Modular Forms and p-adic Representations

advertisement

Modular Forms and p-adic Representations

Spring 2015

These are some notes from lectures by Denis Benois. All mistakes and typos are due to the scribe. Please send

any remarks and corrections to alexey.beshenov@math.u-bordeaux.fr

Contents

1 Modular forms and modular curves

1.1 Fractional linear transformations .

1.2 Modular forms for SL2 (Z) . . . . . .

1.3 The fundamental domain for SL2 (Z)

1.4 Elliptic points and cuspidal points .

1.5 Riemann surfaces . . . . . . . . . . .

1.6 The Riemann surface X (Γ) . . . . .

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

1

1

3

8

11

14

17

1 Modular forms and modular curves

First we are going to review the fractional linear transformations of the complex upper half plane. Then we start

discussion of modular form with the example of modular forms for SL2 (Z).

1.1 Fractional linear transformations

Consider the complex upper half plane

H := {z = x + i y | y = Im z > 0}.

The group

GL+

2 (R) := {γ =

µ

a

c

¶

b

| a, b, c, d ∈ R, det γ > 0}

d

and its subgroup

SL2 (R) := {γ ∈ GL+

2 (R) | det γ = 1}

act on complex numbers by fractional linear transformations

γ(z) :=

az + b

.

cz + d

In fact this action restricts to H , and for each γ ∈ GL+

2 (R) we have a map

Tγ : H → H ,

z 7→ γ(z).

1

—this may be seen from the formula

Im γ(z) = det(γ)

Proposition 1.1.

Im z

.

|c z + d |2

1) GL+

2 (R) is generated by the following matrices:

µ

1

0

¶

b

with b ∈ R,

1

µ

λ

0

¶

0

with λ, µ ∈ R, λµ > 0,

µ

and

µ

0

1

¶

−1

.

0

In other words, the group of fractional linear transformations is generated by the following maps:

z 7→ z + b with b ∈ R,

z 7→ kz with k = λ/µ < 0,

and z 7→ −1/z.

2) GL+

2 (R) and SL2 (R) act on H transitively, i.e. for each z 1 , z 2 ∈ H there exists γ ∈ SL2 (R) such that γ(z 1 ) = z 2 .

3) The stabilizer of i ∈ H is

cos θ

Stab(i ) := {γ ∈ SL2 (R) | γ(i ) = i } = SO2 (R) = {

− sin θ

µ

¶

sin θ

| 0 ≤ θ < 2π}.

cos θ

µ

¶

µ

¶

1 b

1 0

Proof. For 1), we use the fact that GL+

(R)

is

generated

by

transpositions

and

, and diagonal matrices

2

0 1

c 1

µ

¶

µ

¶

λ 0

1 0

. Therefore, it remains to check that

may be decomposed into matrices of the mentioned form

0 µ

c 1

(exercise).

For 2), it is enough to show that for any z ∈ H there exists γ ∈ SL2 (R) such that γ(i ) = z. Indeed, if z = a + b i , we

µ 1/2

¶

b

ab 1/2

may take γ :=

, and

0

b −1/2

b 1/2 i + ab −1/2

= a + bi .

γ(i ) =

b −1/2

µ

µ

¶

¶

a

b

a b

ai +b

Finally, for 3), if γ(i ) = i for γ =

. Since γ ∈ SL2 (R),

, i.e. ci +d = i , then this means that γ has form

−b a

c d

2

2

we have a + b = 1.

■

Remark 1.2. In fact, SO2 (R) is a maximal compact subgroup in SL2 (R).

µ

¶

a b

Proposition 1.3. For γ =

∈ SL2 (R) we consider its trace tr γ = a + d .

c d

µ

λ

0

µ

λ

ii) If | tr γ| = 2, then γ is conjugate to a real matrix of the form

0

µ

α

iii) If | tr γ| < 2, then γ is conjugate to a real matrix of the form

−β

i) If | tr γ| > 2, then γ is conjugate to a real matrix of the form

¶

0

(and we have µ = λ−1 ).

µ

¶

1

(and we have λ = ±1).

λ

¶

β

(and α = cos θ, β = sin θ for 0 ≤ θ < 2π).

α

Proof. The characteristic polynomial of γ is X 2 − (a + d ) X + 1. Its discriminant is given by D = | tr γ|2 − 4. If D > 0,

then γ has two real eigenvalues λ and µ. If D = 0, then γ has one real eigenvalue λ of multiplicity two. If D < 0,

then γ has two complex conjugate eigenvalues.

■

µ

¶

a b

Definition 1.4. A fractional linear transformation corresponding to γ =

is called hyperbolic if | tr γ| > 2,

c d

parabolic if| tr γ| = 2, and elliptic if | tr γ| < 2.

2

Exercise 1.5.

1. A fractional linear transformation is conformal, i.e. it preserves angles between curves. (This

follows from the fact that it is holomorphic, but one can come up with a simple proof without using the implication “holomorphic” ⇒ “conformal”.)

2. A fractional linear transformation sends circles and lines to circles or lines. (For this it may be useful to decompose a transformation into some simple maps and check that each of them satisfies the claimed property.)

We finish this section with review of some metric properties of the upper half plane. We may endow H with a

distance (actually coming from a Riemannian manifold structure)

(d s)2 :=

(d x)2 + (d y)2

.

y2

If δ : [0, 1] → H is a curve, δ(t ) = x(y) + i y(t ), then its length is given by

Z

Z 1 p 0 2

x (t ) + y 0 (t )2 d t

`(δ) = d s =

.

y(t )

δ

0

The distance between two points z 1 and z 2 is

d (z 1 , z 2 ) := min `(δ).

