few of the companies) was the Australian Tax Office under a tax assessment which was being disputed. After months of negotiations, TBGL and most of its subsidiaries entered a ‘refinancing’ transaction with the banks under which: The case in depth: the facts • • The Bell Group Limited (TBGL), an Australian listed holding company, and its English subsidiary had borrowed money from banks on an unsecured basis. The banks had once had recourse to a number of other companies in the group but that had been released. • An offshore subsidiary of TBGL and another subsidiary had issued subordinated convertible bonds, guaranteed on a subordinated basis by TBGL. The funds raised in the bond issues were on-lent to TBGL and its finance subsidiary, but the loans were undocumented. Following its takeover by Bond Corporation Holdings Limited, controlled by Alan Bond, and a market decline, TBGL and its subsidiaries (the Bell Group) were in some financial difficulty. A number of the bank loans were on demand. Most of the group’s assets had been sold and the proceeds stripped out to Bond companies. The main remaining assets and possible cashflow sources were a publishing business, their investments in, and loans to, each other, and their investment in, and fees from, other companies controlled by Bond (including Bell Resources Limited), which were having their • the term of the debt was extended; the banks obtained security from the borrowers, and guarantees and security over principal assets from many other members of the group, most of which had not previously guaranteed the debt; the borrower and guarantors undertook that all asset sale proceeds were to be used to pay down the bank debt or be paid into escrow unless the banks otherwise agreed (and the banks’ subsequent practice was to give their consent to the use of proceeds to pay other creditors including bond interest); in other words, all surplus cash was swept to the banks; and intercompany loans within the Bell Group were expressly subordinated (including at a later date the on-loans of the subordinated bond issue proceeds). Most of the refinancing and security documents were executed in early 1990 and the documents subordinating the on-loans in mid-1990. In April 1991, TBGL appointed a provisional liquidator, and the banks then enforced their security and realised the assets. TBGL and a number of its subsidiaries, the liquidators, and the trustee for the bondholders sued the banks. ©2012 Allens 5 The principal findings Owen J at first instance found that: • • • • • • • TBGL and its subsidiaries were insolvent when they entered into the transaction and insolvency was judged looking forward for 12 months; the directors knew, or should have known, that the companies were insolvent, or nearly insolvent; entering the transaction involved a breach of the directors’ duties to act in good faith in the best interests of each individual company and for a proper purpose. These duties were fiduciary duties; the banks knew of the breach, and were therefore liable as constructive trustees, for the amount received plus compound interest (more than $1.6 billion), but only under the first limb in Barnes v Addy (knowing receipt), not the second (knowing assistance); there was no breach by the directors of the duty to avoid a conflict of interest merely because they were directors of other benefited corporations; the on-loans from the offshore subsidiary to TBGL and its finance subsidiary were subordinated as an inferred term in the informal on-loan contract; and the transaction should be set aside under provisions of the Bankruptcy Act 1966 (Cth) then applicable to companies. Both sides appealed, but the finding of insolvency was not appealed. The Court of Appeal decision was even less favourable for the banks. It found: • • • by majority of two (Lee AJA and Drummond AJA) to one (Carr AJA) that the on-loans were not subordinated; that the relevant directors’ duties were fiduciary duties; by majority of two to one that the • • • directors of the various companies breached their duties, but, except for Alan Bond, there was no breach of the no conflicts duty; by the same majority, that the banks had sufficient knowledge of the breach and were liable as constructive trustees under both limbs of Barnes v Addy; by the same majority, that the banks should repay the amount received plus compound interest calculated at monthly rests at Westpac’s overdraft rate plus 1% pa; and unanimously, that the transactions should be set aside under sections 120 and 121 of the Bankruptcy Act, and the banks required to pay compensation. Changes in the law since the case The case was decided on the law as at 1990. There have been a number of changes in statute law since then. The insolvency laws applicable to corporations have changed significantly. Among other things, the changes introduced a regime to allow the setting aside of voidable transactions in liquidation (including uncommercial transactions), and the voluntary administration regime and the accompanying strict liability for directors for insolvent trading. There have been some changes in statutory ‘directors’ duties’: the Corporations Act 2001 (Cth) now contains (in section 181) obligations on directors paralleling their general law duties to act in good faith in the best interests of the company and for a proper purpose, as well as the duty