20/10/2015 1 I. Global Outlook II. Lightning Round I: The

advertisement

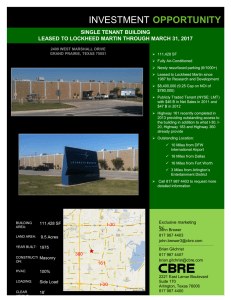

20/10/2015 MARKET OUTLOOK Spencer Levy, Americas Head of Research Vancouver, Canada: October 20, 2015 AGENDA I. Global Outlook II. Lightning Round I: The Globe III. Occupier IV.Lightning Round II: The Disruptors V. Conclusion 2 1 20/10/2015 VALUE OF CANADA’S CURRENCY VS. PRICE OF OIL USD per barrel USD per barrel 0.94 120.00 0.92 100.00 0.90 0.88 CAD/USD 0.84 60.00 0.82 0.80 US $ per barrel 80.00 0.86 40.00 0.78 0.76 20.00 0.74 0.72 0.00 CAD/USD (left) West Texas Intermediate (right) Source: Moody’s Analytics, Oct. 2015. 3 RECORD CRE PRICES LEAD TO RECORD CONDUIT LOAN LTV Source: Moody’s Investor Service Publication. “U.S. CMBS Q2 Review: Twin Peaks – Record Commercial Property Prices Lead to Record Conduit Loan MLTV Ratio July 2015”. 4 2 20/10/2015 CAPITAL MARKETS - IMPRESSIVE INVESTMENT GAINS Source: Real Capital Analytics and CBRE Research. Excludes “entity level” acquisitions. Ytd through July. 5 THE EVOLUTION OF THE FOREIGN BUYER Mexico 3% Japan 3% Germany 4% Bahrain 4% UK 6% 2007 2014 Total Volume: $48.0 Total Volume: $46.3 Other 18% Australia 28% Israel 7% Canada 17% UAE 10% Source: Real Capital Analytics, Sep. 2015. 2008 Total Volume: $15.8 1H 2015 6 Total Volume: $42.3 3 20/10/2015 WHAT DO LARGE OCCUPIERS CARE ABOUT? 1. Workplace Strategy 2. Employee Engagement / Wellness 3. Change Management • Organization Change / Transformation • Implementing Workplace Change • CRM 4. Talent • CRE Organizational • Workforce 5. Enterprise Alignment and CRM 6. Portfolio and Data Analytics 7. Occupancy Expense Management 8. Capital Planning and Management 7 SIGNIFICANT LEASE TRANSACTIONS IN CANADA – TOP 5 OFFICE INDUSTRIES Technology takes the lead Q2 2014 Q1 2015 Q2 2015 6% 9% 31% 18% 12% 12% 44% 12% 38% 15% 17% 21% 21% Finance/Insurance/Real Estate Energy/Mining Technology 27% 18% Business Services Creative Industries Life Sciences/Healthcare Government/Public Admin Other Source: CBRE Research, Q2 2015. 88 4 20/10/2015 EMPLOYMENT: CANADA’S JOB GROWTH BEING LED BY PROF. SCIENTIFIC, & TECH. SERVICES AND HEALTH CARE Oil and gas negative year-over-year % Change in National Employment, Aug. 2015 Professional, scientific and technical services Health care and social assistance Construction Educational services Forestry, fishing, mining, quarrying, oil and gas Transportation and warehousing Accommodation and food services Business, building and other support services Total employed, all industries Trade Finance, insurance, real estate and leasing Manufacturing Information, culture and recreation Public administration Agriculture -15% -10% -5% 0% % Change Since Aug. 2014 5% 10% 15% 20% 25% % Change Since Aug. 2009 Source: Statistics Canada, Aug. 2015. 9 CONVERGENCE IN NORTH AMERICAN OFFICE MARKETS Time to get a little less smug! Overall Vacancy (%) 18.0 16.0 14.0 12.0 10.0 8.0 U.S Q3 2015 Q1 2015 Q3 2014 Q1 2014 Q3 2013 Q1 2013 Q3 2012 Q1 2012 Q3 2011 Q1 2011 Q3 2010 Q1 2010 Q3 2009 Q1 2009 Q3 2008 Q1 2008 Q3 2007 Q1 2007 Q3 2006 Q1 2006 Q3 2005 Q1 2005 6.0 Canada Source: CBRE Limited, Q2 & Q3 2015. 10 5 20/10/2015 HIGH-TECH SOFTWARE/SERVICES JOB AND OFFICE RENT GROWTH Sources: U.S. Bureau of Labor Statistics and CBRE Research, July 2015. 11 “THE CHANGING AGE GAME” The demographic shift of the workforce was identified as a top trend for real estate by ULI in 2015…. 12 6 20/10/2015 MILLENIALS WORKPLACE PREFERENCES… …are similar to other generations Source: CBRE Workplace Strategy, Nov. 2014. 13 DENSIFICATION: URBAN* VS. SUBURBAN 2010-2015 Population Change 25.0% 22.1% 20.0% 17.7% 15.0% 15.2% 13.0% 11.6% 10.0% 7.0% 5.0% 6.6% 5.5% 0.0% Toronto Calgary Montreal Urban Vancouver Suburban * Urban defined as a 2 km radius from city centre. Source: 2015 Environics Analytics 14 7 20/10/2015 SUSTAINABILITY Brand and reputation drive CSR Importance of Environmental Certifications (e.g. LEED ) in Building Selection and Construction Practices Leading Driver | Corporate Social Responsibility (CSR) Program 15 CONCLUSION • • • • • Don’t fear China Don’t fear interest rate hikes either Talent trumps rent Infrastructure is the long-game Canada is ______________ 16 8 20/10/2015 Spencer G. Levy | Americas Head of Research CBRE 260 Franklin Street, Suite 400 Boston, MA 02110 T 617-912-5236 | C 443-794-5341 @ SpencerGLevy spencer.levy@cbre.com | www.cbre.com 9