δ(0)=z 1

δ(1)=z 2

Proposition 1.6. For each γ ∈ SL2 (R) the corresponding fractional linear transformation is an isometry with respect

to d s.

Proof. Let z := x + i y and z := x − i y. In these coordinates x =

(d s)2 = −4

and y =

z−z

2i , and

dz dz

(z − z)2

From a formula

d (γ(z)) = det(γ)

we deduce

z+z

2

dz

(c z + d )2

dz dz

d γ(z) d (γ(z))

=

.

2

(γ(z) − γ(z))

(z − z)2

■

Exercise 1.7. If Re z 1 = Re z 2 , then the geodesic passing through z 1 and z 2 is the vertical line.

If Re z 1 , Re z 2 , then the geodesic is the circle with center on the real axis which passes through z 1 and z 2 .

Exercise 1.8. The group of fractional linear transformations coincides with the group of direct isometries of H with

respect to d s. (Recall that a direct isometry is an isometry that preserves orientations.)

1.2 Modular forms for SL2 (Z)

We consider the group

µ

SL2 (Z) := {γ =

a

c

¶

b

| a, b, c, d ∈ Z, det γ = 1}

d

and its action on H by fractional linear transformations.

Definition 1.9. A meromorphic

µ

¶ function f : H → C is called weakly modular of weight k (where for us k =

a b

0, 1, 2, 3, . . .) if for all γ =

∈ SL2 (Z) it satisfies

c d

f (γ(z)) = (c z + d )k f (z).

3

We recall the following

Fact 1.10. SL2 (Z) is generated by two matrices

T :=

µ

1

0

1

1

¶

and S :=

µ

0

1

¶

−1

.

0

—for a proof see Serre’s Cours d’arithmétique. This means that the condition for being a weakly modular function

may be checked only for γ = T and S:

f (z + 1) = f (z) and

f (−1/z) = z k f (z).

• For k = 0 being weakly modular means that f is invariant under the action of SL2 (Z).

• For k = 2 being weakly modular means that f (z) d z is invariant under the action of SL2 (Z). Indeed, we use a

general formula

dz

d (γ(z)) = det(γ)

(c z + d )2

and obtain for a weakly modular f of weight k = 2 that

f (γ(z)) d γ(z) = (c z

+

d )2 f (z)

dz

.

(c z

+

d )2

• If k is odd, then the unique weakly modular function of weight k is 0. Indeed, for γ =

µ

−1

0

¶

0

∈ SL2 (Z) the

−1

modularity condition reads f (z) = f (γ(z)) = (−1)k f (z) = − f (z).

Now consider a map q from H to the open unit disk B (0, 1) := {z ∈ C | |z| < 1} given by

q : H → B (0, 1),

z 7→ e 2πi z .

If we write z = x + i y, then q(z) = e −2πy e 2πi x , and in particular if for z 1 = x 1 + i y 1 and z 2 = x 2 + i y 2 holds

q(z 1 ) = q(z 2 ), then this is equivalent to y 1 = y 2 and x 1 ≡ x 2 (mod Z).

Now let f be a weakly modular function, in particular, f (z + 1) = f (z). We can write f in the form f (z) =

g (q(z)) = g (e 2πi z ). The image of q is the punctured disk B (0, 1)\{0}, and g is a meromorphic function on B (0, 1)\{0}.

Definition 1.11. We say that f is meromorphic (resp. holomorphic) at ∞ if g is meromorphic (resp. holomorphic)

at 0.

Recall that this means the following: the function g (q) may be developed in a power series

X

g (q) =

an q n .

n∈Z

Then g is meromorphic at 0 if there exists N such that a n = 0 for n ≤ N , and g is holomorphic at 0 if a n = 0 for

n < 0.

Definition 1.12. We say that a function f : H → C is a modular form of weight k for SL2 (Z) if f is weakly modular

of weight k, holomorphic on H , and holomorphic at ∞ in the above sense.

We have the corresponding power series

f (z) =

X

an q n =

n≥0

X

n≥0

4

a n e 2πi z .

Now we consider one particular example, the Eisenstein series. Consider two numbers ω1 , ω2 ∈ H , linearly

independent over R, such that Im(ω2 /ω1 ) > 0. They generate a rank two lattice L := Zω1 + Zω2 . The group SL2 (Z)

acts on L by

µ ¶ µ

¶

µ

¶

ω2

aω2 + bω1

a b

γ

=

for γ =

∈ SL2 (Z).

ω1

cω2 + d ω1

c d

(Recall that det γ = 1, so this is indeed an action on the lattice.)

For k ≥ 4 we put

E k (ω1 , ω2 ) := E k (L) :=

X

1

ω∈L\{0}

ωk

,

which is an absolutely convergent series (exercise). We observe that for odd k the series is zero because of cancellation of terms, so for k = 3 this is not interesting. As for k = 2, we would need another definition, but we won’t talk

about it now.

This satisfies the following properties:

E k (λω1 , λω2 ) = λ−k E k (ω1 , ω2 ),

E k (γ(ω1 , ω2 )) = E k (ω1 , ω2 ) for γ ∈ SL2 (Z).

For z ∈ H and k ≥ 4 we denote

X

1

(m,n)∈Z2 \{(0,0)}

(mz + n)k

E k (z) :=

= E k (Z · 1 + Z · z).

For a moment

assume

that we know that E k (z) is holomorphic on H . Observe also that E k (z) is weakly modular,

µ

¶

a b

since for γ =

∈ SL2 (Z) we get

c d

µ

E k (γ(z)) = E k

¶

az + b

= (c z + d )k E k (az + b, c z + d ) = (c z + d )k E k (z).

cz + d

Finally, E k (z) is holomorphic at ∞, and so E k (z) is a modular form of weight k.

