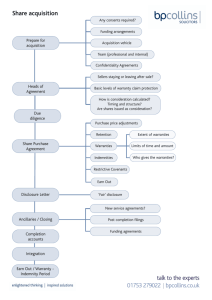

Issues paper 2: Warranties

advertisement