of care and diligence (subject to a business judgment rule) in section 180. These are civil penalty provisions, which means that a lender knowingly involved in the ©2012 Allens 6 wholly-owned subsidiary to act in the best interests of its holding company if the subsidiary’s constitution allows it. It provides that, in those circumstances, they are deemed to have acted in good faith in the best interests of the subsidiary. But they are not deemed to have acted for a proper purpose. Is this a gap? Will the subsidiary’s directors still be in breach of the proper purpose duty? The answer must be no, that if acting in the best interests of the holding company is expressly authorised by the constitution, doing so must be a proper purpose. breach can be liable for compensation. These ‘duties’ are in addition to the general law directors’ duties, which continue. On the plus side for lenders, there is now s187, which allows a wholly-owned subsidiary to put provisions in its constitution allowing it to act in the best interests of its holding company if it is not insolvent. The statutory ‘indoor management rule’, then in s68A of the Companies Code, and now in s128 and s129, has been changed to favour outsiders (though it does not appear to have been raised in the Bell Group case). These affect both general law and statutory duties. Some relevant points to note • Some of the main factors influencing the majority were the fact that the transaction gave the banks security and control of the asset sales proceeds, enabling them to cut off payments to other creditors, and there was no plan for reconstruction. Other creditors were prejudiced. The fact that it would postpone liquidation, allowing a more orderly realisation of assets for a higher price, was insufficient benefit if it meant that all the proceeds of the realisation were diverted to only some creditors. The purpose of the transaction was seen to provide the banks with security in priority to others. Some directors, the court found, were also motivated by a ‘Bond-centric’ view of trying to stave off pressure on the Bond companies. Owen J at first instance also pointed out that the position would have been very different had the banks provided new money. The Court of Appeal mentioned this but did not concentrate on this aspect, and it is not clear whether it would have been definitive. The majority found there was no or Directors’ duties • • All three judges saw the general law duties to act in good faith in the best interests of the company, and to act for a proper purpose, as two separate duties. Commonly, these two duties are elided. In cases concerning guarantees, the courts more usually concentrate on the duty to act in good faith. The duty to act for a proper purpose is more often seen in contexts like the directors issuing shares to avoid takeovers. The majority found a breach of both duties. They focused as much on the proper purpose duty as the other. This is a significant development, in two ways: (i) It can give a significant opportunity for judicial review of directors’ decisions as seen below. (ii)It could also raise a question mark as to the operation of s187 of the Corporations Act. That section effectively allows directors of a solvent • • ©2012 Allens 7 • • • 2 insufficient examination by directors of the position of each company. The directors’ duty was to the individual company, and, though they may normally consider the group position, as the companies approached insolvency their interests diverged. The majority thought that the breaches were so ‘egregious’ that they did not need to apply the test in the Charterbridge case2, which applies where directors of companies in a group do not separately cast their mind to the position of each company. Carr AJA came to a very different interpretation of the facts. He thought that the directors did have a broad strategy (if not an exact plan) for saving the group; that they had no other option, other than liquidation; that they negotiated hard; and that the banks reserved their right to retain control of cash flow mainly to prevent a sweeping of cash to the Bond interest, with the intention (as proved to be the case) that they would allow payment of other creditors as they fell due. His views on directors’ duties were also different in some respects. The directors could, to a greater extent, take account of their position in the group. The court should apply the Charterbridge test as to what a reasonable director would do when there is no separate consideration for a company. He had different views on the application of the proper purpose duty, outlined below. The majority significantly extended what is very loosely called ‘the duty to creditors’ – traditionally seen as a requirement that, when the company is in an insolvency context, directors must consider the interests of creditors as part of their duties to the company. • They said it was more than just an obligation to consider creditors. It was a requirement not to prejudice creditors, though still owed to the company, not creditors. It required there to be a consideration of the position of each creditor, to the point of requiring an examination of whether the defence of the tax office claim would be pursued and whether it would succeed. The majority gave no guidance as to the boundaries of what is an insolvency context, as to how close to