The modular forms E k (z) are related to the Riemann zeta function. Recall that there is a convergent series

ζ(s) :=

X 1

Y

1

=

1

s

n≥1 n

p prime 1 − p s

(Re s > 1),

and it has a meromorphic continuation to the whole complex plane, satisfying the functional equation

ζ(s) = 2s πs−1 sin

³ πs ´

2

Γ(1 − s) ζ(1 − s).

Theorem 1.13. Define for each k = 0, 1, 2, . . . the function

σk (n) :=

X

dk.

d |n

One has for even k

E k (z) = 2 ζ(k) + 2

(2πi )k X

σk−1 (n) q n ,

(k − 1)! n≥1

where q := e 2πi z .

5

In particular, from this we see that E k (z) (with k ≥ 4) are holomorphic, and so they are indeed modular forms.

We will also discuss the special values of the Riemann zeta function. Recall that the Bernoulli numbers B k may

be defined by

t

t2

t4

t6

t8

t X Bk k

t

=

1

−

+

−

+

−

+ · · · =: 1 − +

t ,

et − 1

2 6 · 2! 30 · 4! 42 · 6! 30 · 8!

2 k≥2 k!

so that B k = 0 for odd k ≥ 3 (because the function

k:

Bk :

2

t

e t −1

4

1

− 30

1

6

+ 2t is even), and for even k the first few numbers are

6

8

1

− 30

1

42

10

12

691

− 2730

5

66

···

···

Theorem 1.14 (Euler). For all k ≥ 1 one has

ζ(2k) = (−1)(k−1)

22k−1 π2k

B 2k .

(2k)!

The proof of both 1.13 and 1.14 goes along the same lines. Recall that

cos z =

e i z + e −i z

,

2

and hence

cot z = i

sin z =

e i z + e −i z

ei z

− e −i z

=i

e i z − e −i z

,

2

e 2i z + 1

e 2i z − 1

.

From this we have an expression (by definition of Bernoulli numbers, keeping in mind that B k = 0 for odd k)

z cot z = i z

e 2i z + 1

e 2i z − 1

= iz +

2i z

e 2i z − 1

i

z+

i

z + 1 −

=

X B k (2i z)k

X

B 2k 2k 2k

= 1+

(−1)k

2 z .

k!

(2k)!

k≥2

k≥1

(*)

On the other hand, we have a power series

cot z =

¶

µ

1 X

1

1

,

+

+

z n≥1 z − πn z + πn

from which we get an expression

z cot z = 1 − 2

X z2

X X ³ z ´2k

z2

1

= 1−2

,

¡ z ¢2 = 1 − 2

2

2

2

n≥1 (πn) − z

n≥1 (πn) 1 − πn

n≥1 k≥1 πn

X

where the last equality is by calculating the geometric progression sum. Changing the summation order, we obtain

z cot z = 1 − 2

µ

¶ 2k

X X 1

z

k≥1 n≥1

n 2k

π2k

= 1−2

X ζ(2k)

k≥1

π2k

z 2k

Now comparing (*) and (**), we deduce 1.14.

To show 1.13, we compare the two expressions for π cot(πz). On one hand, we have

π cot(πz) = π i

e 2πi z + 1

e 2πi z − 1

= πi

X n

q +1

2πi

= πi +

= πi − 2πi

q .

q −1

q −1

n≥0

(**)

■

(?)

On the other hand,

π cot(πz) =

µ

¶

1 X

1

1

+

+

.

z n≥1 z − n z + n

6

(??)

Now we differentiate (k − 1) times the identity “(??) = (?)” to get

µ

¶¸

·

X

X k−1 n

1

1

1

+

= −(2πi )k

n

q

−(k − 1)! k +

k

k

z

(z + n)

n≥1 (z − n)

n≥1

(keep in mind that

dq

dz

= 2πi q), so

1

zk

+

X

µ

n≥1

1

(z − n)k

+

¶

1

(z + n)k

=

(2πi )k X k−1 n

n

q .

(k − 1)! n≥1

(? ? ?)

We want to compute

E k (z) :=

1

X

k

(m,n),(0,0) (mz + n)

.

Since k is even, we see that for m = 0 the sum gives 2 ζ(k), and we may write

E k (z) = 2 ζ(k) +

1

X X

k

m ,0 n∈Z (mz + n)

= 2 ζ(k) + 2

X X

1

k

m≥1 n∈Z (mz + n)

.

We calculate the last sum using (? ? ?):

Ã

!

(2πi )k X

(2πi )k X X k−1 n

(2πi )k X X k−1 md

d

q = 2 ζ(k) + 2

d

q

= 2 ζ(k) + 2

σk−1 (n) q n ,

E k (z) = 2 ζ(k) + 2

(k − 1)! m≥1 d ≥1

(k − 1)! n≥1 d |n

(k − 1)! n≥1

which is exactly the expression from 1.13.

■

Definition 1.15. A modular form f for SL2 (Z) is called cuspidal (or parabolic, or cusp form) if f (∞) = 0.

P

This means that in the expansion f (z) = n≥0 a n q n we have a 0 = 0.

For example, consider the following functions:

g 2 (z) := 60 E 4 (z),

g 3 (z) := 140 E 6 (z),

∆(z) := g 2 (z)3 − 27 g 3 (z)2 .

We see immediately that ∆(z) is a modular form of weight 12, since g 2 (z) and g 3 (3) are modular forms of weight 4

and 6. We call ∆(z) the Ramanujan ∆-function. We claim that ∆(∞) = 0, i.e. that ∆(z) is cuspidal. From 1.13 we

know the expansions of E 4 (z) and E 6 (z):

E 4 (z) = 2 ζ(4) + · · ·

E 6 (z) = 2 ζ(6) + · · ·

From 1.14 we know the special values ζ(4) =

π4

2·32 ·5

and ζ(6) =

π6

, and so

33 ·5·7

∆(∞) = (60 · 2 · ζ(4))3 − 27 · (140 · 2 · ζ(6))3 = (22 · π4 /3)3 − 33 · (23 · π6 /33 )2 = 0.

