Empirical Economics

advertisement

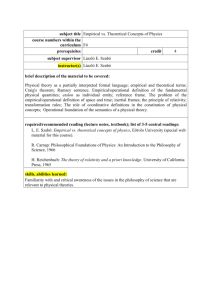

Empirical Economics PROF. LORENZO CAPPELLARI; PROF. ANDREA MONTICINI COURSE AIMS The course focuses on the application of techniques for estimating regression models, on problems commonly encountered in estimating such models, and on interpreting the estimates from such models. The goal of the course is to teach students how to deal with the empirical analysis of economic issues focussing on examples taken from the economics literature. The course runs in parallel with the Computational Laboratory for Economics where students will learn how to estimate econometric models on real world data. COURSE CONTENTS 1. 2. – – 3. – – – 4. – – – – 5. – – – 6. – – – – 7. – Introduction Empirical analysis of linear economic outcomes Properties of estimators useful for the analysis of linear outcomes Empirical application: Estimating wage equations Identifying causal relationships among economic variables The problem of endogeneity, unobserved heterogeneity and reverse causality Solving the problem using instrumental variables Empirical application: estimating returns to human capital investments. Empirical analysis of non-linear economic outcomes Properties of estimators useful for the analysis of non-linear outcomes Empirical application 1: Modelling individual unemployment Empirical application 2: Modelling happiness Empirical application 2: Modelling brand choice Empirical analysis of mixed linear/non-linear economic outcomes Properties of estimators useful for the analysis of mixed outcomes Empirical application 1: Modelling expenditures on durables Empirical application 2: Modelling women wages Univariate Time Series Models: Properties of estimators useful for the analysis of the time series data Empirical application 1: Annual Price/ earnings ratio Empirical application 2: Long-run Purchasing Power Parity Empirical application 3: The Expectation theory of the term structure Multivariate Time Series Models: Dynamic Models with Stationary Variables – – 8. – – Models with Nonstationary Variables Empirical application: Money Demand and inflation Models Based on Panel Data: Static and Dynamic Linear Models Empirical application: Explaining Individual Wages READING LIST M. VERBEEK, A Guide to Modern Econometrics, Wiley,Third edition. Detailed reading lists of papers, class notes, and additional teaching material will be uploaded on teachers web pages and/or blackboard (http://blackboard.unicatt.it/) TEACHING METHOD The course is based on classroom lectures (60 hours). ASSESSMENT METHOD Written examination NOTES Incoming students are expected to be acquainted with the materials covered in Appendices A and B of Verbeek’s textbook. Further information can be found on the lecturer's webpage at http://docenti.unicatt.it/web/searchByName.do?language=ENG or on the Faculty notice board.