insolvency the company must be before the principle applies. Owen J in the first decision gave it a wide compass. The standard applied to the directors was high. The majority thought the directors should have investigated a number of issues. The directors of the English companies in the group had gone to the extent of obtaining separate advice, but, in the eyes of the majority still failed in their duties, as they did not follow that advice to the letter, and relied on statements by other Bell Group companies as to their creditworthiness, rather than having a separate investigation made. Whether the duties are subjective or objective, that is, will the courts impose their own standard? • Traditionally courts have been reluctant to ‘second-guess’ business decisions taken by directors, but Drummond AJA expressly said the courts are moving in that direction. In this case, the court needed to do so if it wished to overturn the directors’ decision, as at least one of the directors genuinely believed what he was doing was Charterbridge Corporation v Lloyds Bank [1970] Ch 62. ©2012 Allens 8 • • in the best interests of the company. Lee AJA went so far as to say that where the company was facing insolvency and the directors entered a dealing that had the effect of prejudicing the interests of creditors, it did not matter if the directors honestly believed that the entry was in the best interests of the company and its creditors. All the appellate judges followed the traditional notion that the duty to act in good faith and the best interests of the company was subjective. The duty was satisfied provided the directors genuinely thought they were acting in the company’s best interests. The courts would only examine the merits of the decision in order to test as a matter of evidence whether the directors genuinely believed it, or where the directors of individual companies had not turned their mind to the position of those companies. (Note: s181 of the Corporations Act appears to apply an objective standard to a statutory ‘duty’ expressed in the same terms). However, both majority judges placed limits on this principle. Courts could still overturn a decision of directors if no reasonable board of directors could make that decision, or it was made on irrelevant considerations or without taking into account relevant considerations (this is known as Wednesbury unreasonableness, a concept from administrative law). This enabled them to re-examine the Bell Group directors’ decision, using words such as ‘unreasonable’ or ‘not rational’, applying tests not normally seen in fiduciary duties. Carr AJA thought that there was a similar rule, that the courts would not support an ‘irrational’ decision, but did not think it applied in this case. • The majority thought that the duty to act for a proper purpose was to be tested objectively. That is, the courts could decide whether the directors’ purpose was proper. This applies even where the directors thought it was in the best interests of the company. This can enable significant court intervention, particularly if the duty is applied as the majority saw it. Carr AJA in dissenting had different views. While agreeing the test was objective, he indicated there was some restraint on the courts in applying it. He said the courts would only upset decisions that would not have been made ‘but for’ the improper purpose. Courts traditionally take a broad view of powers that are part of the general management of the company, and as to what might be proper. It is necessary to identify the improper purpose, he said, and in this case none were identified Whether the duties are fiduciary • All members of the court said that the relevant directors’ duties were fiduciary, even though the High Court had said in relation to trustees that fiduciary duties were limited to proscriptive duties (such as not to act in conflict of interest or to profit from the relationship) and not prescriptive duties. In the eyes of the majority (but not Carr AJA), this seems to even extend to taking positive steps, allowing them look at the duty in terms of what is ‘reasonable’. Lee AJA thought that the duty of care and diligence was also fiduciary (or at least that serious breaches of it could be seen as a breach of a fiduciary duty), though it was not relevant in this case. ©2012 Allens 9 Whether there could be a constructive trust in relation to the breach of duty • • • Because the duties were fiduciary, third parties could be liable as constructive trustees under Barnes v Addy if, as a result of a breach of duty, they received ‘trust property’ knowing of the breach, or they knowingly assisted in the breach and the breach was a ‘dishonest and fraudulent design’. Company property in the hands of directors was treated as ‘trust property’ for this purpose, even though there was no trust. The banks could be liable if they had the requisite degree of knowledge and could be liable even though they had disposed of the company property so it could not be traced. For the second limb, the majority said there was a low threshold as to what is meant by ‘a dishonest and fraudulent design’ though it meant more than a mere breach. In this case, the breach was held to be ‘egregious’, and the second limb of Barnes v Addy could be engaged, even though no dishonesty or fraud in the common law sense was pleaded or proved, if the