Remark 1.16. One has

∆(z) = q

Y

(1 − q n )24 .

n≥1

We may consider the so-called modular invariant, which is given by

J (z) = 123

g 2 (z)3

.

∆(z)

Since g 23 (z) and ∆(z) are modular forms of weight 12, we see that J (z) is of weight 0, so it is invariant under the

action of SL2 (Z), i.e. J (γ(z)) = J (z) for all γ ∈ SL2 (Z). However, J (z) is not a modular form, since it has a pole at

z = ∞, where g 2 (∞) , 0 and ∆(∞) = 0. In fact, this pole is simple, and moreover

X

J (z) = q −1 +

a n q n = q −1 + 744 + 196 884 q + 21 493 760 q 2 + 864 299 970 q 3 + 20 245 856 256 q 4 + · · ·

n≥0

where all a n are integers (http://oeis.org/A000521).

7

1.3 The fundamental domain for SL2 (Z)

Definition 1.17. Let Γ be a discrete subgroup of SL2 (R). We say that D ⊂ H is a fundamental domain for Γ if

1) each orbit of Γ in H has a representative in D ;

2) if z 1 and z 2 are two elements of D lying in the same orbit, then they belong to the boundary of D .

Theorem 1.18. The set given by

1

2

1

2

D := {z ∈ H | − ≤ Re z ≤ , |z| ≥ 1}

is a fundamental domain for SL2 (Z).

µ

¶

µ

1 1

0

and S :=

0 1

1

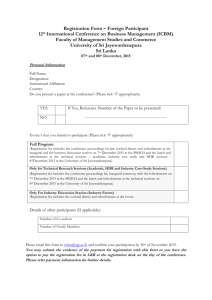

and its images under S and T are depicted as follows:

Recall that SL2 (Z) is generated by T :=

¶

−1

. The fundamental domain D from the theorem

0

Imz

T −1 D

D

i

ζ3

T

−1

SD

TD

SD

T SD

Rez

p

The boundary contains special points i and ζ3 = − 21 + 23 (third root of unity).

Proof of the theorem is routine. First we check that any element z ∈ H may be sent to D by action of an element

γ ∈ SL2 (Z). Let us look at the formula

Im z

Im γ(z) =

.

|c z + d |2

Fix some z = x + i y. Observe that for each M > 0 there exist only finitely many (c, d ) ∈ Z2 such that |c z + d |2 =

(c x + d )2 + c y 2 ≤ M . Therefore there exists γ ∈ SL2 (Z) such that |c z + d |2 is the minimal possible, and so Im γ(z)

is the maximal possible. Replacing, if necessary, γ with T m γ for some m (this does not change Im γ(z)), we can

assume that

1

1

− ≤ Re(γ(z)) ≤ .

2

2

Now we claim that |γ(z)| ≥ 1. Indeed, if we assume |γ(z)| < 1, then

Im(S(γ(z))) =

Im γ(z)

> Im γ(z),

|γ(z)|2

which contradicts maximality of Im γ(z).

8

Next part is to verify µthat if ¶z 1 , z 2 ∈ D belong to the same orbit, then z 1 and z 2 lie on the boundary of D . Let

a b

z 2 = γ(z 1 ) for some γ =

∈ SL2 (Z). Without loss of generality, we may assume that Im z 1 ≥ Im z 2 . Again,

c d

we look at the formula Im z 2 =

necessarily y 1 ≥

p

3

2 .

Im z 1

|c z 1 +d |2

and conclude that |c z 1 + d |2 ≤ 1. Let z 1 = x 1 + i y 1 . Since x 1 ∈ D , we have

Both bounds together give

(c x 1 + d )2 +

3 2

c ≤ (c x 1 + d )2 + c 2 y 12 ≤ 1.

4

(*)

Since c ∈ Z, this means c = 0 or ± 1. We analyze these cases separately.

µ

¶

±1 b

is a translation z 7→ z ± b by some integer ±b, which means Re z 1 , Re z 2 = ± 12 , and

0 ±1

we are on the boundary of D .

• If c = 0, then γ =

• If c = ±1, we look again at the inequality (*), which becomes (c x 1 + d )2 ≤ 14 . Since − 12 ≤ x 1 ≤

conclude that d = 0 or ± 1.

1

2

and d ∈ Z, we

– If d = ±1, then x 1 = ∓ 21 , and we are on the boundary as before.

µ

¶

a ∓1

1

– If d = 0, i.e. γ is of the form

, then γ(z) = az∓1

±z = − z ± a = −S(z) ± a. In this case necessarily

±1 0

|z 2 | = |z 1 | = 1, so we are on the boundary again.

This finishes our proof that D as above is a fundamental domain.

■

Recall that if f (z) is a meromorphic function in z 0 , then its order at z 0 is the integer v z0 ( f ) := m, where the

expansion of f (z) at z 0 is of the form

f (z) = a m (z − z 0 )m + a m+1 (z − z 0 )m+1 + · · ·

(a m , 0)

Similarly, if f (z) is a weakly modular form which is meromorphic at ∞, we set v ∞ ( f ) := m if the expansion in terms

of q := e 2πi z is of the form

f (z) = a m q m + a m+1 q m+1 + · · · (a m , 0).

