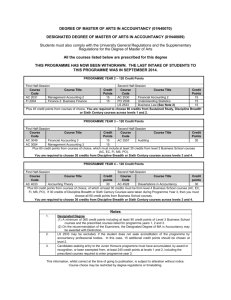

BBA in Accounting Learning Goal 1

advertisement