banks had the requisite degree of knowledge. The necessary degree of knowledge • 3 Both limbs of Barnes v Addy require knowledge. The majority held the relevant types of knowledge are the first four in the list of Peter Gibson J in Baden v Societe Generale3 • • • • (i) actual knowledge; (ii) wilfully shutting one’s eyes to the obvious; (iii)wilfully and recklessly failing to make such inquiries as an honest and reasonable man would make; (iv)knowledge of circumstances which would indicate the facts to an honest and reasonable man; and (v) knowledge of circumstances which would put an honest and reasonable man on inquiry. In this case, the majority said the banks had the types of knowledge listed in (iii) and (iv). The banks were fixed with all the knowledge that was held by the agent banks and by their solicitors. The agents had a duty to receive information on their behalf, and so the banks were deemed to have the knowledge that the agents had, even though they had not passed it on. The solicitors had the requisite degree of knowledge. This was demonstrated in part because they drafted the minutes of the directors’ meetings approving the transaction. The case gives no guide as to whether, in some cases, third parties may be insulated from having the requisite knowledge by the statutory assumptions in ss 128 and 129 of the Corporations Act. Under those sections, parties dealing with a company are entitled to assume, among other things, that its directors comply with their duties to the company, in the absence of actual knowledge or suspicion to the contrary. That should be the case, but it has not been tested. [1993] 1 WLR 509. ©2012 Allens 10 The nature and amount of the remedy • • • • The majority said complainants were entitled to equitable compensation. One concern from the point of view of lenders and directors is that equitable compensation can be more extensive than common law damages. It does not have requirements as to causation, foreseeability and remoteness. There is simply a ‘but for’ test. Another difficulty (though one not stated in the judgment) is that statutes giving proportionate liability do not apply. This is a particular concern if fiduciary duties can be breached, and compensation engaged, if directors fail to take positive steps and make enquiries. The compound interest that was part of the award is an alternative to an account of the profits that the banks would have earned on the amounts received as a result of the breach of duty, hence the high interest rate. No account is taken of tax that would have been paid on the earnings. Even though much of the amount paid to the liquidators would be returned to the banks, it was, in the view of the majority, appropriate to require the banks to pay the full amount so that the liquidators can calculate and make the necessary distributions. Ratification • The Bell Group companies who were shareholders and creditors of each company that entered the transactions ratified that entry. That ratification was held to be ineffective where there were outside creditors, as it did not involve those creditors. Where there were no outside creditors, it was still ineffective, as it was not fully informed, as there was no recognition of the absence of corporate benefit. Note the ratification was in relation to general law duties, breaches of statutory ‘duties’ in ss180 and 181 cannot be absolved by shareholder ratification, though ratification can ameliorate the possible consequences. Set-off The banks sought to set off the amounts owed to them by the borrowers against the amounts owed to the borrowers by way of equitable compensation. The court said there was no mutuality; the liability for compensation did not arise through mutual dealings before commencement of the liquidation. Further, the compensation was owed as constructive trustee. What next? The High Court The banks have announced they are seeking leave to appeal to the High Court. There are a number of issues for the High Court to explore, if it so wishes, but it remains to be seen whether it will grant leave, and on which issues. If it grants leave, then there may be a while before the court hands down its judgment. Until we know, we have an appellate judgment that propounds a number of principles and contains a number of passages that can be quoted against directors and lenders. Parties need to adapt their practices accordingly. ©2012 Allens 11 If you have any questions please do not hesitate to contact any of the specialists listed below. Sydney Diccon Loxton Partner, Lending Jeremy Low Partner, Corporate Governance T +61 2 9230 4791 Diccon.Loxton@allens.com.au T +61 2 9230 4041 Jeremy.Low@allens.com.au Michael Quinlan Partner, Insolvency T +61 2 9230 4411 Michael.Quinlan@allens.com.au Melbourne Greg Bosmans Partner, Corporate Governance T +61 3 9613 8602 Greg.Bosmans@allens.com.au Warwick Newell Partner, Lending T +61 3 9613 8915 Warwick.Newell@allens.com.au Brisbane Karla Fraser Partner, Lending T +61 7 3334 3251 Karla.Fraser@allens.com.au Geoff Rankin Partner, Insolvency T +61 7 3334 3235 Geoff.Rankin@allens.com.au Perth Tim Lester Partner, Lending T +61 8 9488 3841 Tim.Lester@allens.com.au Philip Blaxill Partner, Insolvency T +61 8 9488 3739 Philip.Blaxill@allens.com.au ©2012 Allens 12 www.allens.com.au Allens is an independent partnership operating in alliance with Linklaters LLP. 16351