Exercise 1.19 (Cf. Serre’s Cours d’arithmétique). Let f (z) be a weakly modular form of even weight k which is

meromorphic at ∞. Then

v∞( f ) +

X

1

1

v i ( f ) + v ζ3 ( f ) +

2

3

p∈H / SL

2 (Z)

p .i , ζ3

v p (z) =

k

.

12

(1)

The formula is derived as follows. We consider an integral

Z

γ

f 0 (z)

dz

f (z)

along contours γ of the shape depicted below; namely, γ does not contain points ζ3 , −ζ3 , and i , and it contains

one representative in H / SL2 (Z) of each zero or pole of f (points on the vertical lines in the picture).

9

C

B

D

ζ3

f 0 (z)

γ f (z)

a)

R

b)

R

c)

R

d)

R

d z = 2πi

P

p .i , ζ3

d z = −2πi v ∞ ( f ).

f 0 (z)

DE f (z)

dz +

f 0 (z)

F G f (z)

d z → −πi v i ( f ).

f 0 (z)

H A f (z)

H

−ζ3

v p ( f ).

f 0 (z)

BC f (z)

R

A

F i G

E

d z → − 2πi

3 v ζ3 ( f ).

e) Using f (−1/z) = z k f (z), one shows

f) Putting all together, one gets

P

f 0 (z)

E F f (z)

R

p .i , ζ 3

dz +

f 0 (z)

G H f (z)

R

dz →

k

12 .

k

v p ( f ) = −v ∞ ( f ) − 13 v ζ3 ( f ) − 12 v i ( f ) + 12

.

Now applying the formula (1) we want to describe the structure of modular forms. Denote the space of modular

forms of weight k by M k .

• If k = 0 and f is nonzero, then we look at the formula

v∞( f ) +

X

1

1

v i ( f ) + v ζ3 ( f ) +

2

3

p∈H / SL

v p (z) = 0

2 (Z)

p .i , ζ 3

and conclude that f is constant, so that M 0 = C.

• If k = 2, then f = 0, since otherwise the formula

v∞( f ) +

X

1

1

v i ( f ) + v ζ3 ( f ) +

2

3

p∈H / SL

2

1

v p (z) = ,

6

(Z)

2

1

v p (z) = ,

3

(Z)

p .i , ζ 3

makes no sense—left hand side cannot sum up to 1/6.

• If k = 4, then we have

v∞( f ) +

X

1

1

v i ( f ) + v ζ3 ( f ) +

2

3

p∈H / SL

p .i , ζ 3

so necessarily v ζ3 ( f ) = 1, and other terms are zero. In particular, the Eisenstein series E 4 (z) has weight 4, so

it must have a zero of order 1 at z = ζ3 . Now assume f is another modular form of weight 4. Then f /E 6 is a

modular form of weight 0, so f /E 6 = c for some c ∈ C. We conclude that M 4 = C E 4 .

10

• If k = 6, then by the same argument, f ∈ M 6 has a unique zero at i , and we see that M 6 = C E 6 .

• If k = 8, then M 8 = C E 42 .

• Interesting things happen for k = 12: we have modular form ∆(z) = 4 g 23 (z) − 27 g 32 (z) of weight 12 which is

cuspidal (∆(∞) = 0), and the formula (1) shows that ∆(z) does not vanish on H . Note that if f is another

cuspidal form of weight 12, then f /∆ is a modular form of weight 0, i.e. a constant. Denote by S k the space

of cuspidal forms of weight k. As we observed, S 12 = C, ∆. If f ∈ M 12 , then for some constant c ∈ C we have

( f − E 12 )(∞) = 0, so f − c E 12 ∈ S 12 . We get M 12 = C E 12 ⊕ C ∆.

• For k ≥ 12, we have M k = C E k ⊕ C S k and S 12 = M k−12 · ∆. In particular, dim S k = dim M k−12 .

From the obtained results we have

j k

k

12 ,

dim M k =

jkk

+ 1,

12

k ≡ 2 (mod 12),

k . 2 (mod 12).

Exercise 1.20. There are no modular forms for SL2 (Z) of negative weight (there are weakly modular).

(Assume that f is modular of weight −k; consider f 12 ∆−k and look at the formula (1).)

L

Exercise 1.21 (Serre’s book). Show that k≥0 M k is isomorphic as a C-algebra to C[E 4 , E 6 ]. (Again, use somehow

formula (1).)

1.4 Elliptic points and cuspidal points

We consider the action of SL2 (Z) on the compactified upper half plane H ∪ R ∪ {∞} given by the same formula

:= ∞; if z = ∞, then

γ(z) = az+b

c z+d . Precisely, if z , ∞ and c z + d = 0, then γ(z)

γ(∞) :=

½

a/c,

∞,

c , 0,

c = 0.

Proposition 1.22. Let γ ∈ SL2 (R) act on H ∗ .

1) γ is elliptic iff γ has one fixed point on H and one fixed point on −H .

2) γ is parabolic (cuspidal) iff γ has a unique fixed point on R ∪ {∞}.

3) γ is hyperbolic iff γ has two fixed points on R ∪ {∞}.

Proof. Assume z is fixed by γ =

µ

a

c

¶

b

, i.e. z =

d

az+b

c z+d .

Suppose that γ is elliptic, i.e. | tr γ| = |a + d | < 2. We get a

quadratic equation

c z 2 + (d − a) z − b = 0,

with discriminant D = (a + d )2 − 4 < 0, so one of the solutions

p

d ±a D

2c

lies in H . This proves 1).

¶ µ

¶

µ

1 1

−1 1

or

, i.e. for some α ∈ SL2 (R)

For 2), recall that if γ is parabolic, then it is conjugate in SL2 (R) to

0 1

0 −1

−1

γ=α

We see that both

µ

1

0

¶

µ

1

−1

and

1

0

µ

±1

0

¶

1

α.

