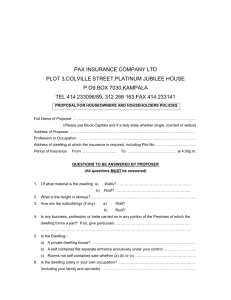

Your Personal Insurance Policy Wording Booklet

advertisement