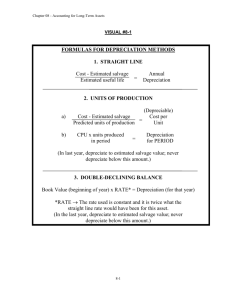

Chapter 10 Plant Assets, Natural Resources, and Intangible Assets

advertisement