±1

¶

1

have ∞ as the only fixed point, and hence the only fixed point of γ is

−1

α−1 (∞) ∈ R ∪ {∞}.

Proof of 3) is similar and it is left as an exercise.

■

11

Definition 1.23. Let Γ ⊂ SL2 (Z) be a discrete subgroup. A point z ∈ H ∗ is called elliptic (resp. cuspidal) for Γ if

there exists an elliptic (resp. cuspidal) element γ ∈ Γ such that γ(z) = z.

Proposition 1.24. A point z ∈ H is elliptic for Γ iff StabΓ (z) is a finite cyclic group, distinct from {±1}.

Proof. Note that

StabΓ (z) = Γ ∩ StabSL2 (R) (z).

The group StabSL2 (RR) (z) is compact, isomorphic to the circle group R/Z—indeed, by transitivity of action of SL2 (R)

on H , there exists some α ∈ SL2 (R) such that z = α(i ) and

SO2 (R) = StabSL2 (R) (i ) = α StabSL2 (R) (z) α−1 .

The rest follows from the following claims (left as an exercise).

1. A discrete subgroup of R/Z is finite and cyclic.

2. If Γ is a discrete group, then γ is of infinite order iff γ is elliptic or γ = ±1.

3. If γ is of even order 2n, then the transformation z 7→ γ(z) is of order n.

4. If −1 ∉ Γ, then each elliptic point of Γ has an odd order.

■

Proposition 1.25. Let γ ∈ SL2 (Z).

1) If γ has order 4, then γ is conjugate in SL2 (Z) to

µ

0

S=

1

−1

0

¶

or S

−1

µ

0

=

−1

¶

1

.

0

2) If γ has order 3, then γ is conjugate to

µ

0

−1

1

−1

¶

µ

0

1

−1

1

¶

or

µ

−1

1

¶

−1

.

0

µ

¶

1

.

0

3) If γ has order 6, then γ is conjugate to

or

1

−1

µ

¶

−1 0

.

0 −1

Consider the lattice Z e 1 + Z e 2 endowed with a Z[i ]-module structure

Proof of 1). The unique matrix of order 2 in SL2 (Z) is −I =

(a + b i ) ·

µ ¶

µ ¶

e1

e1

= (a + b γ)

.

e2

e2

Since Z[i ] is a PID, we have for some ideals I 1 , . . . , I n ⊂ Z[i ]

Z e 1 + Z e 2 Z[i ]/I 1 ⊕ · · · ⊕ Z[i ]/I n .

However, if I k , 0, then Z[i ]/I k is finite, but this is not possible, since Z e 1 + Z e 2 is torsion-free. Therefore, we must

have Z e 1 + Z e 2 Z[i ] (the Z-rank is 2).

µ ¶ µ ¶

1

i

Each basis of Z[i ] is conjugate in SL2 (Z) to

or

, and we have

i

1

12

µ ¶ µ ¶ µ

¶µ ¶

1

i

0 1 1

=

=

,

i

−1

−1 0 i

µ ¶ µ ¶ µ

¶µ ¶

i

−1

0 −1 i

i

=

=

.

1

i

1 0 1

i

■

Proposition 1.26. Let z ∈ H be an elliptic point for SL2 (Z). Then we have two possible cases.

1) z is conjugate to i in SL2 (Z), i.e. there exists an element α ∈ SL2 (Z) such that α(i ) = z. Then StabSL2 (Z) (z) =

α StabSL2 (Z) (i ) α−1 , where

StabSL2 (Z) (i ) = ⟨S⟩

is a cyclic group of order 4.

2) z is conjugate to ζ3 , i.e. there exists an element α ∈ SL2 (Z) such that α(ζ3 ) = z. Then StabSL2 (Z) (z) = α StabSL2 (Z) (ζ3 ) α−1 ,

where

StabSL2 (Z) (ζ3 ) = ⟨ST ⟩

is a cyclic group of order 6.

Recall that S =

µ

0

1

¶

µ

−1

1

,T =

0

0

¶

µ

1

0

, and ST =

1

1

¶

−1

.

1

µ

¶

a b

Proof. Assume that z ∈ H is elliptic for SL2 (Z), i.e. that there exists an elliptic element γ =

∈ SL2 (Z) such

c d

that γ(z) = z. Then | tr γ| = |a + d | < 2, so a + d ∈ {0, ±1}. The characteristic polynomial of γ has one of the following

forms:

a) X 2 + 1, which divides X 4 − 1 = (X + 1) (X − 1) (X 2 + 1).

b) X 2 − X + 1, which divides X 6 − 1 = (X + 1) (X − 1) (X 2 + X + 1) (X 2 − X + 1).

c) X 2 + X + 1, which divides X 6 − 1 = (X + 1) (X − 1) (X 2 + X + 1) (X 2 − X + 1).

In case a) the order of γ is 4, hence by the previous proposition it is conjugate to

b) and c) the order is 3 or 6, hence γ is conjugate to a matrix in StabSL2 (Z) (ζ3 ).

µ

0

1

¶ µ

−1

0

or

0

−1

Proposition 1.27. Let Γ be a discrete subgroup of SL2 (R) and let z ∈ R ∪ {∞} be a cuspidal point. Then

1) if γ ∈ StabΓ (z), then γ = ±1, or γ is cuspidal;

2) StabΓ (z)/(Γ ∩ {±1}) Z.

Proof. We define

P Γ (z) := {γ ∈ StabΓ (z) | γ is cuspidal} ⊂ StabΓ (z).

First assume that z = ∞. Then

P SL2 (R) (∞) = {γ ∈ SL2 (R) parabolic | γ(∞) = ∞} = {

Now

P Γ (∞) = Γ ∩ P SL2 (R) (∞),

13

µ

±1

0

¶

b

| b ∈ R}.

±1

¶

1

. In case

0

■

and P SL2 (R) (∞) is isomorphic to {±1}×R. The group P Γ (∞)/(Γ∩{±1}) is a discrete subgroup in R, so it is necessarily

µ

¶

1 h

isomorphic to Z. Its generator is the matrix

∈ Γ where h ∈ Z is the minimal possible.

0 1

We claim that if δ ∈ StabΓ (∞) and δ , ±1, then δ is a parabolic

element.

Indeed, δ is not µelliptic, since

µ

¶

¶ elliptic

a

b

a −1 −b

−1

elements do not fix ∞. If δ is hyperbolic and fixes ∞, then δ =

for a , ±1 and δ =

. Then we

0 a −1

0

a

have

µ

¶

µ

¶

1 h

1 a −2 h

δ−1

δ=

∈ StabΓ (∞).

0 1

0

1

If |a| > 1, then a −2 h < h, contradicting the minimality of h. If |a| < 1, we may replace δ with δ−1 and repeat the

same argument. We conclude that StabΓ (∞) does not contain parabolic elements, and the proposition is proved

for z = ∞.

For an arbitrary parabolic point z ∈ R∪{∞} we use the fact that there is α ∈ SL2 (R) such that z = α(∞), and then

StabΓ (z) = Stabα−1 Γ α (∞), where α−1 Γ α is a discrete subgroup. Hence all reduces to the case of ∞.

■

Proposition 1.28. Parabolic points for SL2 (Z) are Q ∪ {∞}.

Proof. ∞ is a parabolic point and

StabSL2 (Z) (∞) = {±1} × ⟨T ⟩ ,

µ

1

where T =

0

¶

1

.

1

µ

¶

a b

If z ∈ Q, then write z = a/c for two coprime integers a, c. There exists an element

∈ SL2 (Z) such that

c d

γ(∞) = a/c, so a/c is parabolic.

■

Conversely, if z ∈ R ∪ {∞} is parabolic for SL2 (Z), then for some a, b, c, d we have az+b

c z+d = z, so z ∈ Q.

1.5 Riemann surfaces

By definition, a Riemann surface is a connected two-dimensional complex manifold* . Topologically, a compact

Riemann surface is a sphere with g handles attached, and g is the genus of the surface. We recall the formula

relating genus with Euler characteristics:

χ(X ) = 2 − 2 g .

Our ultimate goal is to study the following situation: if Γ is a discrete subgroup of SL2 (R), we consider

H ∗ := H ∪ {cuspidal points of Γ},

and then Γ\H is a Riemann surface. We will need two basic results about Riemann surfaces: Riemann–Hurwitz

formula and Riemann–Roch theorem.

Let f : X → Y be a nonconstant holomorphic map between compact Riemann surfaces. Fix a point y ∈ Y and

consider one of its preimages x ∈ f −1 (y) ⊂ X . Locally, in a neighborhood of x and y, the map f may be written as

f (z) = z e x for some e x ≥ 1. We call e x the ramification index at x. If y ∈ Y is a point such that y = f (x) for some

P

x ∈ X and e x ≥ 2, we say that y is a ramification point. Note that f (x)=y e x is a locally constant function, and by

our assumption Y is connected, therefore it does not depend on the choice of y. We call this the degree of f .

Theorem 1.29 (Riemann–Hurwitz formula). Let f : X → Y be a nonconstant holomorphic map between compact

Riemann surfaces. Denote by d the degree of f . Then

X

χ(X ) = d · χ(Y ) −

(e x − 1).

x∈X

* Some part of the lecture was devoted to other basic definitions and facts about complex manifolds, but they are omitted in these notes.

14

Proof. The Euler characteristics of a surface may be calculated from a triangulation as V − E + F , where V is the

number of vertexes, E is the number of edges, and F is the number of faces. We take a triangulation of Y such that

each ramification point y ∈ Y is a vertex of the triangulation. Over each edge and each face in Y there are d edges

P

and d faces in X . As for the vertexes, over a ramification point y ∈ Y there are d − x∈ f −1 (y) (e x − 1) vertexes in the

triangulation of X . Hence the formula.

■

Let us recall some definitions and fix notation. Let X be a Riemannian surface.

• A meromorphic function on X is a map f : X → C defined on X \ {p 1 , . . . , p k } such that f is holomorphic at

each point of X \ {p 1 , . . . , p k }, and at each point p 1 , . . . , p k there is a chart (U , φ) with p i ∈ U and the function

f ◦ φ−1 is meromorphic on φ(U ). We denote by C(X ) the set of meromorphic functions on X .

• In particular, on a neighborhood of p i we have an expansion

X

a k (z − φ(p i ))k = a m (z − φ(p i ))m + a m+1 (z − φ(p i ))m+1 + · · ·

f ◦ φ−1 (z) =

kÀ−∞

with a m , 0, and we put ordp i ( f ) := m.

• A meromorphic differential form on X is a differential form that can be locally written on a chart (Ui , φi )

as ωi = f i (z) d z with f i (z) a meromorphic

function. We ask that these local expressions are compatible: for

¯

Ui ∩U j , ; holds ωi |Ui ∩U j = ω j ¯U ∩U . We denote by M 1 (X ) the set of meromorphic differential forms on X

i

j

and by Ω1 (X ) the set of holomorphic differential forms on X .

• For a meromorphic differential form ω ∈ M 1 (X ) for p ∈ X let φ : U → C be a chart such that φ(p) = 0. Then

setting z = φ(x) for x ∈ U , we can write ω = f (z) d z at a neighborhood of 0. We put ordp (ω) := ord0 ( f ), which

equals m where

f (z) = a m z m + a m+1 z m+1 + · · ·

with a m , 0. Further, the residue of ω at p is resp ω := a −1 .

Here are some basic properties. As always, X denotes a compact Riemann surface, which is assumed to be

connected.

• A function f : X → C which is holomorphic on the whole X is necessarily constant.

• The field of meromorphic functions C(X ) is a nontrivial extension of the field of holomorphic functions C.

That is, there are meromorphic functions that are not holomorphic.

• For each meromorphic differential form ω ∈ M 1 (X ) holds

X

resp (ω) = 0

p∈X

(locally, this follows from Cauchy integral formula).

• For each nonzero meromorphic function f ∈ C(X ) holds

X

ordp ( f ) = 0

p∈X

(this may be reduced to the previous result by considering ω = d f / f ).

• Let f ∈ C(X ) be a nonconstant meromorphic function. Then we may consider it as a map X → P1 (C), where

P1 (C) = C ∪ {∞}, by setting f (p) := ∞ when p ∈ X is a pole. Then f is a holomorphic map.

• Let f ∈ C(X ) be a nonconstant meromorphic function, where f : X → P1 (C) is a surjective map of degree d .

Then C(X )/C( f ) is a finite field extension of degree d .

15

As before, X denotes a compact Riemann surface. The divisor group Div(X ) is the free abelian group generated

by points p ∈ X . For f ∈ C(X ) the associated principal divisor is

X

( f ) :=

ordp ( f ) · p.

p∈X

Principal divisors form a group P(X ) ⊂ Div(X ). The class group of X is by definition

Cl(X ) := Div(X )/P(X ).

In other words, in Cl(X ) two divisors D 1 and D 2 are equivalent if D 1 = D 2 + ( f ) for some f ∈ C(X ).

P

P

For a divisor D = p∈X n p · p we set deg D = p∈X n p . In particular, we see that deg( f ) = 0 for all f ∈ C(X ).

1

To a meromorphic differential form ω ∈ M (X ) we associate a divisor

X

div(ω) :=

ordp (ω) · p.

p∈X

We assume the following

Fact 1.30. M 1 (X ) is a one-dimensional vector space over C(X ).

So if ω1 and ω2 are two meromorphic differential forms on X , then there exists a meromorphic function f ∈

C(X ) such that ω1 = f ω2 , and

div(ω1 ) = ( f ) + div(ω2 ).

In particular, the class of div(ω) in Cl(X ) does not depend on ω. Also, deg(ω1 ) = deg(ω2 ).

P

We say that a divisor D = p∈X n p · p is positive if n p ≥ 0 for all p ∈ X .

For a divisor D the corresponding linear system is

L(D) := { f ∈ C(X ) | ( f ) + D ≥ 0} ∪ {0}.

• L(D) is a C-vector space. It can be shown that it is finite dimensional, and we set `(D) := dimC L(D).

• If deg(D) < 0, then we see from the definition that L(D) = 0.

• If D 1 and D 2 are equivalent in Cl(X ), then `(D 1 ) = `(D 2 ). Indeed, if D 1 = D 2 + ( f ), then g ∈ L(D 1 ) iff g f ∈

L(D 2 ).

We are ready to state the Riemann–Roch theorem.

Theorem 1.31. Let X be a compact Riemann surface of genus g . Fix a nonzero meromorphic differential form

ω ∈ M 1 (X ). Then for each D ∈ Div(X )

`(D) = deg(D) − g + 1 + `(div(ω) − D).

(We observe that the class of div(ω) in Cl(X ), and hence `(div(ω) − D) does not depend on the choice of ω.)

We are not recalling the proof here, but we will collect some important corollaries of Riemann–Roch.

1. If D = 0, then L(D) = C, `(D) = 1, deg D = 0, so the formula becomes

`(div(ω)) = g .

2. Let Ω1 (X ) be the set of holomorphic differential forms on X , i.e.

Ω1 (X ) = { f ω | f ∈ C(X ), div( f ω) ≥ 0}.

We have

dimC Ω1 (X ) = dimC { f ∈ C(X ) | ( f ) + div(ω) ≥ 0} = `(div(ω)) = g .

16

3. Take D = div(ω). We obtain

`(div(ω)) = deg(div(ω)) − g + 1 + `(0),

and since `(div(ω)) = g , the formula reads

deg(div(ω)) = 2g − 2.

4. If we assume deg(D) > deg(div(ω)) = 2g − 2, then deg(div(ω) − D) < 0, then `(div(ω) − D) = 0, and

`(D) = deg(D) − g + 1.

Exercise 1.32. Assume that X is a compact Riemann surface of genus 0. Then X P1 (C).

Let X be a compact Riemann surface of genus g . Then there exists a surjective map f : X → P1 (C) of degree ≤ g +1.

1.6 The Riemann surface X (Γ)

Let Γ ⊂ SL2 (R) be a discrete subgroup. Then it acts on H by fractional linear transformations. We consider the

space Y (Γ) := Γ\H with the associated topology. Namely, we have the projection π : H → Y (Γ) and U ⊂ Y (Γ) is

open iff π−1 (U ) ⊂ H is open.

The basic example is Γ = SL2 (Z). We identify the points of the fundamental domain by maps T (z) = z + 1 and

S(z) = −1/z, and then SL2 (Z)\H looks like the sphere without the point ∞. We compactify it by adding ∞. The

fundamental system of neighborhoods at ∞ is

U M := {z = x + i y ∈ H | y > M }/ ⟨T ⟩ ∪ {∞}.

As a topological space, X (SL2 (Z)) is the sphere.

T

S

17